Want to know exactly how VCs evaluate your space startup?

Together with Seraphim, one of the leading space VCs, we’ve built this guide to unpack the inside baseball on how VCs evaluate space startups, and in turn how you can raise a successful round.

Informed by reviewing thousands of decks, and insights on which startups get the most traction on Deep Checks, this playbook helps put together a teaser deck that gets your first VC pitch scheduled.

We’ll go slide by slide on how investors decide whether or not to move forward with a startup. It’ll cover:

1. Problem: Demonstrating you’re solving a burning pain point for your customers

2. Solution: Show why you have the best solution to this problem

3. Technical risk: How to convince investors to get behind the remaining technical risk that you have

4. Traction: How to show there’s demand for your product before the market has adopted it

5. Business Model: How VCs think about your economics

6. Go to market: Showing you can become big enough, fast enough

7. Why now?: Demonstrating why your startup has just become possible to build. This is make-or-break for many pitches

8. Market Size: Why bottom up beats top down

9. Competition: Who are your competitors, and how do you demonstrate defensibility

10. Team: What makes for a world-class founding team?

11. The Ask: Use of proceeds and round size

12. Pitching: Do’s and dont’s of pitching your startup to VCs

Problem

Demonstrating you’re solving a burning pain point for your customers

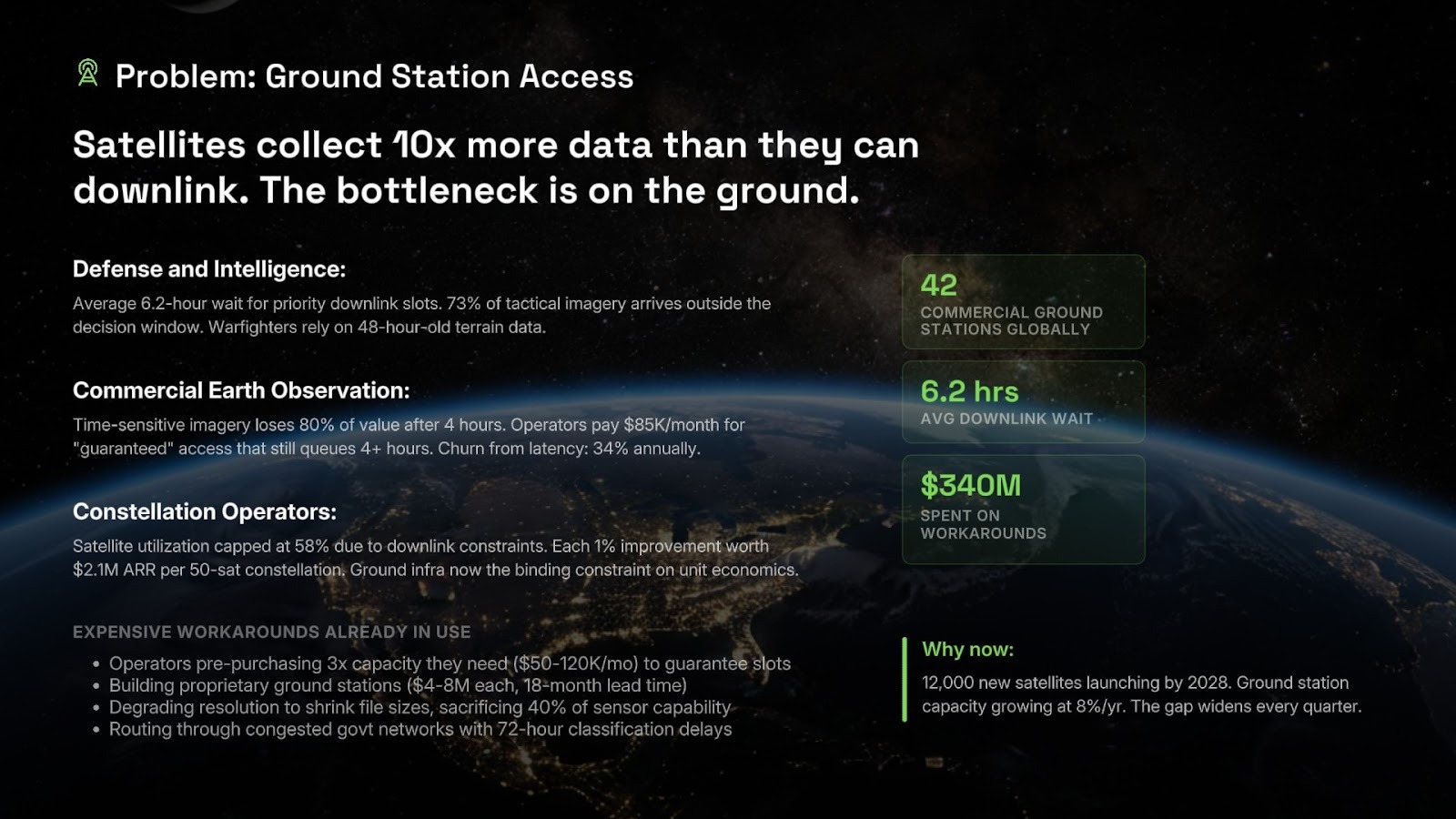

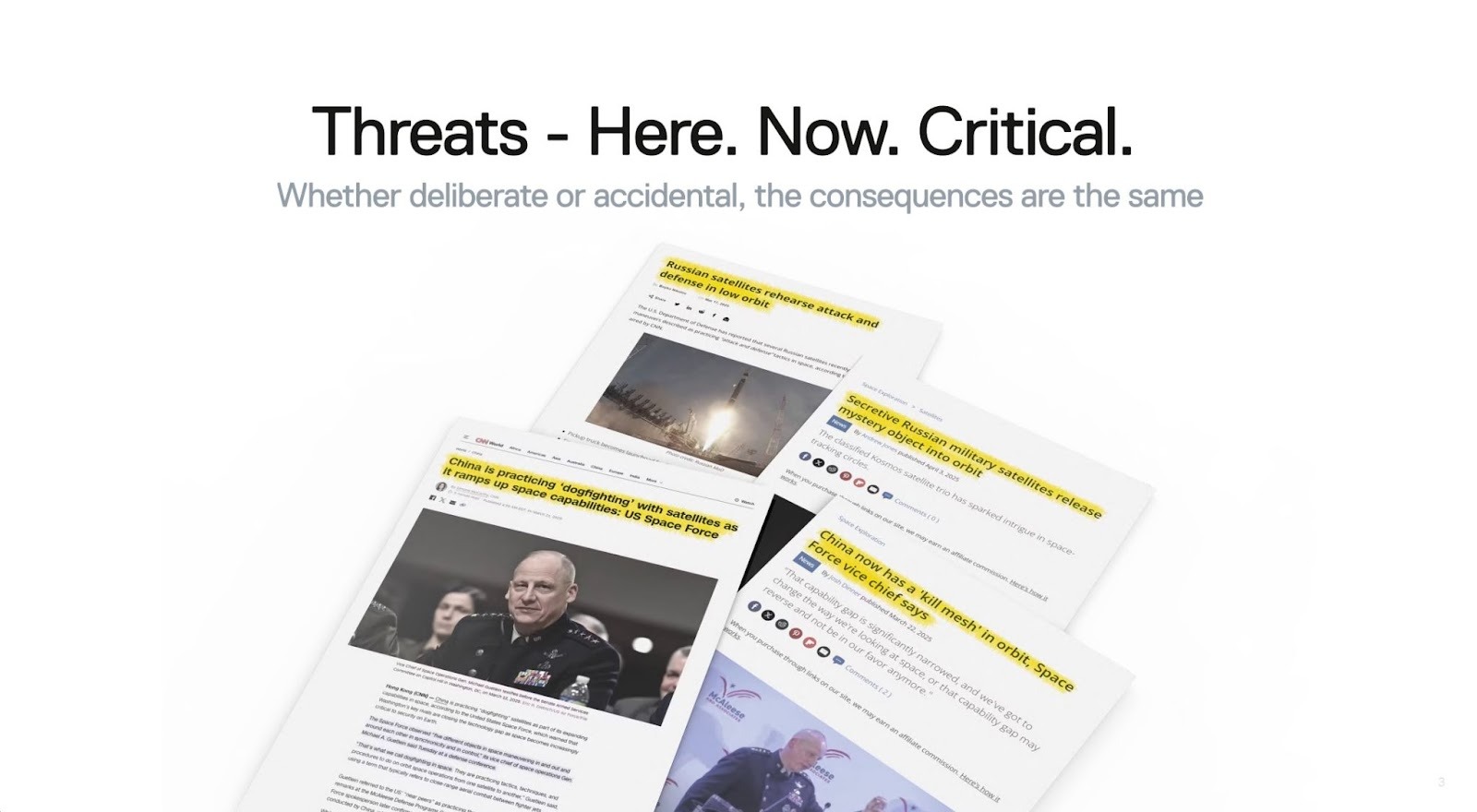

The problem slide exists to convince VCs the pain point you’re solving for your customers is a large, distinct, burning issue that they are willing to endure switching costs to solve.

