Medical Devices

Want to know exactly how VCs evaluate your medical device startup?

Together with SOSV — one of the most active early stage VCs that invests in medical devices — we’ve built this guide to unpack the inside baseball on how VCs evaluate medical devices startups, and in turn how you can raise a successful round.

Informed by the thousands of decks we’ve reviewed, and insights on which startups get the most traction on Deep Checks, this playbook helps put together a teaser deck that gets your first VC pitch scheduled.

We’ll go slide by slide on how investors decide whether or not to move forward with a startup. It’ll cover:

1. Problem: Demonstrating you're solving a burning clinical or operational pain point

2. Solution: Show why your device is the best solution to this problem

3. Technical Risk: How to convince investors to get behind your remaining development and regulatory risk

4. Traction: How to show clinical and commercial demand before broad market adoption

5. Business Model: How VCs think about your economics

6. Market Size: Why bottom up beats top down

7. Go to Market: Showing you can reach physicians, hospitals, and health systems fast enough

8. Why Now?: Demonstrating why your device has just become possible to build and sell.

9. Competition: Who are your competitors, and how do you demonstrate clinical and commercial defensibility

10. Team: What makes for a world-class medtech founding team?

11. The Ask: Use of proceeds and round size

12. Pitching: Do's and don'ts

Problem

Demonstrating you're solving a burning clinical or operational pain point for your customers

The problem slide exists to convince VCs the pain point you’re solving for your customers is a large, distinct, burning issue that they are willing to endure switching costs to solve.

In medical devices, the question is generally whether the market is willing to pay for your solution, whether reimbursement exists or can be established, and whether you can get physicians to change their practice patterns to adopt it. Namely: who is your patient population, the underlying problem, and desired outcome to improve care.

In light of this, medtech customers have unique purchase dynamics that can make sales complex:

- Physician adoption and behavior change — Even the best device fails commercially if providers won't change how they operate. Show you understand the specific workflow your device enters, what training burden it imposes, and what clinical outcome improvement is compelling enough to drive adoption.

- Hospital and health system purchasing — Most capital equipment and many disposables are purchased through value analysis committees (VACs), GPO contracts, and formulary processes that can take 6–18 months. Knowing how hospital procurement works for your product category will help you address this.

- Reimbursement dependency — In the US, most medical devices depend on CMS coverage and adequate reimbursement rates to drive adoption. Whether you're coding to an existing CPT code, pursuing a new technology add-on payment, or targeting cash-pay markets, you need to show that your reimbursement pathway is understood and achievable.

- Regulatory pathway — FDA clearance or approval is a prerequisite for US commercialization. Whether your path is 510(k) substantial equivalence, De Novo classification, or PMA approval, investors need to see that you understand what is required and have a credible timeline.

Are you solving a clear unmet clinical need with a compelling patient outcome, or offering a marginal improvement to a workflow that physicians already tolerate?

Frame the problem in terms of clinical and economic burden on patients, physicians, and health systems. And show how your solution fits into the existing clinical workflow without requiring hospitals to rebuild their operations around you.

How to show this:

In your deck, start with a slide that outlines the general clinical or operational challenge, then follow with a slide on the specific unmet need your device addresses—ideally quantified in terms of patient outcomes, procedure costs, or system burden.

What gets VCs excited

- Problems where the clinical and economic burden is quantifiable and large—complication rates, readmission rates, procedure costs, length of stay, or quality-adjusted life years lost

- Unmet needs supported by published clinical literature, society guidelines citing inadequacy of current treatment, or FDA breakthrough device designation

- Problems getting worse over time: aging population increasing disease prevalence, surgeon shortage reducing access to complex procedures, rising hospital costs creating pressure to shift care to lower-acuity settings

- Evidence that physicians are currently using workarounds or off-label applications that reveal demand: using laparoscopic tools for robotic procedures, repurposing imaging systems across specialties, or combining multiple disposables to approximate a function your device performs in one step

- Payer pressure and outcome-based contracting creating urgency: bundled payments that penalize complications your device prevents, CMS quality metrics tied to your clinical endpoint

Red flags

- Problems framed around regulatory or CPT code availability alone without underlying clinical and economic drivers—reimbursement can change, outcomes data is durable

- Technology-first framing ('Our novel piezoelectric actuator') rather than clinical outcome framing ('Reduces procedure time by 40% and eliminates the most common intraoperative complication')

- Generic statements about large patient populations without showing what percentage are inadequately served by current treatment

- Problems that only matter at massive scale or require full system transformation—a hospital IT infrastructure overhaul, a specialty care redesign—before your device creates value

- A problem slide that simply says 'X million patients suffer from this condition' without showing why current treatments fail and why those patients or their physicians would choose your device

Solution

Show why your device is the best solution to this problem

The solution slide demonstrates why your device is uniquely suited to the clinical problem your customers face.

Effective solution slides translate device performance into clinical and economic outcomes. For example:

- Quantified clinical benefit: 'Reduces major adverse cardiac events by 32% versus medical management in the target population' rather than 'novel drug-eluting scaffold with bioresorbable polymer.'

- Procedural and workflow advantage: 'Cuts procedure time from 90 minutes to 35 minutes, reduces contrast use by 60%, and eliminates the need for general anesthesia—enabling same-day discharge.' Show that your device improves the economics and logistics of the procedure, not just the outcome.

- Physician learning curve: 'Achieves proficiency in 5 cases based on proctored training data, compared to 50+ cases for open surgical alternatives.' Show that adoption doesn't require years of retraining.

- Safety and durability profile: 'Zero device-related serious adverse events across 280 first-in-human procedures, 36-month durability data showing sustained efficacy.' Show the safety data you have and what remains to be collected.

In showing why you have the best solution, you must address why your approach is better than: (1) the current standard of care (medication, open surgery, watchful waiting), (2) other emerging devices in your category, and (3) doing nothing or waiting for guidelines to evolve. These can be implied by the distinct clinical and economic benefits of your device.

