Want to know exactly how VCs evaluate your energy startup?

Together with Lowercarbon, Voyager, and Climate Capital — some of the leading energy VCs— we’ve built this guide to unpack the inside baseball on how VCs evaluate energy startups, and in turn how you can raise a successful round.

Informed by the thousands of decks we’ve reviewed, and insights on which startups get the most traction on Deep Checks, this playbook helps put together a teaser deck that gets your first VC pitch scheduled.

We’ll go slide by slide on how investors decide whether or not to move forward with a startup. It’ll cover:

- Problem: Demonstrating you’re solving a burning pain point for your customers

- Solution: Show why you have the best solution to this problem

- Technical risk: How to convince investors to get behind the remaining technical risk that you have

- Traction: How to show there’s demand for your product before the market has adopted it

- Business Model: How VCs think about your economics

- Go to market: Showing you can become big enough, fast enough

- Why now?: Demonstrating why your startup has just become possible to build. This is make-or-break for many pitches

- Market Size: Why bottom up beats top down

- Competition: Who are your competitors, and how do you demonstrate defensibility

- Team: What makes for a world-class founding team?

- The Ask: Use of proceeds and round size

- Pitching: Do’s and dont’s of pitching your startup to VCs

Problem

Demonstrating you’re solving a burning pain point for your customers

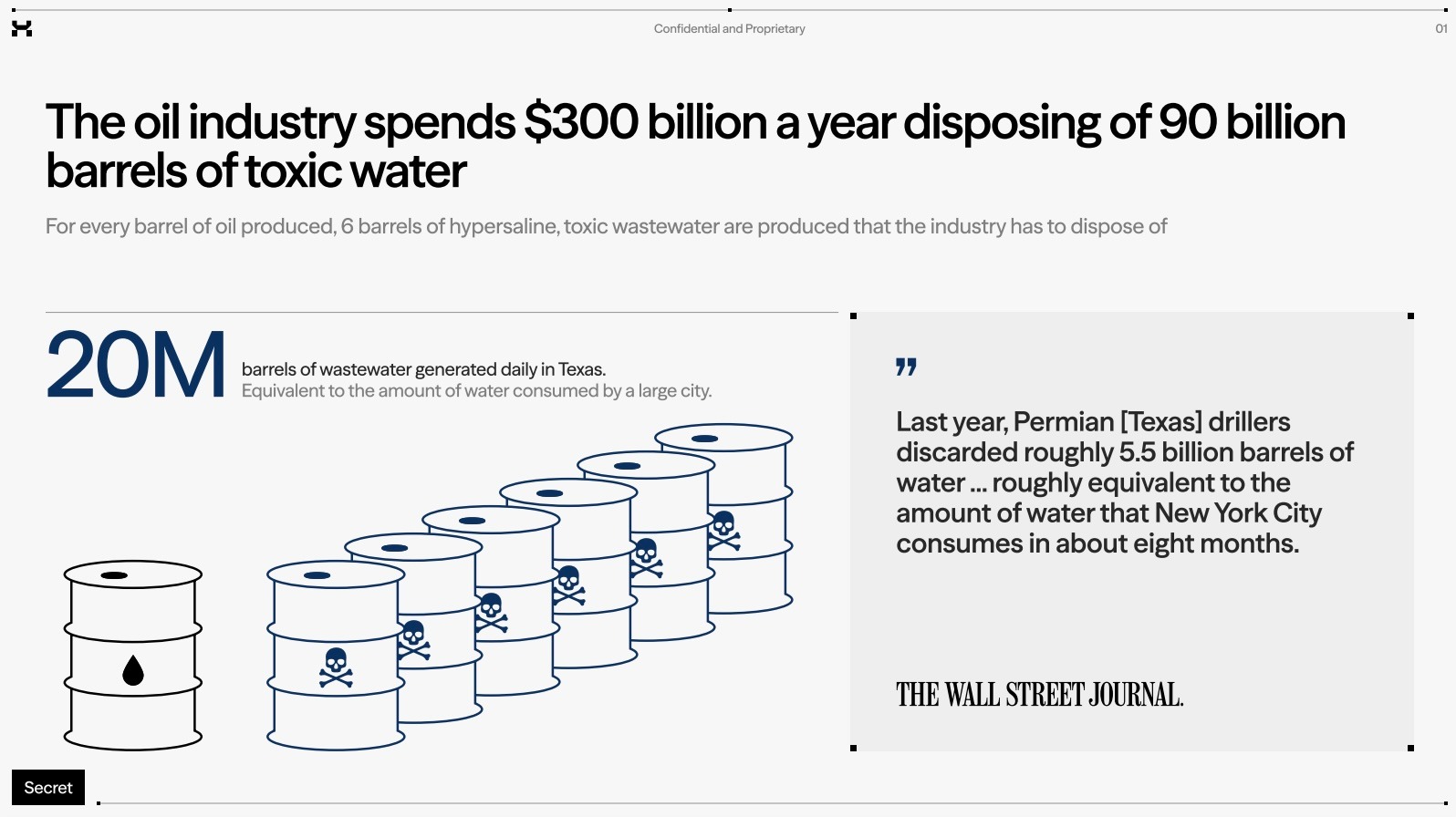

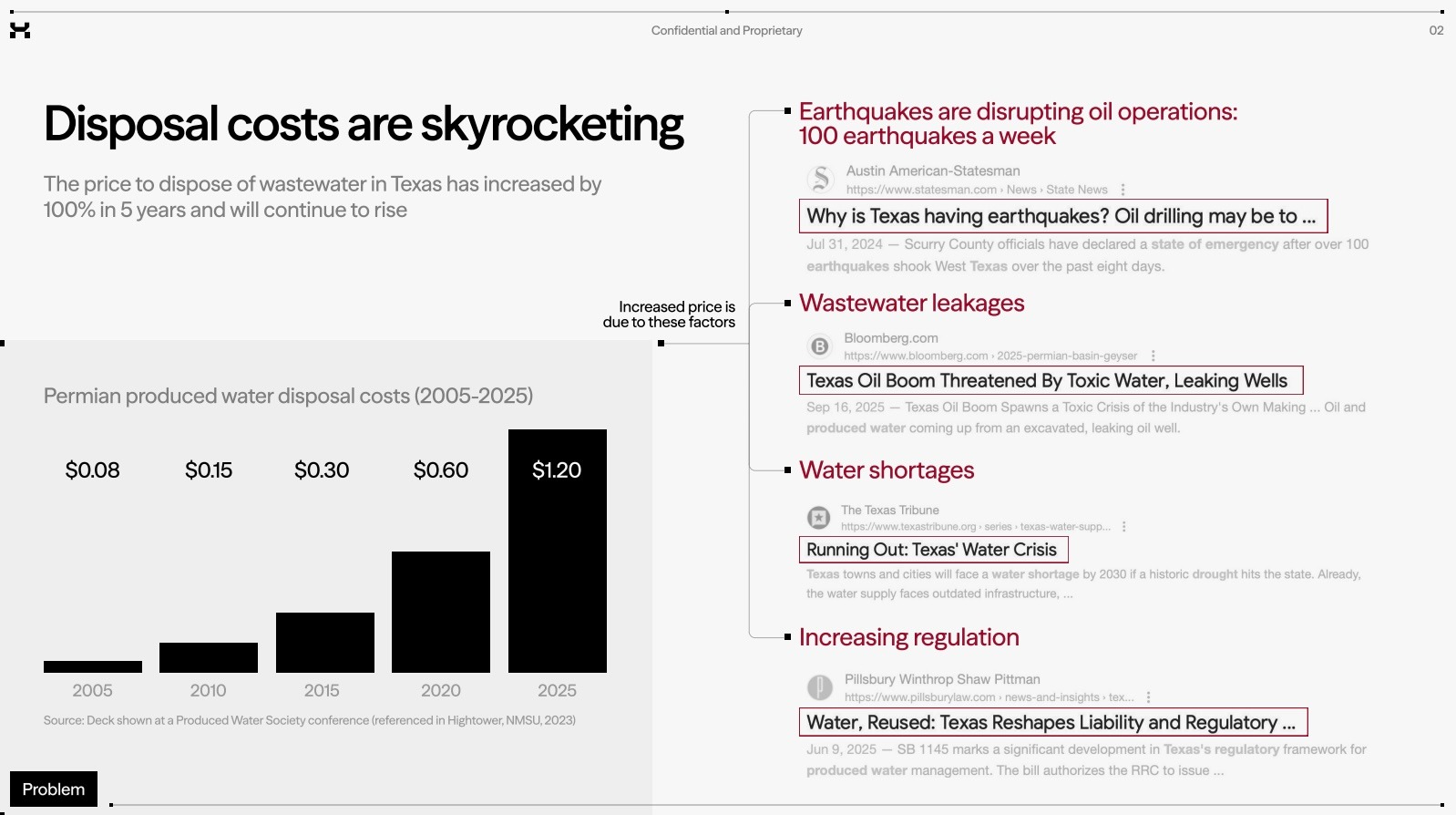

The problem slide exists to convince VCs the pain point you’re solving for your customers is a large, distinct, burning issue that they are willing to endure switching costs to solve.