A great problem statement does three things at once. It names a pain that is large, undisputed, and getting worse. It signals that the founder understands the structural reasons the problem has persisted — not just cited market reports, but done the harder work of understanding why it has not been solved. And it opens onto a larger story, so the investor can already see where this is going before you tell them.

The problem slide is the first test of the founder's mind. If your problem leads nowhere bigger — technically hard, genuinely felt, but contained — it is probably not a venture opportunity. The founders who break through are the ones whose problem, if solved, unlocks something across an entire industry. The best deep tech problems have a certain inevitability to them. You could not argue they do not need solving. You could not argue the timing is wrong.

Which means the problem slide is also the first place to have a point of view. The best founders say something that makes an investor slightly uncomfortable — something that challenges a conventional assumption about their market, their technology, or the way the industry has always worked. If your problem slide could have been written by anyone who read the same three industry reports, it will read that way. If it could only have been written by someone who spent years inside this problem, it will read that way too. The difference is felt immediately.

In describing your problem statement, it’s important to keep in mind that space customers have unique purchase dynamics that can make sales complex:

Government and defense procurement — A large share of space revenue flows through NASA, the DoD, and allied-nation equivalents. These customers operate on multi-year acquisition cycles, require extensive certification and compliance, and often favor incumbents. Understanding where you fit—SBIR/STTR grants, OTAs, or prime contractor relationships—is essential to framing your go-to-market credibly.

Integration Challenges— Most startups face a chicken & egg problem with integration on in-space systems where customers will require flight heritage (proof your technology works in space) before adopting it. On the flip side, companies are very willing to sign LOIs demonstrating intent to procure upon proof points. You can use this to your advantage to secure indications of demand, while knowing that it will take flight heritage to realize it.

Frame the problem in terms of customer mission challenges, and show how your solution fits into customers’ existing architectures and workflows holistically.

What gets VCs excited

• Problems where the operational or mission pain is quantifiable and large (cost per launch, cost per sensor revisit, communications latency, on-orbit reliability)

• Regulatory or policy tailwinds creating urgency (FCC spectrum allocation reforms, Space Policy Directive mandates, NASA CLPS program, DoD Space Force procurement growth)

• Problems that are getting worse over time (orbital debris increasing collision risk, spectrum congestion, launch manifest backlogs, aging government satellite infrastructure)

• Evidence that customers are currently using expensive or inadequate workarounds (booking expensive rideshare slots years in advance, relying on foreign launch providers, tolerating multi-day revisit times)

• Multi-stakeholder pain spanning mission operators, program managers, acquisition officers, and commercial end-users simultaneously

Red flags

• Problem statements without underlying economic or mission drivers

• Technology-first framing (“Our novel propulsion chemistry”) rather than customer-outcome framing

• Generic statements about the space economy without specific customer validation or quantified impact

• Problems that only matter once a full constellation is deployed or require industry-wide infrastructure changes before your solution creates value

• Conflating the overall growth of the space economy with a specific customer pain point

• A shallow problem statement without any additional context on the specific problems faced by your customers

Solution

Show why your solution is the best solution to this problem

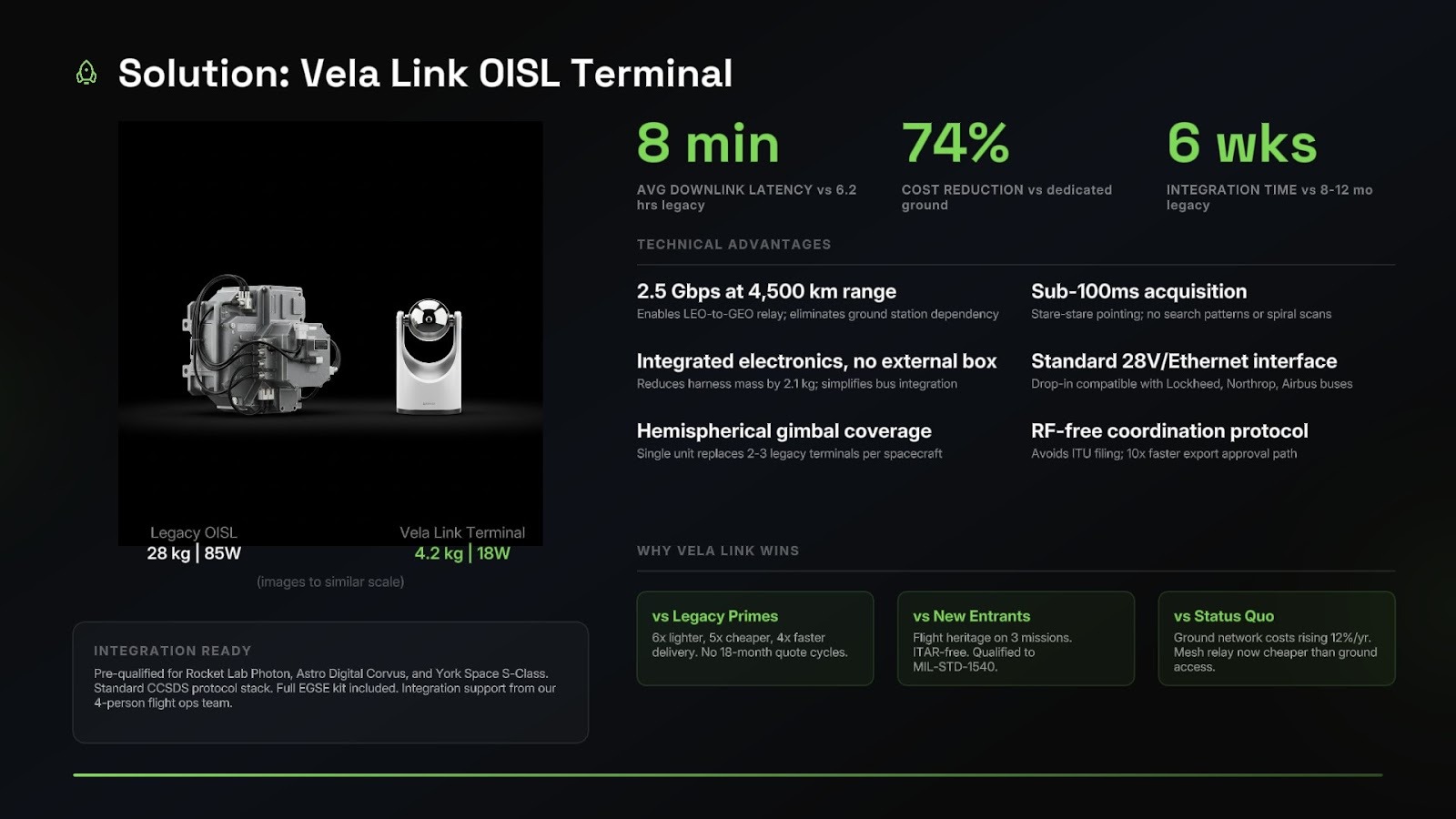

The solutions slide demonstrates why you have the best solution to the problem your customers face.