What gets VCs excited

- Clear clinical superiority over current standard of care—ideally supported by IDE trial data, real-world evidence, or a published pivotal study showing statistically significant improvement on a clinically meaningful endpoint

- Devices that expand the treatable population by enabling procedures that weren't previously possible, safe, or accessible

- Technology that improves with each generation: next-gen iterations that compound the initial clinical advantage through improved materials, sensing, or software

- Solutions with clear reimbursement alignment: existing CPT codes with adequate relative value units, a credible path to a new technology add-on payment, or a cash-pay market with demonstrated willingness to pay

- Dual benefit of better outcomes and lower total cost of care—devices that both improve clinical results and reduce the overall episode cost are the strongest reimbursement and commercial stories

Red flags

- Claiming clinical superiority without data—'we expect our device will outperform current treatment' is not a solution slide

- Leading with engineering specifications (impedance, burst pressure, material composition) before showing what those specifications mean for the patient and the physician

- Comparing only to legacy open surgical approaches without addressing why other minimally invasive or interventional alternatives don't solve this equally well

- Physician training and adoption requirements that are so high that sales cycles become multi-year educational campaigns

- Reimbursement assumptions that require new CPT codes or PMA-level clinical evidence when your current data is preliminary

Technical risk

How to convince investors to get behind your remaining development and regulatory risk

Your technical risk slide helps show what has been de-risked, and what remaining steps are needed to reach commercialization. In medtech, this includes both engineering risk and regulatory risk—both must be addressed.

Investors in medical devices accept development risk (technically feasible engineering work to refine and scale a device) but not fundamental feasibility risk (your mechanism of action requires a scientific breakthrough to work as intended in the clinical environment). Early stage VCs want to know:

- What has been demonstrated in bench testing, animal studies, or human use

- What remains to be demonstrated—clinical efficacy at scale, long-term durability, manufacturing consistency

- What the FDA regulatory pathway is, what submission type is required, and what clinical evidence the agency will need

- Why you're confident you'll achieve clearance or approval on the timeline and budget you've projected

The key question investors want to understand is whether your device will work in real clinical use, clear the FDA, achieve reimbursement, and reach your projected commercial economics. These are some areas they will want to talk through:

- Regulatory pathway clarity: Is your path 510(k), De Novo, or PMA? Have you had a Pre-Sub meeting with FDA to align on the predicate device, special controls, or clinical study design? What is the realistic timeline from IDE approval (if required) to clearance or approval?

- Clinical study design and endpoint: If a clinical trial is required, what is your primary endpoint and how was it selected? Is it a clinically meaningful endpoint that FDA will accept, or a surrogate that may require additional evidence? What is your powering assumption and enrollment timeline?

- Manufacturing and quality system risk: Can your device be manufactured consistently to specification at commercial scale? What is your COGS at current production and at target volume?

- Biocompatibility and sterilization: Have you completed biocompatibility testing? What is your sterilization modality and have you completed validation?

- Durability and failure mode analysis: What is the expected device lifetime and what accelerated aging data supports it? What are the failure modes and what mitigations are in place?

- Reimbursement pathway: Separately from FDA clearance, what is the pathway to coverage and adequate reimbursement? Is there an existing code, and at what rate? If a new code is needed, what clinical evidence and MEDCAC review process is required?

The technical risk slide won't cover all of this, but you can lay a strong baseline with a regulatory timeline and what has been demonstrated by means of technical progress. It should outline the technical readiness level of your device, and describe the remaining technical risk to pare down.

What gets VCs excited

- A strong narrative as to why you’ll pass upcoming human trials

- A Pre-Sub meeting with FDA that has aligned on predicate device, special controls, or IDE study design—showing the agency is not a black box

- Clear delineation between engineering risk (solvable with known methods) and regulatory risk (a study design FDA will accept)—with both risks actively managed

- Manufacturing partnership with a contract manufacturer experienced in FDA-regulated device production

Red flags

- No Pre-Sub meeting with FDA and no plan to have one before spending heavily on clinical studies

- Assuming a 510(k) pathway without a credible predicate device and without having discussed the classification with FDA

- Clinical study designs powered for surrogate endpoints when FDA is likely to require a clinical outcome endpoint

- Manufacturing plans that assume the device can be made at COGS targets without evidence from a contract manufacturer

- Reimbursement treated as an afterthought to be figured out after FDA clearance

Traction

How to show clinical and commercial demand before broad market adoption

The traction slide demonstrates how far you've come across your clinical and commercial goals before heading into the fundraise. It helps VCs understand your pace and capability of execution in a highly regulated environment.

For pre-clinical stage companies, VCs generally look for verbal buy-in from key opinion leaders. Show 20–40+ conversations with the target physicians across the institutions where this device would be used. LOIs help further demonstrate intent. Be ready to walk through their current practice patterns, what outcome improvement would drive them to change, and what their institution's procurement process looks like.

Your traction slide should demonstrate how far you’ve gotten in clinician validation, and can speak to regulatory or insurance reimbursement readiness as well if not addressed in the technical risk slide.

What gets VCs excited

- First-in-human data with a clean safety profile and promising efficacy signals

- Named KOL physician champions who are actively using or considering the device

- Peer-reviewed publications or major conference presentations of your clinical data

- Grant funding (NIH SBIR, NSF, BARDA) alongside commercial or clinical traction—validates technical merit and clinical relevance

Red flags

- Physician interest that hasn't converted to IRB-approved use or intent of commercial adoption

- Animal study data without a plan or timeline for first-in-human use

- Clinical data from international markets that doesn't translate to FDA requirements or US payer coverage

Business Model

How VCs think about your reimbursement strategy, ASP, and margin structure

Your business model slide should include how you make money, your average selling price to hospitals or physicians, the reimbursement rate that drives adoption, and the gross margin you can achieve. This slide helps VCs understand the margin potential of your business and stress test your commercial model.

When diving deeper in your pitch, VCs want to understand:

- Your gross margin today and at commercial scale—what drives the improvement (manufacturing volume, supplier relationships, design-for-manufacturability iterations)

- Your reimbursement plan, and resulting economics to providers, payors, and potentially distributors.