In energy, the challenge isn't proving customers want your product— there are distinct energy needs across the market. The real question is whether you can productize, sell, and execute your solution effectively.

In describing the problem, it’s important to note that energy customers have unique purchase dynamics that can make sales complex.

Interoperability — Your product must work within an ecosystem of grid technologies and actors. A smart EV charger, for instance, needs to coordinate with your home's power draw, solar panels, other devices, and grid pricing. You need to understand how you fit into this web and demonstrate it clearly.

Utility sales cycles — Utilities operate differently than typical businesses. Sales can require navigating complex approval processes, grid studies, and interconnection queues. Even if you aren't selling directly to a utility, knowing how you interact with them will help you address the interoperability challenge.

Ask yourself: are you solving a clear bottleneck, or offering a marginal economic benefit?

Frame the problem in terms of customer business challenges, not technology gaps. And show how your solution fits into customers' existing business holistically.

How to show this:

In your deck, start with a slide that outlines the general industry challenge you're addressing, then follow with a slide on the specific problem your end customers face.

What gets VCs excited:

- Problems where the economic pain is quantifiable and large

- Problems that are getting worse over time (growing electricity demand from data centers and electrification, aging grid infrastructure, increasingly extreme weather), leading to a growing market size

- Evidence that customers are currently using expensive or inadequate workarounds (diesel backup, manual load shedding, purchasing carbon offsets instead of reducing emissions)

- Multi-stakeholder pain that spans operations, finance, sustainability, and compliance teams simultaneously

Red flags:

- Problems framed around policy mandates alone without underlying economic drivers (policy can change—economics are durable)

- Technology-first framing (“Our novel electrochemistry”) rather than customer-outcome framing

- Generic statements about climate change without specific customer validation or quantified impact

- Problems that only matter at massive scale or require full system transformation before your solution creates value

- Conflating the overall energy transition with a specific customer pain point—“the world needs clean energy” is not a problem slide

- A shallow problem statement that simply says, “there’s an energy shortage” without any additional context on the specific problems faced by your customers.