Effective solution slides show how your technology translates to customer mission and business outcomes. For example:

• Quantified cost or performance advantage tied to the needs of your end customer: “Delivers continuous Earth observation at $0.08 per sq km” rather than “12-meter GSD with a 95% revisit rate.” Translate your technical specs into the units your buyer cares about: cost per image, latency in minutes, dollars saved per mission per year.

• Direct mission comparison: “Reduces satellite build cost by 40%, launch-to-operations in under 6 months” with clear assumptions.

• Integration simplicity: “Drops into existing ground station networks with standard S-band interfaces, no custom hardware required.” Show that your solution fits into existing mission architectures, certification timelines, and physical infrastructure.

In showing why you have the best solution, you must address why your approach is better than: (1) the incumbent technology (traditional large satellites, government-owned infrastructure, terrestrial alternatives), (2) other emerging solutions in your category, and (3) doing nothing or waiting for technology to mature. These can be implied by the distinct benefits of your technology.

Your solution slide should show your distinct economic benefits and feasibility of integration for your end customers.

What gets VCs excited

• Clear cost or performance advantage over incumbents— substantial improvements on a metric customers use to make purchase decisions, with a credible path to further gains at scale

• Having the only solution for a major customer pain point

• Technology that gets better or cheaper with each unit deployed (manufacturing learning curves, software-defined upgradability, constellation network effects)

• Solutions with clear government or commercial contract alignment (NASA IDIQ vehicles, DoD OTA pathways, anchor tenant agreements) that de-risk customer acquisition

Red flags

• Development timelines exceeding 3–5 years to first revenue without strong contractual backing (unless your market structurally necessitates it)

• Leading with technical specifications absent showing mission or business value

• Comparing only to legacy government systems without addressing why other well-funded startups don’t solve this equally well

• Assuming full government contract awards or maximum available program funding

• High risk in regulatory requirements (FCC licensing, launch approvals, ITAR compliance, orbital debris mitigation)

Technical risk

How to convince investors to get behind your remaining technical risk

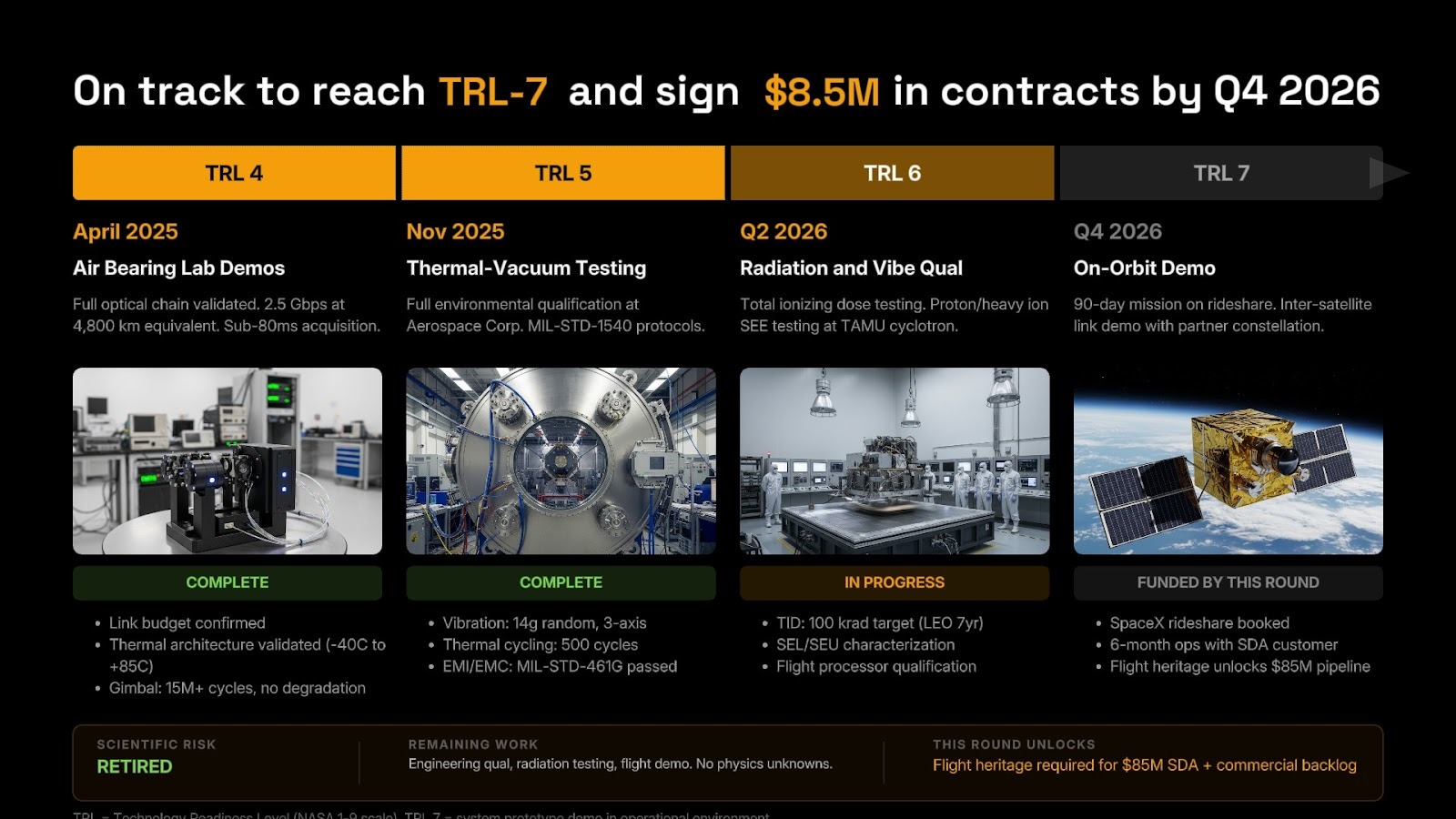

Your technical risk slide helps show what has been de-risked, and what remaining steps are needed to reach commercial scale.

Investors are not looking for certainty. They are looking for founders who have thought honestly about the paths that do not go perfectly. This does not just mean a risk slide. It means an embedded signal throughout the deck that you understand where the hard parts are and have a view on how to navigate them.

The founders who build the great companies are not the ones with the most confidence. They are the ones who have mapped their own failure modes with the most precision. If a founder cannot tell you what kills their business, they have not thought hard enough about it yet. The quality of that answer, when it comes up in conversation, tells an investor more about execution probability than any slide in the deck.

In describing this in your deck and pitch, deeptech venture investors typically accept engineering risk (technically feasible engineering work) but not scientific risk (your solution requires scientific breakthroughs to work as expected). Early stage VCs want to know:

1. What has been proven

2. What needs to be proven (within technical efficacy, system performance, technoeconomics, or scale-up)

3. Why you’re confident you’ll achieve this

The key question investors want to understand is if your technology will work in the harsh environment of space, at your projected economics. These are some areas they will want to talk through in this section of the deck:

• Sequenced milestones that show you understand how each stage unlocks the next, with explicit system improvements and scale-up risks identified

• Projected system economics at each future stage: and which customer segments will pay at each price point

• Speed of iteration demonstrated through your current progress and future development plans

• Clear capital requirements mapped over time

• Core technology validation: Has the core physics, engineering principle, or manufacturing process been validated at a meaningful scale? Is scaling up a matter of known optimization, or novel technical development?

• Space heritage and environmental qualification: Has your technology been tested to space-relevant standards (vibration, thermal vacuum, radiation)? What is your path to flight heritage?

• System integration risk: Space systems don’t operate in isolation—they connect to launch vehicles, ground stations, and customer data pipelines. Can your system integrate with existing infrastructure?

• Reliability and lifetime risk: Will your technology perform reliably over a 5–15 year design life in the space environment? How do radiation, thermal cycling, and atomic oxygen affect performance?

• Regulatory and licensing risk: What licenses and certifications does your product require (FCC, FAA launch license, NOAA remote sensing license)? What gives you confidence in securing these on your timeline?

The technical risk slide won’t cover all of this, but you can lay a strong baseline to talk atop with system block diagrams, your TRL level, and highlight any remaining

customer benefits not covered in the solution slide.