What gets VCs excited

- Existing CPT codes with adequate reimbursement rates relative to your ASP—ideally a 3:1 or better ratio of reimbursement to device cost to create clear economic value for the hospital

- Single-use disposable model with 65%+ gross margin at scale and a clear path to get there from current production economics

- Capital equipment with high-margin disposable pull-through: the system placement is the sales event, and recurring disposable revenue drives the financial return

- International revenue from CE-marked markets that validates ASP and physician adoption before US commercialization

- Value-based care alignment: devices that reduce total episode cost, hospital readmissions, or complication rates in ways that health systems can document and contract around

Red flags

- Gross margins below 50% at scale for a disposable device, or below 40% for capital equipment, without a compelling structural explanation

- Reimbursement strategy that depends on new CPT code creation without a clear pathway, timeline, and clinical evidence requirements

- Business model entirely dependent on out-of-pocket patient payment without demonstrated willingness-to-pay data

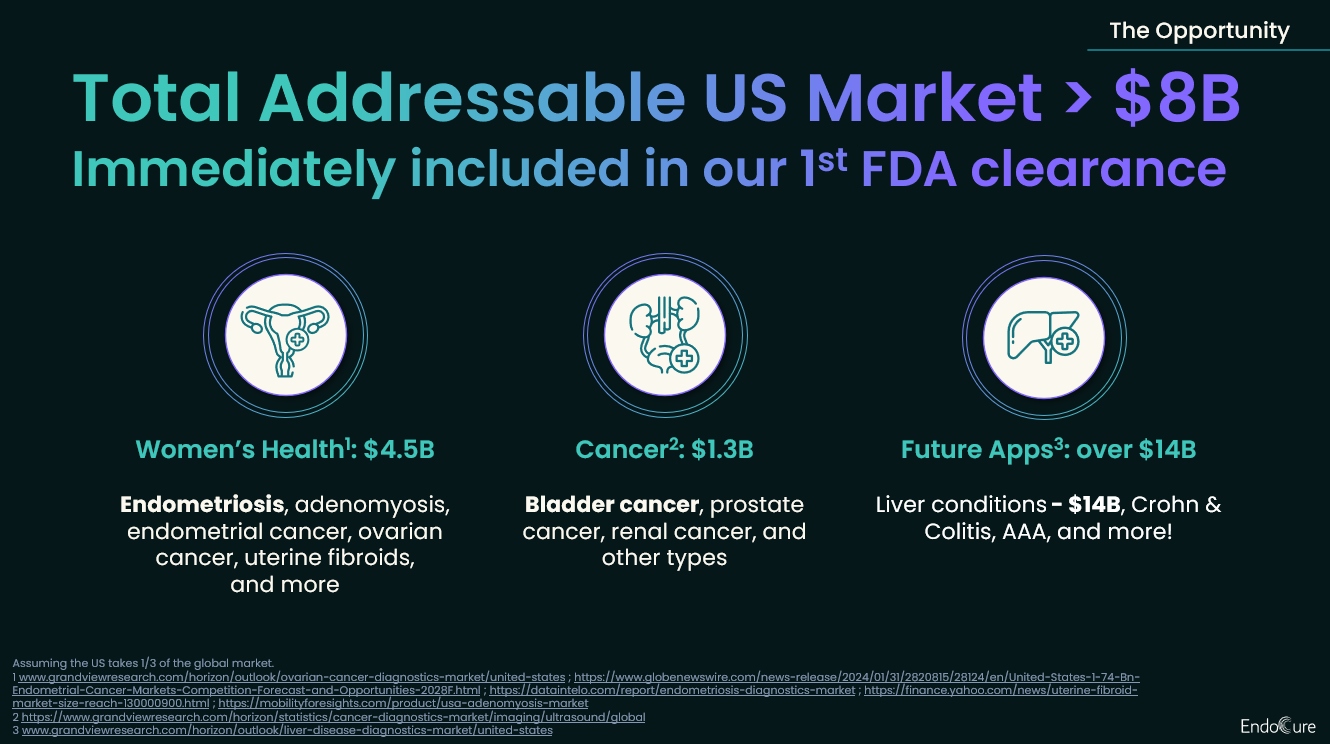

Market Size

Why bottom up beats top down

Your market sizing slide should be broken down into your:

Total Addressable Market (TAM) — The total revenue opportunity if you achieved 100% market share across all potential patients or procedures globally. Total annual procedures or patients × Revenue per procedure or patient.

Serviceable Addressable Market (SAM) — The portion of TAM you can realistically reach given your regulatory clearances, reimbursement coverage, geographic focus, and current product capabilities. Procedures matching your indicated patient population × Revenue per procedure.

Serviceable Obtainable Market (SOM) — The market share you can realistically capture in the next 1–3 years, accounting for sales force build, competitive dynamics, and clinical adoption timelines. SAM × Realistic market share % over the next few years.

This method of calculating these numbers is much preferred to 'top down' market sizing, where you infer total demand from high-level industry reports. This is because VCs want to understand how large your business can actually get. The total cardiac device market might be $75B, the amount addressable might be limited by your specific indication.

It's acceptable (though less desirable) to lean toward top-down if bottom-up is hard to quantify, and to include projected future market sizes (e.g., 2030 structural heart market), so long as it's clearly labeled how you're arriving at those conclusions.

What gets VCs excited

- TAM >$1B with clear, defensible bottom-up math—ideally validated by procedure volume data from CMS claims, hospital discharge data, or published epidemiology

- SOM achievable in 3–5 years representing a $100M+ revenue opportunity

- Market sizing validated by actual physician conversations about their annual procedure volumes and current device spend

- Evidence of market growth driven by structural forces: aging population increasing disease prevalence, shift from open surgery to minimally invasive procedures, expanded indications driven by better outcomes data

- Platform potential where your initial indication opens adjacent anatomies, specialties, or patient populations with your existing device or a next-generation iteration

Red flags

- Top-down only: citing the total cardiovascular device market or total US healthcare spend without procedure-level bottom-up math

- Market size claims that require treating all patients with a condition when your device is indicated for a specific subgroup

- Procedure volume estimates that don't account for the current standard of care—if most patients are managed medically, your addressable surgical or interventional market is much smaller than the total disease population