Solution

Show why your solution is the best solution to this problem

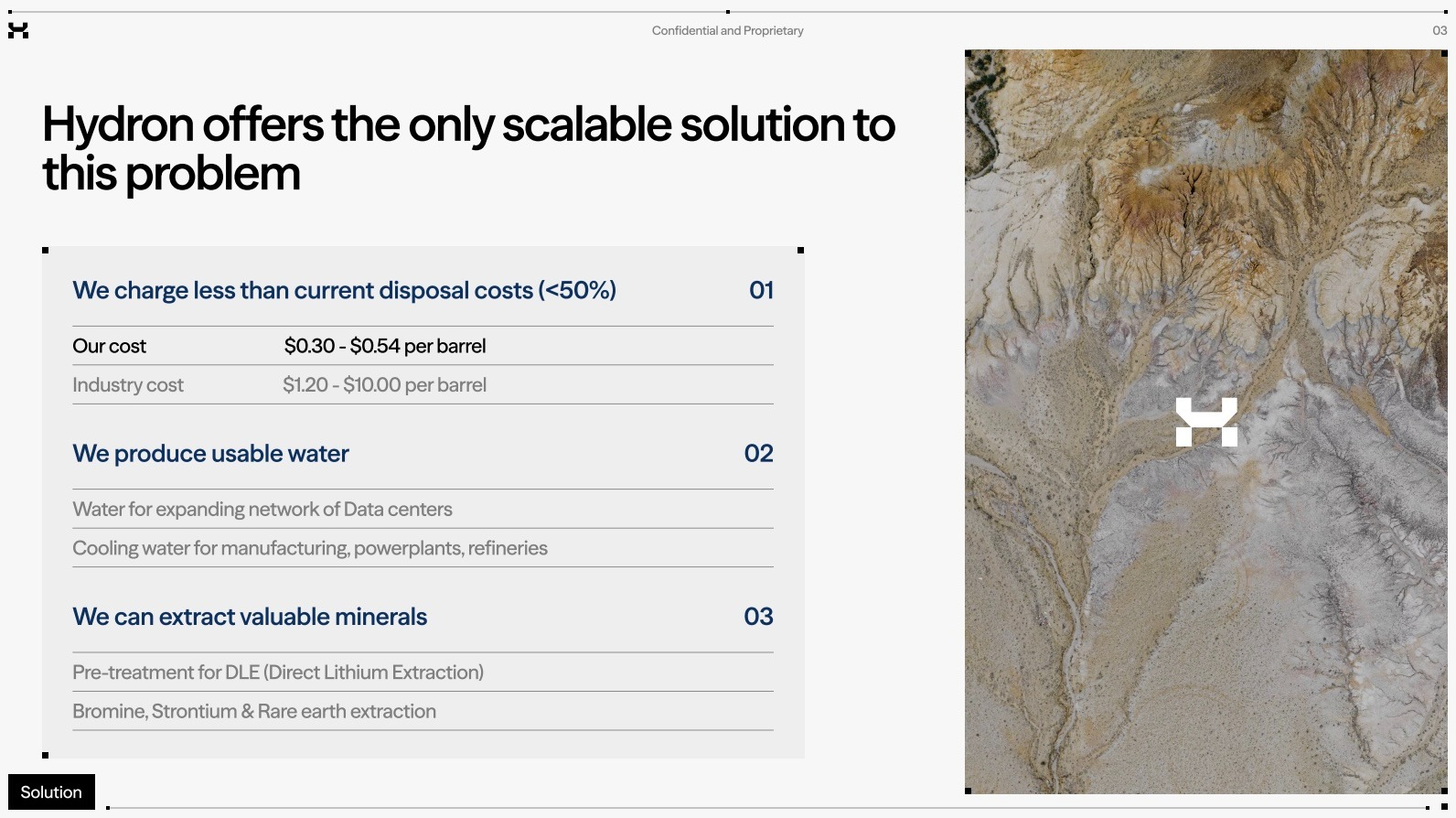

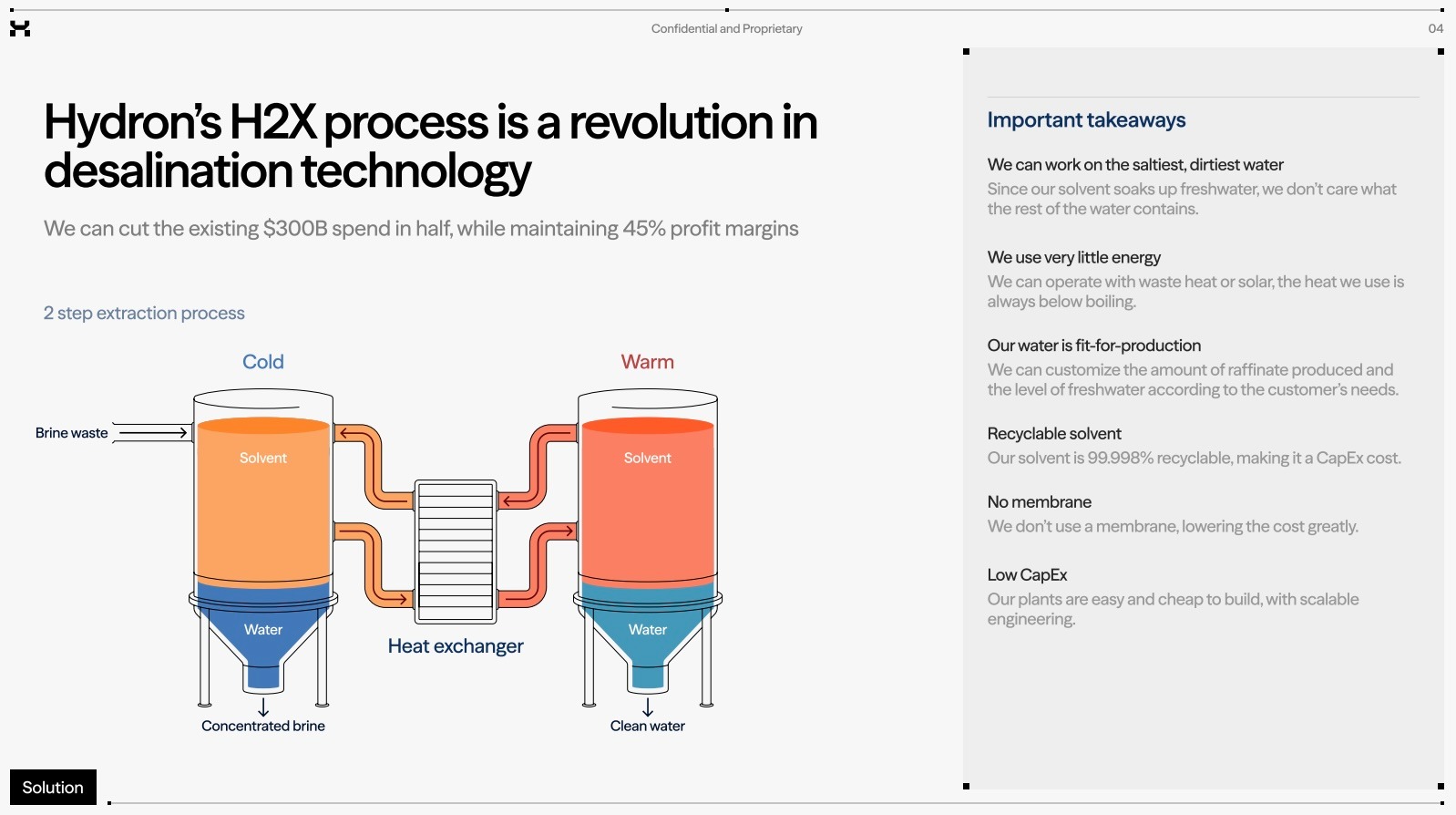

The solutions slide demonstrates why you have the best solution to the problem your customers face.

Effective solution slides show how your technology translates to customer business outcomes. For example:

- Quantified cost advantage: “Delivers firm, dispatchable clean power at $55/MWh” rather than “85% round-trip efficiency with 200-hour duration.” Translate your technical specs into the units your buyer cares about: levelized cost of energy, dollars saved per facility per year.

- Direct economic comparison: “Reduces customer energy costs by 30%, payback in 2.5 years” with clear assumptions.

- Deployment simplicity: “Installs in 8 weeks using existing electrical infrastructure, no facility modifications required.” Show that your solution fits into existing workflows, permitting timelines, and physical infrastructure.

- Performance durability: “20-year design life with <1% annual degradation, warranted performance.” Show durability, degradation curves, and maintenance requirements that align with buyer expectations.

In showing why you have the best solution, you must address why your approach is better than: (1) the incumbent technology (natural gas peakers, diesel generators, conventional heat), (2) other emerging solutions in your category, and (3) doing nothing or waiting for technology to mature. These can be implied by the distinct benefits of your technology.

What gets VCs excited

- Clear levelized cost advantage over incumbents, with a credible path to further cost reduction at scale

- Solutions that address multiple value streams simultaneously (e.g., energy storage that provides both peak shaving and grid services revenue)

- Technology that gets better or cheaper with each deployment (learning curves, manufacturing scale, software optimization)

- Demonstrating an understanding of the sales cycle in the beachhead market

Red flags

- Payback periods over 5 years without strong contractual certainty (energy buyers have shorter planning horizons than asset life might suggest)

- Leading with technical specifications absent showing business value

- Comparing only to legacy systems without addressing why other emerging competitors don’t solve this equally well

- Assuming perfect policy environments or maximum available tax credits

- High risk in deployment requirements (permitting timelines, interconnection)