What gets VCs excited

• Components or subsystems tested to TRL 5+ with documented performance data in relevant environments. Bonus points for founders who are scrappy and have found creative ways to demonstrate tech.

• Clear delineation between engineering risk (solvable with known methods) and scientific risk (might not work)—with your remaining risk firmly in the engineering category

• Proprietary technical insights or IP that provide a fundamental advantage, not incremental improvement

• A credible manufacturing cost roadmap showing how you get from current prototype costs to commercial-scale economics

• Flight heritage—even as a payload on another spacecraft—that validates core technology in the actual space environment

Red flags

• Lab-scale performance with no path to space qualification

• Core technology relying on materials or processes not yet demonstrated at relevant scales

• Scale-up plans that skip intermediate steps (going from lab prototype directly to constellation deployment)

• No discussion of radiation effects, thermal management, or performance under real space environment variability

• Long list of remaining technical milestones without clear prioritization or funding alignment

• Dismissing the complexity of launch integration, on-orbit commissioning, or ground segment development

• Unrealistic cost estimates that ignore non-recurring engineering (NRE), testing campaigns, and regulatory timelines

Traction

How to show there’s demand for your product before the market has adopted it

The traction slide demonstrates how far you’ve come across your business goals before heading into the fundraise. It helps VCs understand your pace and capability of execution - investors are particularly interested in your rate of adoption and pace of execution.

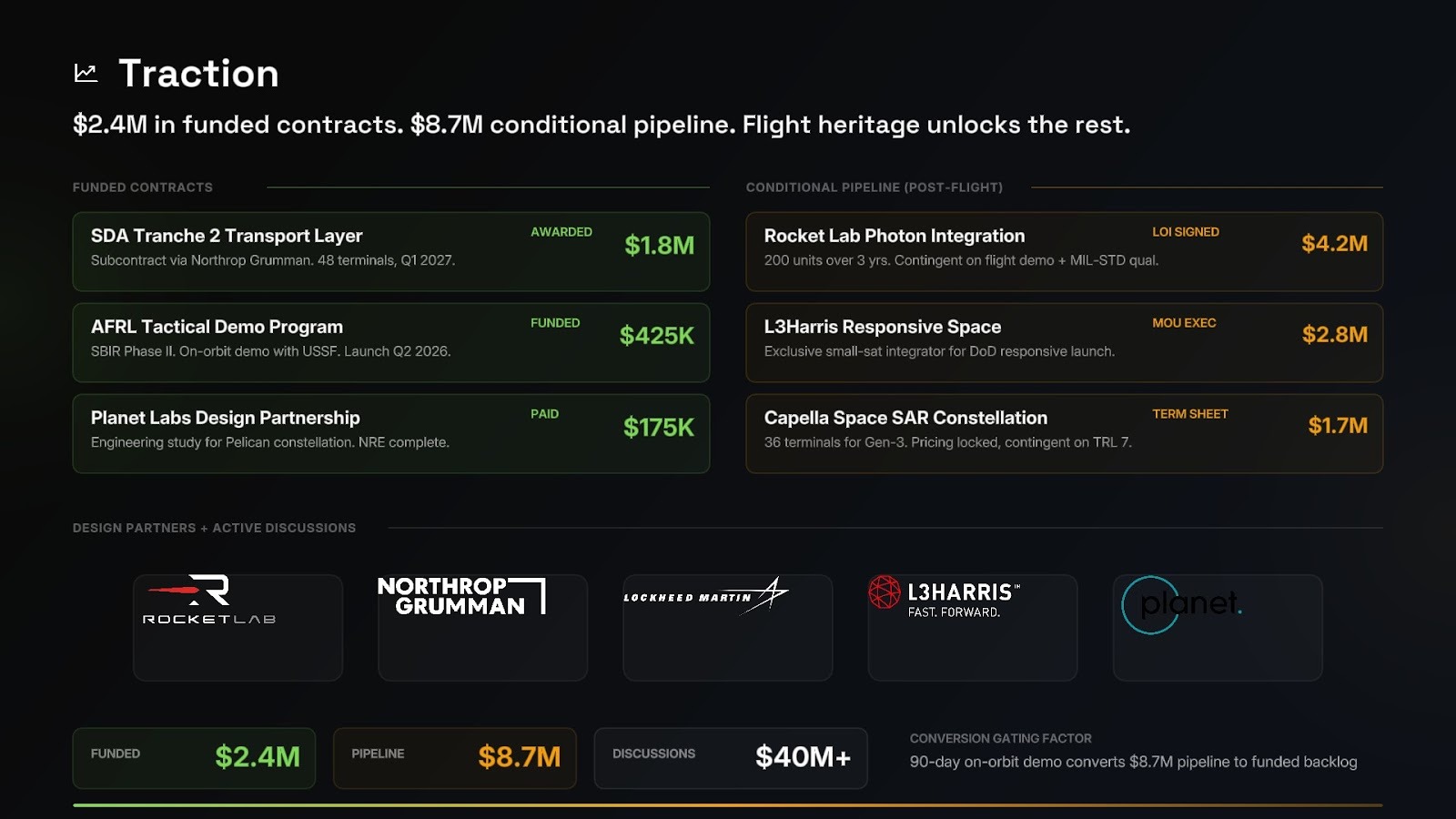

Within commercial traction, you should show the pipeline, not the forecast. A credible pipeline with real names, real conversations, and real momentum tells more truth than a five-year revenue model. What investors are looking for is evidence that the market is real and that this team can sell into it.

A company that went from nothing to a signed LOI with a credible customer in six months tells a more compelling story than one sitting on a Phase I SBIR for two years with nothing building on top of it. Show the velocity, not just the current position.

Traction is also not only commercial. A team that has shipped hardware faster than anyone expected, attracted an unlikely advisor, won a contract everyone said was too early, or converted a pilot to a paid relationship ahead of schedule — all of that is traction. It is evidence of a team that executes faster than the environment would predict. That is one of the most valuable signals an early-stage investor can receive.

Government engagement belongs in this frame too. The question is not whether you have government contracts — it is whether that engagement is building toward something a private investor would back, or whether it is the ceiling. An SBIR that seeds a capability, validates a use case, and opens a door to a commercial customer is a smart on-ramp. An SBIR that has been renewed twice with no private interest building behind it is a different story. Government can be the best possible first chapter. The question is whether there is a second one.

In order of most to least impactful, there are four ways you can demonstrate your traction to VCs:

• Paying customers or funded contracts (most valuable): A government contract (SBIR Phase II, OTA, prime subcontract - and a plan for how it expands into something more meaningful), commercial data subscription, or launch services agreement where a customer is committing real dollars to your solution.

• Design partnerships or co-development agreements: A government agency or commercial operator co-developing with you—investing resources such as facilities access, engineering support, data sharing, or integration testing.

• Letters of intent (LOIs): For space, LOIs must include specific conditions, volumes, product requirements, and pricing frameworks. “Will purchase 5 satellite buses upon demonstration of <100kg mass and TRL 6 propulsion subsystem” is strong. “Interested in exploring space data solutions” is not. This industry is fraught with large LOI claims without specific paths to procurement. The more detailed the better.

• Customer discovery depth: For pre-product companies, show 30–50+ customer conversations across your target verticals. Document specific mission requirements, willingness-to-pay thresholds, procurement processes, and success criteria. Include details like: Who’s the program manager vs. contracting officer? What’s the approval process? What performance threshold triggers a purchase decision? What are their current alternatives and costs?

Your traction slide should demonstrate how far along this spectrum you’ve gotten. At minimum for the seed stage, investors will generally want to see a functional prototype and evidence of customer engagement. You should use it to show off all progress you’ve made, and can include other accomplishments like IP filed, launch manifests secured, or spectrum licenses granted.