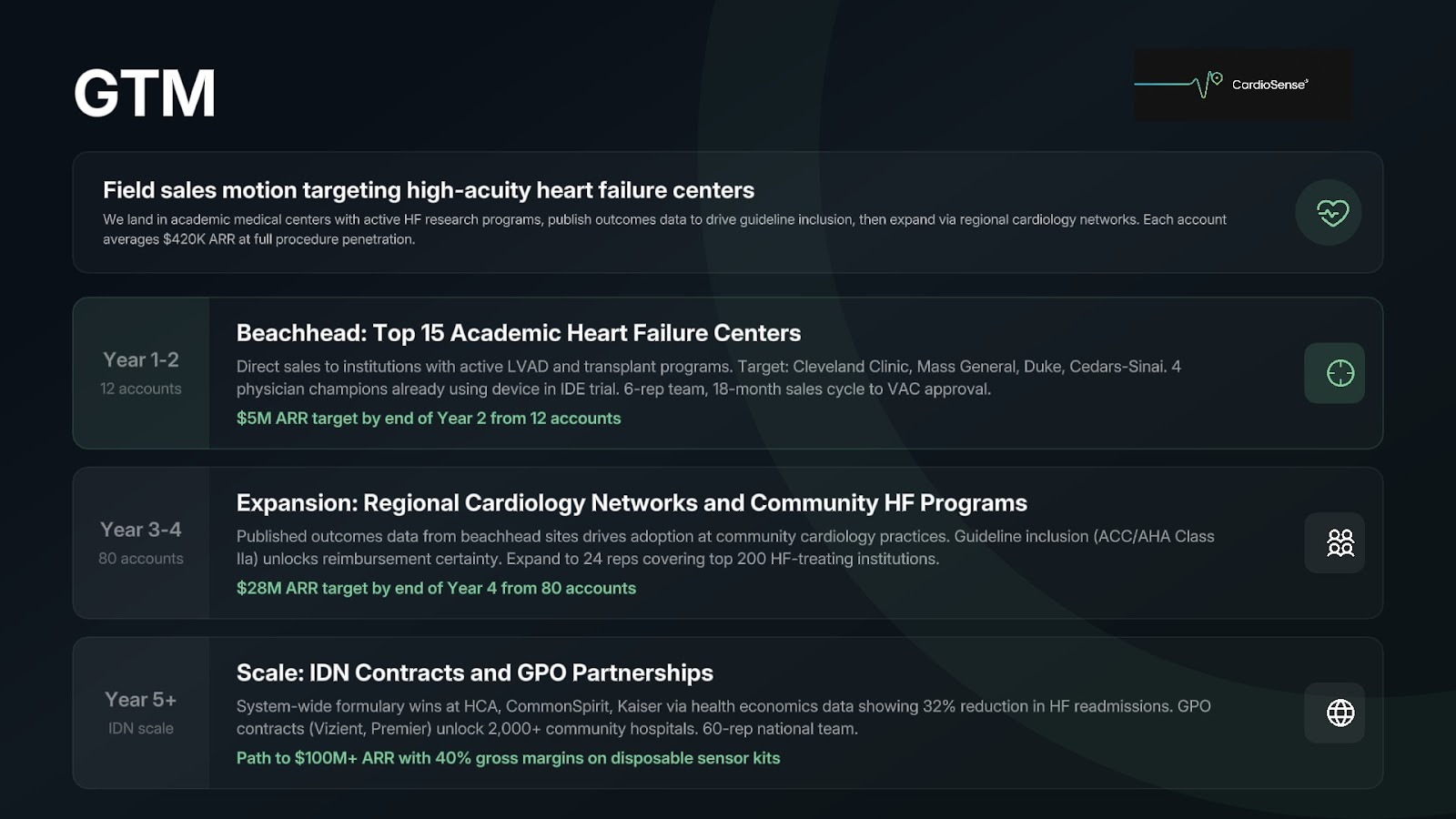

Go to market

Showing you can reach physicians, hospitals, and health systems fast enough

Within the pitch, the most important question to answer is how your GTM motion can support a venture-scale amount of revenue (usually $100M+) within the decade timeframe of a venture fund. VCs will generally use this slide to understand your depth of knowledge on the medical device sales cycle and hospital purchasing dynamics.

VCs will want to talk through:

Customer segmentation and sequencing:

- Initial beachhead: Start with the hospital systems and physicians most willing to adopt new devices—typically major academic medical centers with active IRBs and physicians who are KOLs in the target specialty. These accounts generate the clinical data and peer influence that drive community hospital adoption.

- Expansion path: How do you move from academic medical center KOLs to community hospitals and high-volume private practice groups? What proof points—peer-reviewed publications, society guideline inclusion, payer coverage decisions—are needed to unlock mainstream adoption?

- Health system and IDN timing: When can you sell to integrated delivery networks and national health systems through GPO contracts? What outcomes data and economic analyses are needed to get on a formulary or win a system-wide contract?

This slide should outline who your first, second, and third customer archetypes are, how you reach them, and how your field sales model scales as you move from academic centers to community hospitals to ambulatory surgery centers.

What gets VCs excited

- A clear beachhead with named academic medical centers and physician champions who have used the device and are willing to present data

- A field sales model that matches your device category—direct sales reps for capital equipment, distributor networks for disposables in certain markets, or a hybrid model with clinical specialists supporting early cases

- Pipeline of qualified opportunities at named institutions with active VAC or formulary review processes underway

- KOL physicians willing to evangelize within their specialty society and accelerate peer adoption

- A clear account economics model: revenue per account per year at full penetration, rep productivity targets, and the sales force size required to hit your revenue projections

Red flags

- No clear segmenting and sequencing of customer types—treating all US hospitals as equivalent opportunities

- A direct sales model that requires more reps than your raise can fund before you reach cash-flow breakeven

- Ignoring the role of VACs, GPO contracts, and pharmacy and therapeutics committees in hospital purchasing decisions for your device category

- Sales cycle assumptions that underestimate the time from first physician contact to first revenue-generating procedure