What gets VCs excited

• Funded government contracts (even small SBIR Phase I awards) that validate both technical approach and customer interest

• Commercial customers paying something—even discounted early-adopter pricing—for data, services, or hardware. Or demonstrations of intent of demand through LOIs

• Evidence of expanding scope: customers requesting additional capabilities, longer contract terms, or referrals to other agencies

• Having your product being used by customers, even if as a less capable MVP

• NASA, DoD, or allied-nation program office endorsements alongside commercial traction—shows both technical validation and market demand

Red flags

• Multiple funded studies or Phase I SBIRs that haven’t converted to Phase II or commercial agreements (suggests technology isn’t maturing fast enough)

• LOIs from individuals without contracting authority or budget allocation

• Over-reliance on government grants without any commercial validation or a clear path to non-dilutive follow-on funding

• Traction in one market segment (e.g., government) with no evidence of applicability to commercial markets you’re claiming in your TAM

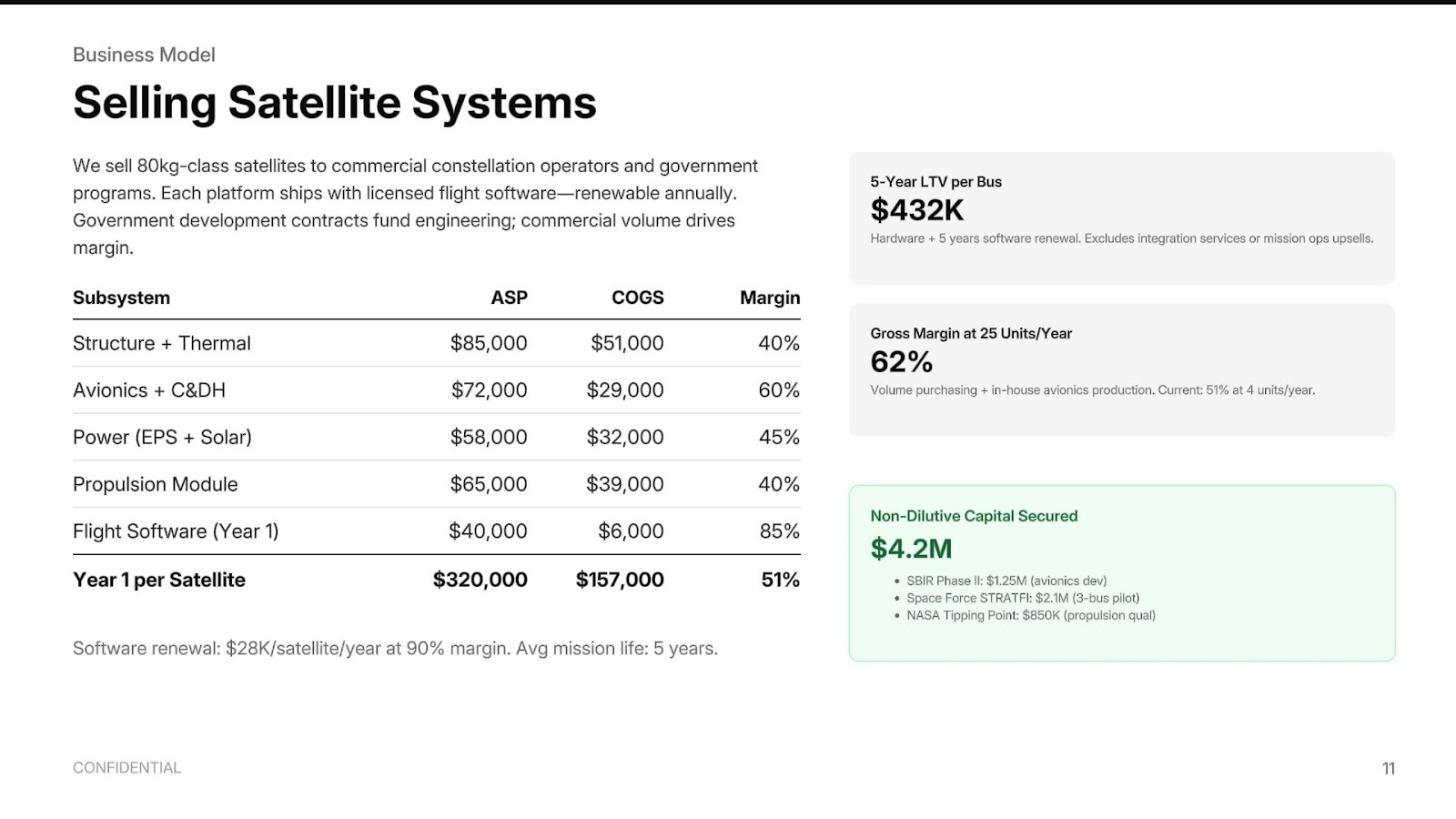

Business Model

How VCs think about your economics: cost structures, capital intensity, and contract stacks

The only business model question that matters early is simple: does this business get cheaper, faster, or more powerful with every unit of output, every dollar spent, every customer added? If yes, you are building a machine. If not, you are building a project. Machines deserve venture capital. Projects deserve grants and government contracts.

Within this, every great venture business has a denominator that falls with scale. Cost per launch. Cost per inference. Cost per megawatt hour. The first thing an investor is looking for is what that denominator is and whether it is falling. Articulating this demonstrates a deep first principles understanding of how your business fundamentals evolve over time.

In light of this, your business model should include how you make money, the price point to your end customers, and the margin you are able to achieve over time. This slide helps VCs understand the margin potential of your business, and stress test your anticipated customer pricing.

When diving deeper in your pitch, VCs want to understand:

1. Your economics today

2. Your projected economics at scale (and what needs to happen to get there)

3. How you’ll fund capital-intensive satellite builds, launch campaigns, and ground infrastructure—and how non-dilutive sources (government contracts, grants, debt) limit dilution over time

For hardware-selling companies: Show your unit economics at current and projected production volumes. VCs want to understand your bill of materials and path to positive gross margins. A cost breakdown showing how manufacturing scale drives cost reduction is highly valuable.

For data and services companies: Investors want a pathway to attractive gross margins on recurring revenue. Being able to explain why your constellation architecture, ground segment design, data processing pipeline, and pricing model are optimized for your target use case helps VCs grasp your solution’s long-term attractiveness.

What gets VCs excited

• Data-as-a-service or subscription models with demonstrated customer willingness to sign multi-year agreements

• For hardware unit sales: clear path to 40%+ gross margins at scale

• Government contracts that fund development or deployment and de-risk commercial deployment simultaneously (SBIR, AFWERX, NASA COTS-style arrangements)

• Land-and-expand dynamics where an initial government contract opens the door to larger program awards and commercial adjacencies

Red flags

• Low gross margins at scale, and no justification as to why you can maintain strong margins in light of competition

• Business model entirely dependent on a single government program or handful of businesses that could be canceled or restructured

• Satellite replacement and replenishment costs that aren’t accounted for in your long-term economics

• No clear path from current prototype costs to commercially viable margins • Revenue projections that assume perfect satellite performance, 100% availability, or maximum constellation utilization without real-world data