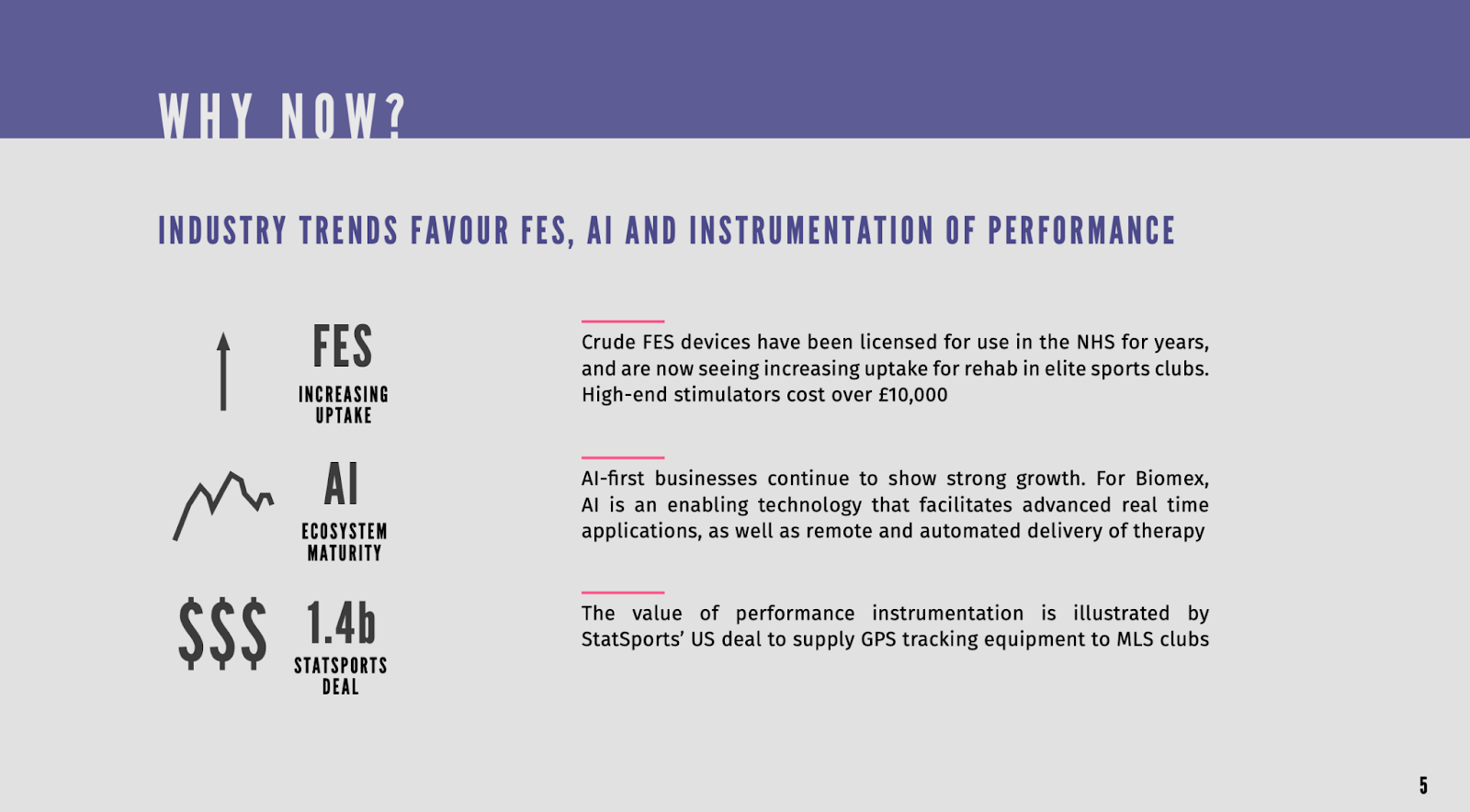

Why Now?

Demonstrating why your device has just become possible to build and sell

Many medical device concepts have been attempted before. After addressing technical and regulatory risk, explain what makes your device uniquely possible now to overcome investors' 'prior failed attempts' concerns.

Inflection points across technology, clinical evidence, reimbursement, and market dynamics create compelling narratives for why your startup is timely. Here are examples we're seeing in 2026:

Technology:

- Miniaturization of sensors, batteries, and wireless communication has enabled implantable and wearable devices that were physically impossible to build five years ago—opening cardiac monitoring, neural stimulation, and drug delivery applications that required components that didn't exist at the required size and power profile

- AI-enabled image analysis and surgical guidance have made it possible to automate decisions that previously required expert physician judgment, enabling less experienced operators to achieve outcomes previously limited to high-volume specialists

- Advanced materials—bioresorbable polymers, shape-memory alloys, hydrogel coatings—have enabled device performance that overcomes the failure modes of first-generation technologies in structural heart, orthopedics, and vascular intervention

Regulatory and reimbursement:

- The FDA Breakthrough Device Designation program has created a faster, more collaborative pathway for devices addressing life-threatening conditions—reducing the timeline from IDE to clearance for qualifying devices

- New CPT codes established for procedures in your category have created the reimbursement foundation that makes your commercial model viable in a way it wasn't three years ago

- CMS bundled payment programs for joint replacement, cardiac care, and oncology are creating financial incentives for hospitals to adopt devices that reduce complications and readmissions—exactly the clinical and economic benefit your device provides

Market dynamics:

- Surgeon shortage and OR time constraints are driving health systems to adopt devices that reduce procedure time and enable shift of care to ambulatory settings—creating demand for your less invasive approach that didn't exist when hospital capacity was less constrained

- Aging population demographics are driving rapid growth in the patient population for your indication—the annual procedure volume in 2030 will be 2–3x the volume today, making market entry now the right time to build the clinical heritage and market position to capture that growth

Your why now slide should speak to the specific changes that have made your business uniquely possible today.

What gets VCs excited

- Specific, quantified changes in enabling conditions ('The miniaturized ASIC we're using became commercially available in 2023 at a price point that makes our implant COGS viable for the first time')

- Confluence of multiple trends making your solution newly viable: technology cost + regulatory pathway + reimbursement foundation + demographic demand

- Evidence that physician willingness-to-adopt has shifted ('Two years ago, interventionalists were skeptical of transcatheter approaches for this anatomy. Now three major centers have published outcomes data supporting the approach and society guidelines are being revised.')

- Recent failures of competing approaches that validate your different mechanism ('First-generation devices in this category failed due to polymer degradation at 18 months; our ceramic matrix composite avoids this failure mode entirely')

Red flags

- Generic claims about the aging population or healthcare cost crisis without showing what specifically changed for your device and clinical indication

- 'Why now' arguments based on regulatory approvals or reimbursement codes that haven't been granted yet

- Ignoring why previous devices in your category failed clinically or commercially and how your approach avoids those failure modes

- Over-reliance on a single reimbursement code or CMS policy that could be modified in a future rule-making—without showing the clinical evidence supports the device value independently

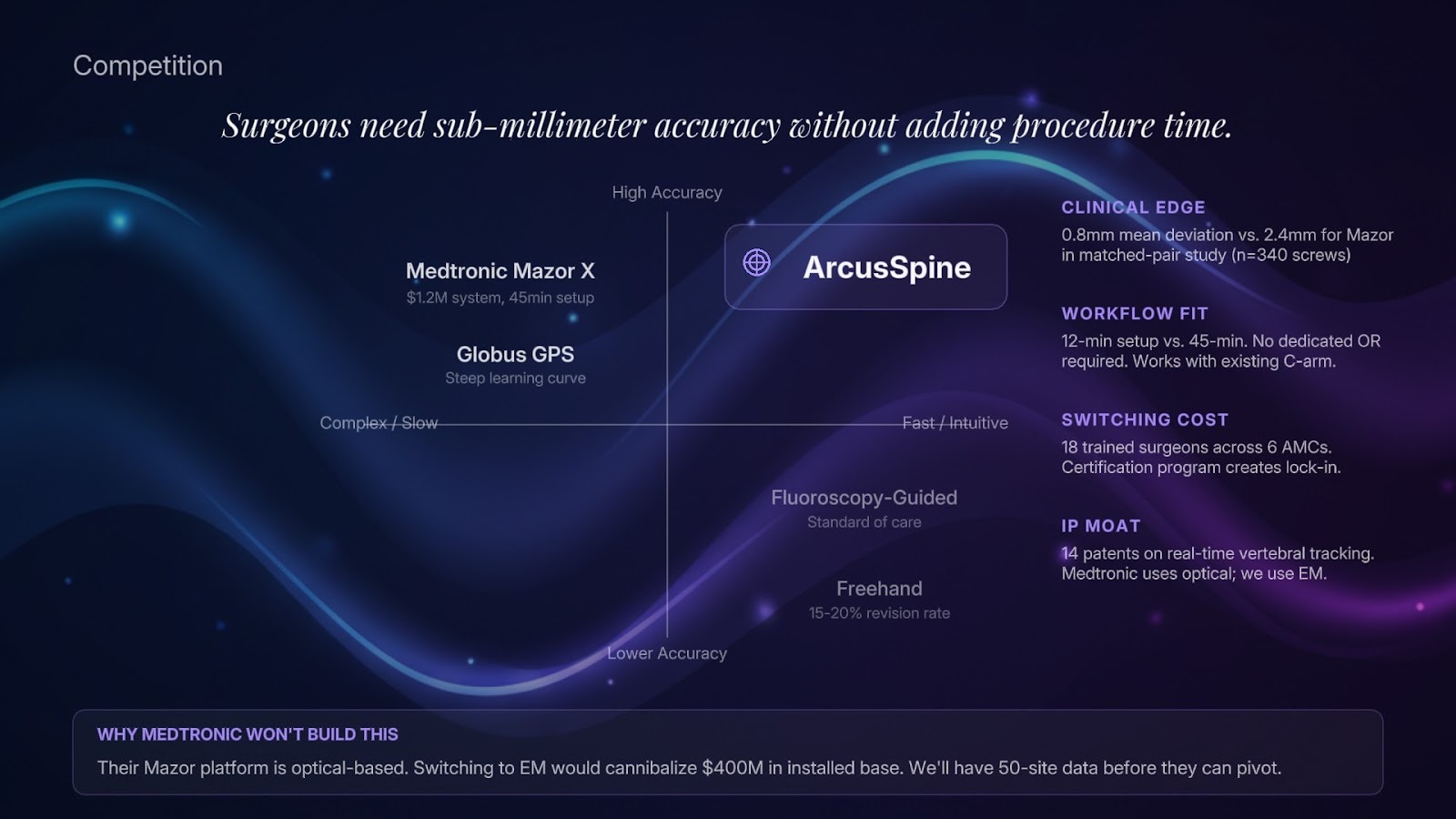

Competition

Who are your competitors, and how do you demonstrate clinical and commercial defensibility

Your competition slide serves to show how you beat out incumbent methods of care, incumbent product lines, and potential new entrants.

Medtech competition is multi-dimensional. You're competing against: (1) the current standard of care (medication, open surgery, watchful waiting), (2) established medical device companies with existing hospital contracts and physician relationships, (3) other early-stage device companies in your category, and (4) physicians choosing not to change their practice. Your competitive positioning must address all four.

Addressing large company risk:

VCs will ask: 'Why won't Medtronic / Abbott / Boston Scientific / Stryker build this or acquire a competitor?' Your answer must show:

- A mechanism of action or technology platform that is fundamentally different from their existing product lines—not just a next-generation iteration of what they already sell

- A market segment they're not currently serving well, or a patient population they've historically ignored

- A speed advantage: you can run a clinical study and reach the market before they can redirect their R&D resources, and by the time they can build it, you'll have the clinical data, physician relationships, and market position that make you the acquisition target rather than the victim

Tied to immediate competitive advantage, is building a story as to why you will maintain defensibility over time.

Defensibility can emerge from:

- Clinical data and outcomes record: Every patient treated, every publication, every conference presentation builds the evidence base that physicians need to switch and maintain their current practice pattern with your device. First movers with a strong clinical record are difficult to displace. Superior efficacy enables physician lock in.

- Physician training and certification: If your device requires structured training and certification to use effectively, the physicians you certify first become embedded adopters who are resistant to retraining on a competitor's device.

- Proprietary technology and IP: Novel mechanisms of action, material compositions, delivery system architectures, or sensor modalities protected by patents. In medtech, IP protection combined with clinical data creates the strongest defensibility.

- Surgeon or interventionalist preference: In discretionary procedure categories, physician preference drives device selection. Building a strong preference position through superior ergonomics, reliability, and clinical outcomes creates switching costs that purchasing committees find difficult to override.

Your competition slide should describe why you are better than incumbents and potential entrants across factors that matter to physicians. In conversation, VCs will use it to talk about incumbent risk and broader defensibility.