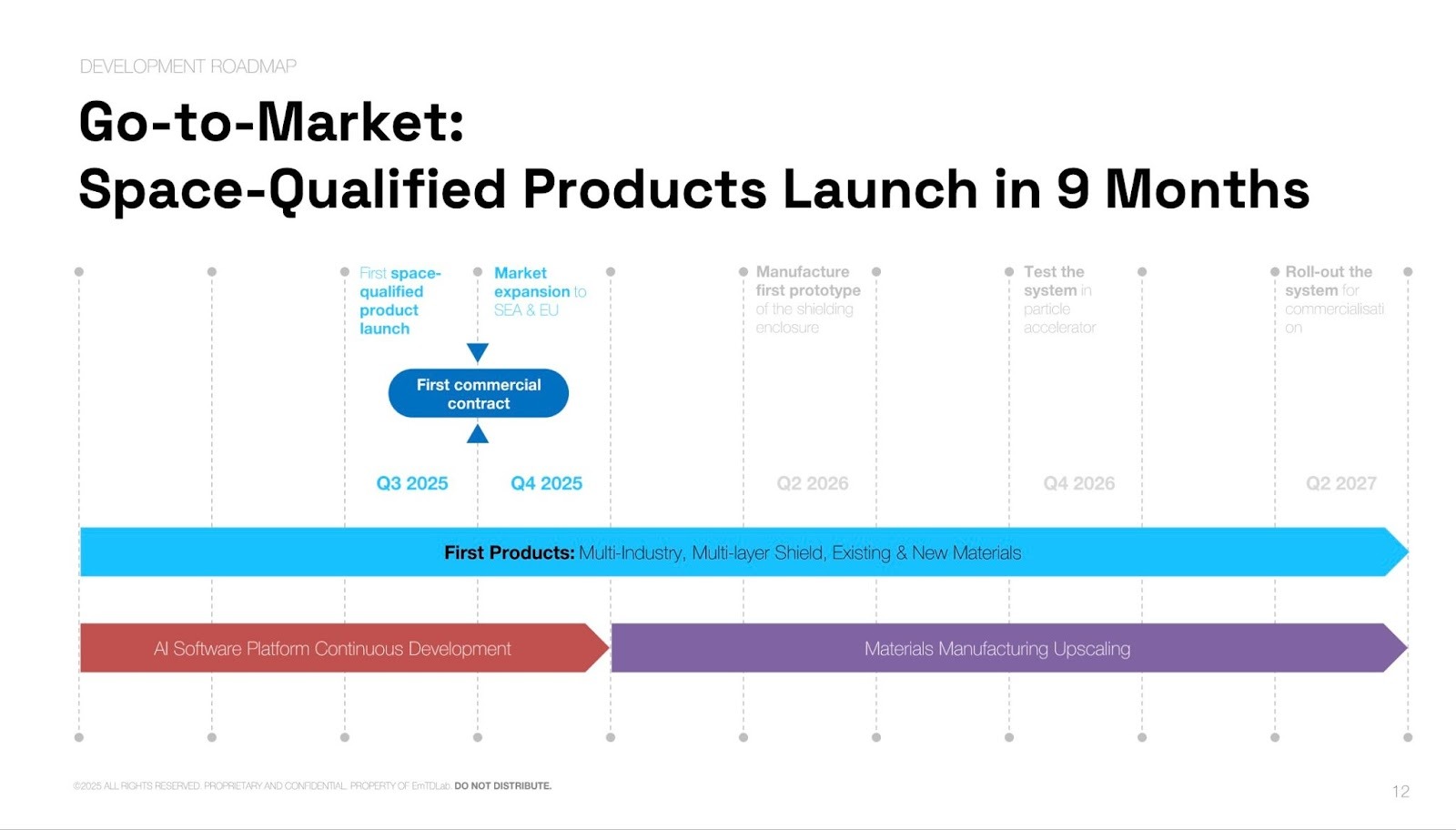

Go to market

Showing you can become big enough, fast enough

Within the pitch, the most important question to answer is how your GTM motion can support a venture scale amount of revenue ($100M+) within 5-7 years. VCs will generally use this slide to get to understand your depth of knowledge on the sales cycle and customer purchasing dynamics.

You should be prepared to talk through your customer segmentation and sequencing:

• Initial beachhead: Start with the customer segment most willing to adopt new technology and where your economics are strongest—often a specific government program office, defense contractor, or commercial operator with an acute unmet

need.

• Expansion path: How do you move from early adopters to mainstream government and commercial buyers? What proof points unlock the next tier?

• Enterprise and government timing: When can you compete for large prime contracts or sell to the largest commercial operators? What mission heritage and past performance records do you need to get there?

This slide should outline who your customers will be, how you reach them, and how you will stage your GTM if your customer type changes over time.

What gets VCs excited

• A clear beachhead with a distinct willingness to pay and ability to move fast (often a commercial customer or an agile government program like AFWERX or DIU)

• Pipeline of qualified opportunities with named agencies or commercial operators

• Customer references willing to evangelize and co-market, accelerating sales to peers in the industry

• Understanding what GTM channels generate leads at scale

• Teams that understand how to sell within larger organizations and governments. Having a track record of sales on the team helps build enthusiasm

Red flags

• No clear segmenting and sequencing of customer types

• GTM strategy that depends entirely on winning large government prime contracts without a track record of past performance

• Ignoring the role of systems integrators, prime contractors, and channel partners in scaling space businesses

• Pilots or studies that don’t convert to funded development programs or commercial contracts

Why Now

Demonstrating why your startup has just become possible to build

Most decks treat why-now as one section among many. It should be the spine of the entire narrative. Every slide should be quietly answering it.

The strongest why-now arguments distinguish between what is already locked in and what is a directional bet. Falling launch costs are locked in. Certain policy tailwinds are locked in. These are structural changes that will become inevitable with execution.

Many space startup ideas have been tried before. After addressing technical risk, explain what makes your startup uniquely possible now to overcome investors’ “prior competitive landscape” concerns.

Inflection points across technology, policy, launch access, and buyer demand create compelling narratives for why your startup is timely. Here are examples we’re seeing in 2026:

Launch access:

• Reusable launch vehicle costs have fallen by 10x over the past decade, making commercial space economics viable for an entirely new category of missions

• Dedicated small launch providers and rideshare programs have reduced time-to-orbit from years to months for smallsat operators

Technology:

• Commercial off-the-shelf (COTS) components now meet radiation tolerance requirements for LEO missions, collapsing satellite bus costs

• Advances in AI/ML, software-defined radio, and edge computing are enabling far more capable and autonomous spacecraft at small form factors

Policy and demand:

• The DoD’s pivot toward resilient, proliferated LEO architectures is driving demand for affordable, rapidly-replaceable satellites

• Commercial demand for persistent Earth observation, global connectivity, and space domain awareness is accelerating from both government and enterprise buyers

Market structure:

• Consolidation among legacy primes has left gaps in the market that agile startups can fill with faster iteration and lower overhead

• New financial instruments (space insurance products, satellite-backed debt) are making it easier to fund capital-intensive missions

Describing what inflection points make your business uniquely possible today helps investors overcome the “prior attempt” risk, and build enthusiasm for your business.

What gets VCs excited

• Specific, quantified changes in enabling conditions (“Reusable launch costs fell below $3,000/kg to LEO, making our constellation economics viable for the first time”)

• Confluence of multiple trends making your solution newly viable (launch cost reduction + COTS component maturity + government demand pull) - and spotting trends unseen by the market

• Evidence that buyer willingness-to-adopt has shifted (“Two years ago, program offices wanted studies. Now they’re issuing OTAs with delivery timelines.”)

• Recent failures of competing approaches that validate your different method (“Large GEO satellite programs are being canceled; our distributed LEO architecture avoids the single-point-of-failure problem entirely.”)

Red flags

• Generic claims about the growth of the space economy without showing what specifically changed as relevant to your business

• “Why now” arguments based on hypothetical future improvements (“When on-orbit servicing is mainstream, our components will be essential”)

• Ignoring why previous startups failed at similar problems

• Over-reliance on a single government program that could be modified or cancelled—without showing the economics work with commercial customers independently

Market Size

Why bottom up beats top down

Your market sizing slide should be broken down into your:

Total Addressable Market (TAM) The total revenue opportunity if you achieved 100% market share across all potential customers globally. Total potential customers × Annual revenue per customer

Serviceable Addressable Market (SAM) The portion of TAM you can realistically reach given your business model, geographic focus, and current capabilities. Customers matching your target profile and location × Annual revenue per customer

Serviceable Obtainable Market (SOM) The market share you can realistically capture in the next 1-3 years, accounting for competition and resources. SAM × Realistic market share % that you could target over the next few years

This method of calculating these numbers is much preferred to “top down” market sizing, where you infer total demand based on high level industry numbers. This is because VCs want to understand how large your business can get. The TAM might be $10B, but if you serve only a specific orbit regime and customer type, the amount of market you can realistically capture might be $500M.

It’s ok to lean towards top down if bottom up is hard to quantify, as well to have market sizes based on estimates into the future (i.e. 2030 market size is X), so long as

it’s clearly labeled how you’re getting to those conclusions.

The space-specific nuance to market sizing is that space markets are often too small for venture on their own, and the founders who break through are the ones whose solution unlocks capital across an entire industry, not just a vertical. This might mean applications across markets in space, or on Earth.

What gets VCs excited

• TAM >$5B with clear, defensible bottom-up math showing a venture-scale opportunity

• SOM achievable in 3–5 years representing a $100M+ revenue opportunity independently, with assumptions built from real world sales data (LOIs, your discovery)

• Market sizing validated by actual government program budgets, commercial operator procurement plans, and customer conversations

• Evidence of market growth driven by structural forces (proliferated LEO architectures, commercial space station transition, defense space budget expansion) rather than cyclical trends

• Platform potential where your initial application opens adjacent markets with realistic expansion path

• Ability to walk through how you arrived at your market sizing, and what your bottom up market size is for your SOM and SAM

Red flags

• Top-down market sizing only, citing broad “global space economy” figures without connecting them to your specific customer and product

• Market size claims that don’t match deployment realities (claiming 100% of Earth observation demand when your sensor works only in daylight, clear-sky conditions)

• Conflating government program budgets with addressable revenue (a $10B satellite program budget doesn’t mean $10B in component sales)

Competition

Who are your competitors, and how do you demonstrate defensibility

Space is a massive and growing market that can support multiple venture-scale outcomes. The concern is whether competitive pressure from incumbents or well-funded peers will crowd out your sales or erode pricing over time.

Put simply: when competing head-to-head, do you have good reason to win? Can you demonstrate a path to quickly become a trusted industry leader or achieve enough scale to carve out meaningful market share?

In discussing this slide, it’s important to keep in mind:

Space competition is multi-dimensional. You’re competing against: (1) legacy prime contractors and government-owned systems, (2) established startups with flight heritage, (3) other well-funded startups in your category, and (4) customers choosing to build in-house or wait for technology to mature. Your competitive positioning must address all four.

Addressing incumbent risk:

VCs will ask: “Why won’t Lockheed / Northrop / Boeing / SpaceX build this?” Your answer must show:

• Technology approach fundamentally different from their product roadmap or core competency

• Market segment they’re not targeting (they focus on large GEO satellites; you target smallsat constellations) or business model they can’t easily adopt

• Speed advantage: you can iterate and deploy faster while they manage legacy programs and cost-plus contracts

• Novel manufacturing or materials approach that requires different expertise than they possess

At a higher level, if you are truly at the frontier, the honest answer is that nobody is doing exactly what you are doing. A feature matrix misses the point entirely.

The question an experienced investor is actually asking is not who else is doing this. It is why a well-resourced incumbent cannot eventually own this space, and what makes the loop impossible or prohibitively expensive to copy.

Tied to showing you can overcome competition, is showing why you will maintain a competitive edge.

Defensibility can emerge from:

• Proprietary technology and IP: Novel manufacturing processes, sensor designs, propulsion approaches, or software architectures protected by patents or trade secrets.

• Operational data and learning: Each satellite deployed generates performance data that improves system design, autonomy algorithms, and predictive maintenance—advantages that compound over time.

• Flight heritage and bankability: Every orbit completed, every mission milestone achieved, every year of reliable operation builds a performance track record that insurers, program offices, and commercial customers require.

• Supply chain and manufacturing relationships: Exclusive component supply arrangements, manufacturing partnerships, or launch vehicle agreements that limit competitor access.

• Customer integration and ecosystem: Deep integrations with ground station networks, mission control systems, customer data pipelines, and operational workflows create switching costs.

• Economies of scale: Larger constellation or higher production volume drives down unit costs and enables pricing competitors cannot match, protected by the capital required to replicate your scale.

Your defensibility argument should show why your solution is directionally impossible or highly unlikely for top incumbents to build themselves. It should be technically novel, challenging to replicate without your team’s specific expertise, and protected by IP. Over time, accumulating flight heritage and customer past performance creates durable advantages over future competitors.

The strongest defensibility arguments are structural. Physics-based advantages cannot be shortcut. Operational data generated by years of flight cannot be purchased. Regulatory qualifications cannot be compressed by capital alone. If your moat is any of these, say so plainly. If it is not, build toward one that is.

The more important question underneath all of this is whether the world is ready for what you are building, not whether someone else got there first. Founders who frame competition correctly are not dismissing it — they are showing that they understand the difference between a crowded market and a frontier, and that they know which one they are operating in.

This can be shown by describing the paradigm shift in capability you bring as compared to incumbents, emerging startups, and existing processes.

What gets VCs excited

• Unique technical approach with IP protection (patents filed or granted on core innovations)

• Demonstrable performance advantages (3x lower cost per image, 10x faster revisit, 5x smaller form factor) on metrics customers actually use to make purchase decisions

• Speed to market enabled by being first to market with a differentiated capability

• Market positioning that makes you the obvious choice for a specific mission application or orbit regime

• Customer validation that your differentiators matter and are reflected in procurement criteria

Red flags

• “No competitors” or “we’re first”—there’s always competition, even if it’s a legacy government program or a terrestrial alternative

• Competitive axes that don’t drive purchase decisions (“we use a different orbit” when customers care about revisit rate and data latency)

• No clear answer to why large primes or well-funded peers won’t build this

• Differentiation based only on features, not fundamental approach or business model

• Multiple well-funded competitors further ahead with similar approaches and more flight heritage

• Claiming IP protection on obvious or easily-designed-around innovations

Team

What makes for a world-class founding team?

At the early stage, investors are not betting on the idea. They are betting on the people. A compelling idea with the wrong team is a pass. A less obvious idea with a world-class team is a serious conversation.

The team slide is not a credential list. It is the answer to a specific question: why are these the exact right people to do this specific thing at this specific moment? Domain depth matters. Relevant hardware or operational experience matters. But what matters most is whether you can read the team slide and feel that this problem was almost inevitable for these people to work on. That their backgrounds converged here for a reason. That this is their life's work, not a market they found interesting.

Founder personality and alignment to mission carry through every slide even when they are not explicitly stated. Investors feel it when it is there. They feel its absence even faster.

From this, space founders emerge from diverse backgrounds—aerospace engineers, government program managers, defense scientists, prior founders. The common thread among great founders is understanding that commercial, regulatory, and mission execution challenges matter as much as technical ones, and surrounding themselves with teams to tackle all of them.

At Julian Capital, we’ve written about what makes a great founding team here. We're excited by founding teams who are:

• Commercially minded with deep technical depth

• Building their life’s work—the culmination of their career or their final pursuit • Ambitious enough to scale to $1B+ valuation

• Relentlessly resourceful with high agency

• Persuasive and authentic storytellers

• Comprehensive in thinking through all business avenues (GTM, competitive landscape, bottom-up TAM, etc)

Within space, these qualities shine through:

• Deep aerospace and systems engineering expertise: At least one founder with the technical depth to navigate spacecraft design, systems integration, and space environment challenges—from concept through on-orbit operations.

• Hardware and manufacturing experience: Someone who has built and delivered hardware to space or near-space environments. Understands: design for manufacturing, supply chain management, quality control, environmental testing, and what goes wrong between prototype and flight.

• Government and commercial space industry expertise: Deep understanding of your target customer’s world: NASA and DoD acquisition processes, FAA and FCC licensing, ITAR, power purchase agreements for satellite services. You know procurement cycles, past performance requirements, and the language that resonates with program offices.

• Commercial and project development capability: Someone who can sell into your end market and navigate both government contracting and commercial sales. Doesn’t have to be a founder (can hire VP Business Development) but the founding team needs commercial orientation.

Your team slide should detail the qualities your team has as related to these skill sets.