What gets VCs excited

- Demonstrably superior clinical outcomes on a primary endpoint that matters to physicians and payers

- Physician champions at major academic centers who are opinion leaders in the target specialty and who actively advocate for your device in their training programs and publications

- Patent portfolio covering the core mechanism of action, device architecture, and key manufacturing processes

- First-mover advantage in a new clinical indication with an IDE already approved and enrollment underway

- A device category where physician preference is the dominant purchasing driver

Red flags

- 'No competitors' or 'we're first'—there's always competition, including the standard of care and physician inertia

- Competitive differentiation based only on a single performance metric without addressing total clinical and economic value

- No clear answer to why Medtronic, Abbott, or Boston Scientific won't build or acquire a competing device if your approach proves out clinically

- Differentiation that requires physicians to accept meaningfully more clinical risk or procedural complexity to achieve a benefit that is marginal relative to existing options

- Assuming that FDA clearance alone will drive physician adoption—clearance is a prerequisite, not a commercial strategy

Team

What makes for a world-class medtech founding team?

At Julian Capital, we’ve written about what makes a great founding team here. We're excited by founding teams who are:

- Commercially minded with technical depth

- Building their life's work—the culmination of their career or their final pursuit

- Ambitious enough to scale to $1B+ valuation

- Relentlessly resourceful with high agency

- Persuasive and authentic storytellers

- Comprehensive in thinking through all business avenues (GTM, competitive landscape, bottom-up TAM, etc.

Medtech founders come from diverse backgrounds—interventional cardiologists and surgeons, biomedical engineers from large device companies, regulatory affairs specialists, clinical research scientists, and prior medtech founders. The common thread among great founding teams is understanding that regulatory strategy, clinical evidence generation, and commercial execution are as important as the device itself.

These specific roles on the founding team give VCs confidence:

- Clinical domain expertise: At least one founder—or a very closely engaged physician co-founder or chief medical officer—with deep expertise in the target specialty. They should be able to specify the clinical requirements, critique the device design, and attract the KOL relationships that drive early adoption. In many successful medtech startups, a physician co-founder's clinical practice becomes the first human use site.

- Medical device engineering experience: Someone who has taken a device from concept through FDA submission and commercial production. Understands design controls, verification and validation, design history file documentation, and what FDA reviewers look for in a 510(k) or PMA submission. This is not a role that can be outsourced entirely to a consulting firm.

- Regulatory and clinical affairs expertise: Deep understanding of FDA classification and clearance requirements, IDE study design, clinical data requirements for the target indication, and the reimbursement pathway. Ideally someone who has been through an IDE trial and a PMA submission before.

- Commercial and market access capability: Someone who understands hospital purchasing dynamics, physician adoption economics, GPO contracting, and reimbursement strategy. Doesn't have to be a founder, but the team needs commercial orientation from the start—the biggest mistake medtech startups make is treating commercialization as something to figure out after FDA clearance.

Of course, not all of these are necessary on a founding team. Your team slide should showcase the skillsets and prior experience you bring that are relevant for bringing your business off the ground.

What gets VCs excited

- Teams that combine clinical domain expertise, medical device engineering experience, and regulatory and commercial orientation

- Founders who have successfully developed and commercialized a device before—even in prior companies or roles at large device companies

- A physician co-founder or chief medical officer who is an active clinician in the target specialty with existing KOL relationships

- Track record of navigating FDA interactions: Pre-Sub meetings, IDE submissions, 510(k) clearances, or PMA approvals

- Commercial leadership with experience in medtech field sales, health system contracting, or reimbursement strategy

Red flags

- Teams without anyone who has developed and submitted a medical device to FDA before (can be overcome with an advisor or proof of work with a 3rd party for FDA approval)

- Physician founders who are not connected to active clinicians in the target specialty

- Engineering teams from non-medical industries who underestimate the design control, biocompatibility, and quality system requirements of medical device development

- Lack of commercial orientation—founders who view FDA clearance as the finish line rather than the starting line