What gets VCs excited

• Teams that combine deep aerospace engineering expertise,

hardware/manufacturing experience, and space industry commercial orientation • Founders who have successfully built, launched, and operated space systems before (even in prior companies or government roles)

• Deep domain expertise in target space market with existing customer, prime contractor, and program office relationships

• Track record of attracting top aerospace engineering and systems integration talent

• Founders who are mission-driven and committed for the long term—space businesses require a decade of dedication

• Understanding of government contracting vehicles, ITAR compliance, and capital structures needed to scale space programs

Red flags

• Teams without anyone who has designed, built, or operated hardware in a space or space-adjacent environment

• Pure software teams trying to build complex space hardware without an experienced aerospace hardware co-founder

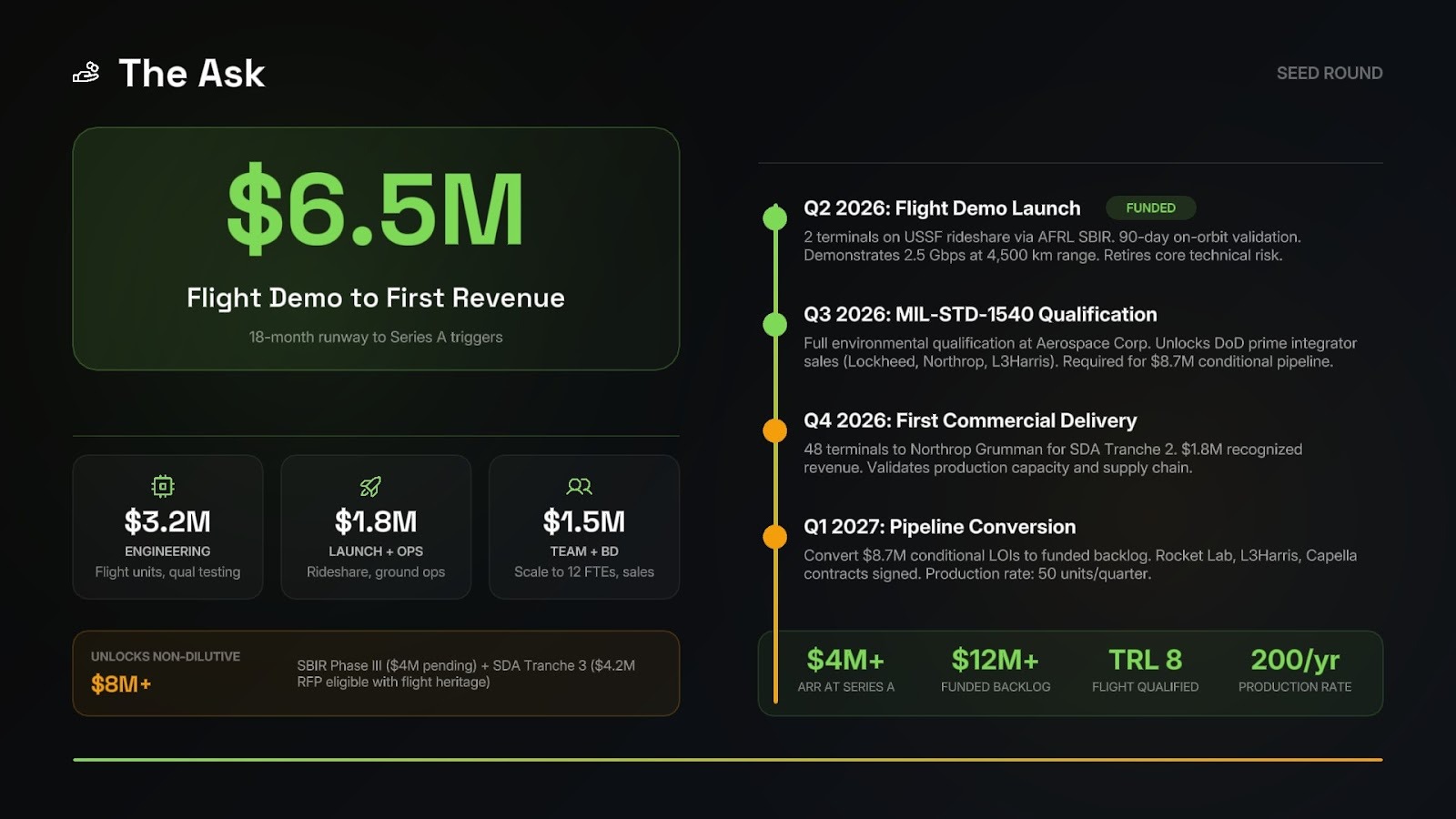

The Ask: Use of proceeds and round size

The ask shows how much you are raising and what you plan to accomplish with it. We wrote about choosing how much to raise here.

You should account for the capital intensity of spacecraft development, launch campaigns, ground segment build-out, and the long timelines associated with government procurement and commercial space sales cycles. Investors want to see that your raise gets you to clearly defined technical and commercial milestones.

The round size, the milestone it targets, and the path to the next round should form a single coherent argument. We are raising X to get to Y, which makes Z the natural next conversation. If those three things do not connect cleanly, the ask feels arbitrary and the investor has no way to evaluate whether the capital is being deployed with conviction or simply being consumed.

The milestones you are buying should be irreversible. A technical proof point that permanently changes the risk profile. A customer relationship that opens a category. A flight that no competitor can claim. Irreversible matters because it signals that the capital is doing permanent work — not funding another year of existence, but closing off lines of doubt that can never be reopened.

The best use of early venture capital is not survival. It is the permanent, compounding reduction of the most important risks in the business. Show that you understand the difference, and show that this round gets you there.

What gets VCs excited

• Raise sized to specific technical or commercial milestones (first flight demonstration, first paying customer, first constellation satellite on orbit, specific

performance threshold)

• Clear articulation of what de-risking the next round requires

• Evidence that non-dilutive capital (SBIR/STTR grants, DoD OTAs, NASA commercial programs) has been pursued or secured to extend runway

• Use of proceeds that maps directly to the team, hardware development, and launch campaigns needed to hit stated milestones

Red flags

• Raise sized by “how long we can survive” rather than “what we need to prove”

• No clear milestone that the funding unlocks—just generic “product development and sales”

• Underestimating capex requirements for environmental testing, launch campaigns, ground station build-out, or regulatory approvals. You should give yourself a 6+ month buffer to give room for delays

• Assuming maximum government grant funding without contingency, or not accounting for the 12–18 month lag between SBIR application and award

Pitching: Do’s & Dont’s

Here’s how (and how not) to pitch:

The best pitches are conversational. Answers should be succinct yet demonstrate depth of thought.

Great founders bridge vision with detail. They intimately understand their problem space and can explain it clearly—both the technical challenge and the customer and mission system around it. They understand the path to scale and can map how the business will evolve getting there.

Do

• Be honest about what doesn’t work yet: VCs appreciate realism. “Our propulsion system has demonstrated 1,500 seconds of specific impulse in vacuum testing; we’re targeting 1,800 seconds with our next-gen thruster design.”

• Have strong answers on unit economics: You should be able to walk through your projected satellite cost, launch cost, ground segment cost, and what revenue per satellite is required to achieve your target returns.

• Demonstrate customer intimacy: Drop specific details that show you deeply understand your buyer: “DoD acquisition for a program of this size requires an OTA

agreement, a successful CDR, and typically an 18–24 month evaluation period before a production contract is awarded.”

• Address the “why now” directly: Proactively explain what’s changed that makes your solution viable and your business timely.

• Acknowledge and address incumbent risk: Don’t wait for VCs to ask “Why won’t Lockheed/Northrop/SpaceX build this?” Address it upfront with a credible, specific answer.

• Lean in on your team: At the early stages, you and your team are a driving decision factor. Show why you’re uniquely qualified to execute in one of the most demanding technical and regulatory environments in the world.

Don’t

• Get lost in technical details: Focus on what your system does, what it costs, and why customers need it. Dive further into the engineering when prompted to.

• Overclaim your capabilities: Every space technology has limitations—orbit regimes, revisit rates, power constraints, launch vehicle compatibility. Be specific about what you can and cannot do.

• Dismiss competition: Acknowledge competitors—including legacy government systems and the status quo—and explain your differentiation.

• Ignore the commercialization challenge: If your team is all aerospace engineers or scientists with no business development or government contracting experience, acknowledge this as a gap and show your plan to address it (advisory board, early commercial hires, prime contractor partnerships).

We hope this guide was useful to you and if you’d like to get in touch, don’t hesitate to reach out to Julian.Capital, Seraphim, and additional contributor, Alan Yu. You can also apply in <1 minute to get put in touch with thesis fit investors for free at DeepChecks.VC.