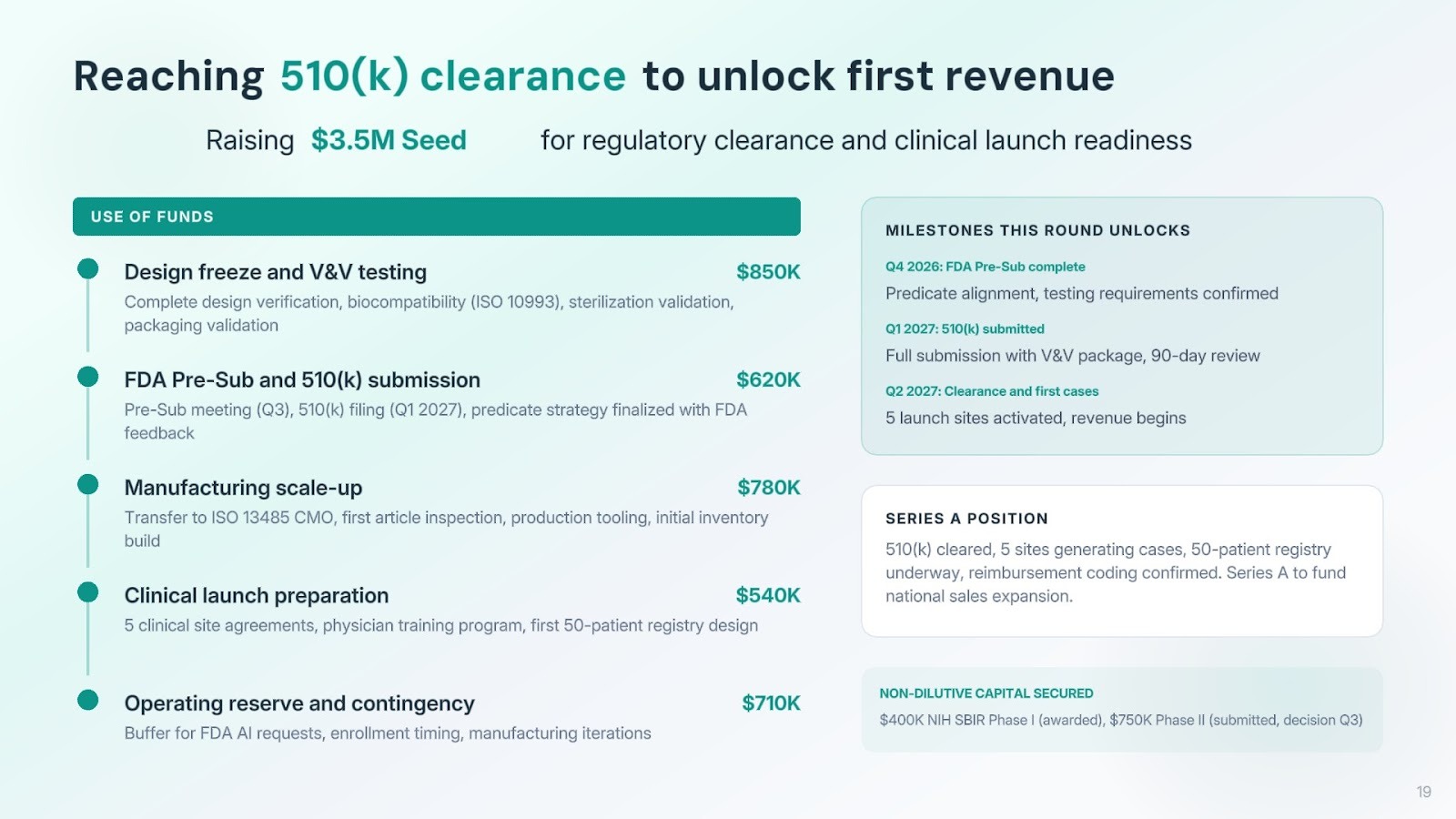

The Ask: Use of proceeds and round size

The ask shows how much you are raising and what you plan to accomplish with it. We wrote about choosing how much to raise here.

Medical device development is capital-intensive—device iteration, bench testing, animal studies, biocompatibility testing, clinical studies, manufacturing scale-up, and regulatory submissions all require capital before a dollar of revenue arrives.

This slide should show the amount you’re raising, and the specific outcomes (by means of technical, regulatory, manufacturing, and commercial progress) you aim to achieve with it.

What gets VCs excited:

- Raise sized to specific clinical or regulatory milestones: IDE submission, first-in-human completion, pivotal trial enrollment completion, or 510(k) clearance

- Clear articulation of what de-risking the next round requires—and why the milestones this raise funds are the right ones to get there

- Evidence that non-dilutive capital (NIH SBIR, NSF, BARDA, state medical device grants) has been pursued or secured to extend runway

- Use of proceeds that maps directly to the device iterations, testing campaigns, clinical site activations, and regulatory submissions needed to hit stated milestones

- A realistic contingency for enrollment delays, FDA additional information requests, and manufacturing iterations—the three most common sources of medtech schedule overrun

Red flags:

- Raise sized by 'how long we can survive' rather than 'what we need to prove to reach the next financing milestone'

- No clear milestone that the funding unlocks—just generic 'product development and regulatory clearance'

- Underestimating IDE study costs, CRO fees, clinical site activation timelines, and the cost of FDA submission preparation

- Assuming that enrollment will proceed at projected rates without buffer for site activation delays, IRB timelines, and patient eligibility rates

- Treating reimbursement strategy as a post-clearance problem when it should be funded and underway before your pivotal trial completes

Pitching: Do's & Don'ts

The best pitches are conversational. Answers should be succinct yet demonstrate depth of thought.

Great medtech founders bridge clinical vision with regulatory and commercial pragmatism. They intimately understand the clinical problem and the physician's decision-making process, and can explain both the device and the path to market clearly. They understand the reimbursement landscape and can explain why their device creates value for health systems, not just patients.

Do

- Be honest about where you are in the regulatory process: VCs appreciate realism. 'We've had a Pre-Sub meeting with FDA and they've aligned on our 510(k) pathway with the predicate we identified, but flagged that they'll want a 30-patient biocompatibility study completed before clearance' is far more credible than a vague claim that you're on a 510(k) pathway.

- Have strong answers on reimbursement: You should be able to walk through the specific CPT or DRG codes that apply to your procedure, the current reimbursement rates, the economic value proposition for the hospital at your ASP, and your strategy if coverage gaps exist.

- Demonstrate physician intimacy: Drop specific details that show you deeply understand your target clinician: 'Interventional cardiologists in high-volume cath labs are seeing 8–12 severely calcified lesions per week that they currently manage with atherectomy at a 30% residual stenosis rate. Our device addresses the 40% of those cases where atherectomy alone is inadequate.'

- Address the 'why now' directly: Proactively explain what has changed—in technology, reimbursement, FDA policy, or clinical evidence—that makes your device viable and your business timely.

- Acknowledge and address large company risk: Don't wait for VCs to ask 'Why won't Medtronic build this?' Address it upfront with a credible, specific answer that shows you've thought through their product roadmaps and R&D priorities.

- Lean in on your clinical data: At the early stages, clinical evidence is a driving decision factor. Show your bench data, your animal data, and your first-in-human results. Be specific about what each dataset demonstrates and what remains to be proven.

Don't

- Lead with the mechanism of action before the clinical problem: Focus on what your device does for the patient and the physician, what it costs the health system, and why the market will pay for it. Dive deeper on the device engineering when prompted to.

- Overclaim your clinical data: Every medical device company has limitations in its early clinical evidence. Be specific about your study design, patient numbers, follow-up duration, and what the data does and doesn't show.

- Dismiss competition from established device companies: Acknowledge competitors—including the current standard of care and large company products—and explain your differentiation with specificity. 'We're better because we're smaller and more innovative' is not an answer.

- Ignore reimbursement: If your team hasn't engaged a reimbursement consultant and doesn't have a clear view of the coding and coverage landscape, investors will notice. Reimbursement is as important as FDA clearance for commercial success.

- Underestimate the commercialization timeline: FDA clearance is not revenue. The time from first clearance to meaningful commercial scale is typically 18–36 months in medtech. Build your projections to reflect that reality.

We hope this guide was useful to you! If you'd like to get in touch, don't hesitate to reach out to Julian.Capital, SOSV, and apply in <1 minute to get put in touch with thesis fit investors for free at DeepChecks.VC.