Technical risk

How to convince investors to get behind your remaining technical risk

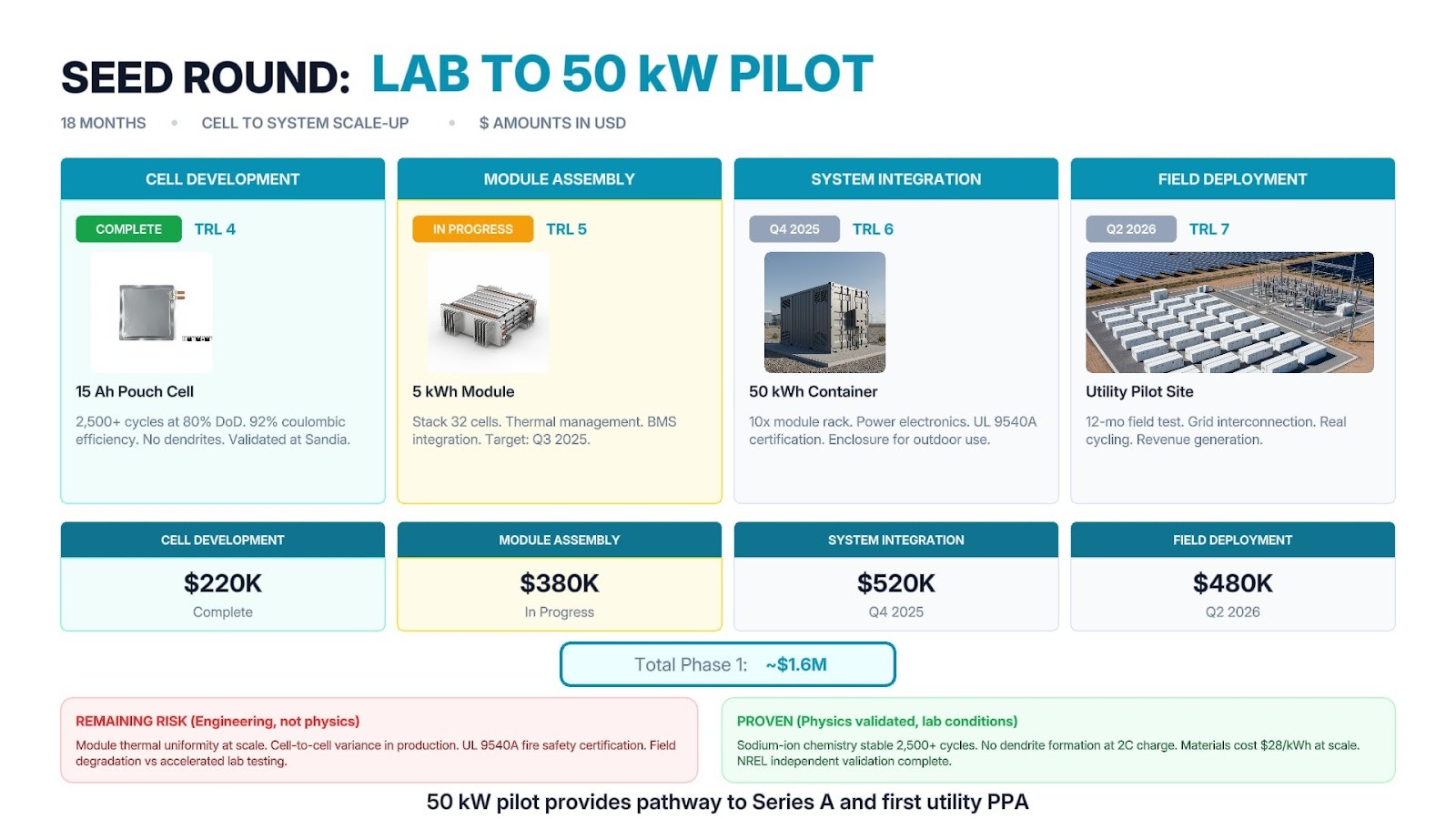

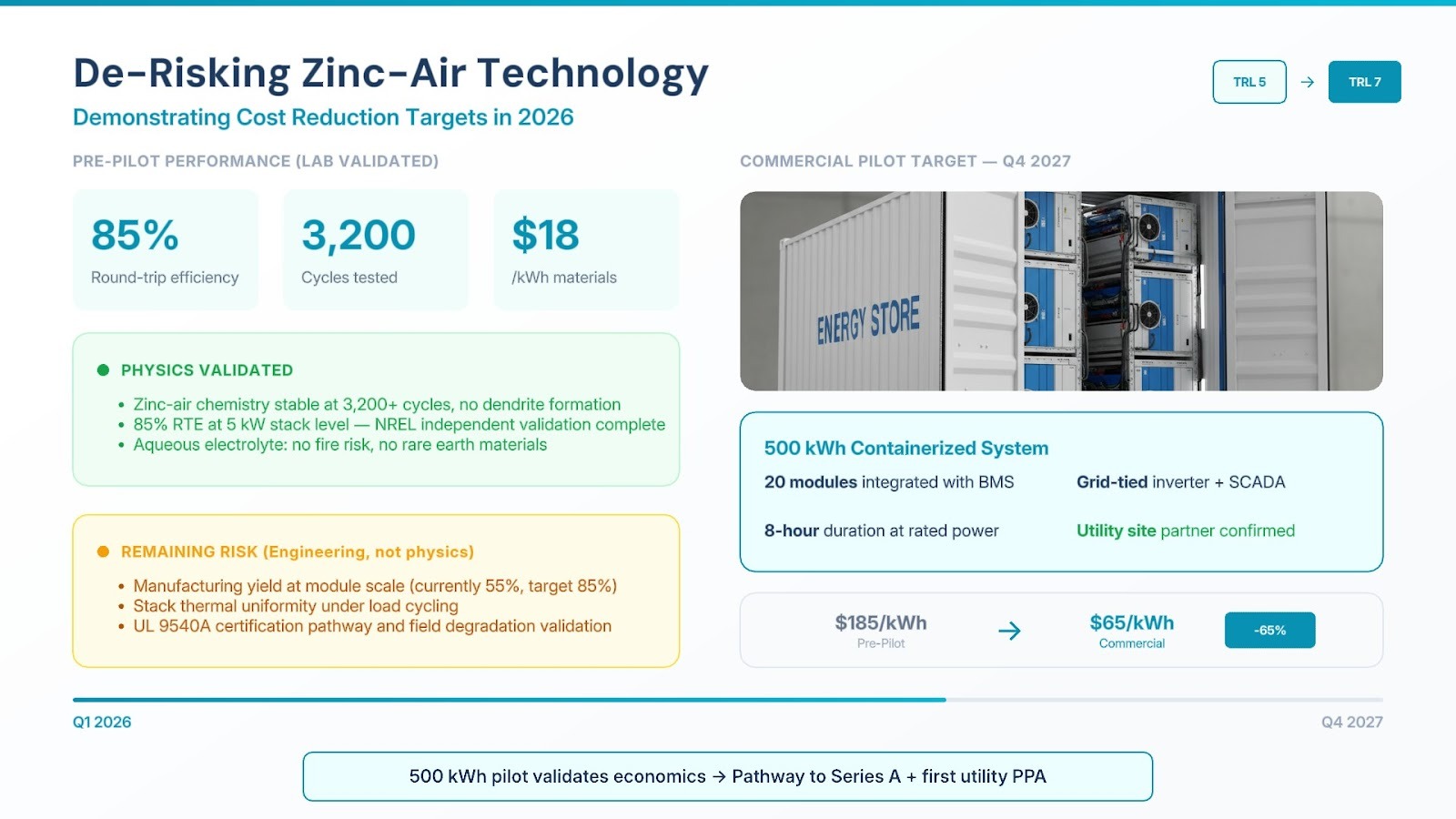

Your technical risk slide helps show what has been de-risked, and what remaining steps are needed to reach commercial scale.

Deeptech venture investors typically accept engineering risk (technically feasible engineering work) but not scientific risk (your solution requires scientific breakthroughs to work as expected). Early stage VCs want to know:

- What has been proven

- What needs to be proven (within technical efficacy, system efficiency, technoeconomics, or scale-up)

- Why you're confident you'll achieve this

The key question investors want to understand is if your technology will work at scale, at your projected economics. These are some areas they will want to talk through in this section of the deck:

- Sequenced milestones that show you understand how each stage unlocks the next, with explicit system improvements and scale-up risks identified

- Projected system economics at each future stage: And which customer segments will pay for each price point

- Speed of iteration demonstrated through your current progress and future development plans

- Clear capital requirements mapped over time

- Core technology validation: Has the core chemistry, physics, or engineering principle been validated at a meaningful scale? Is scaling up a means of known optimization problems, or novel technical development?

- Manufacturing and scale-up risk: Can your technology be manufactured at cost and quality?

- System integration risk: Energy systems don’t operate in isolation—they connect to grids, industrial processes, and buildings. Can your system integrate with existing infrastructure?

- Durability and degradation risk: Will your technology perform reliably over 10–25 year asset lives?

- Permitting and certification risk: What permitting needs do your customers have to sell into them (ie UL), what gives you confidence in securing this?

The technical risk slide won’t cover all of this, but you can lay a strong baseline to talk atop with technical diagrams, your TRL level, and highlight any remaining customer benefits not covered in the solution slide.

What gets VCs excited

- Paid pilots with documented performance data

- Clear delineation between engineering risk (solvable with known methods) and scientific risk (might not work)—with your remaining risk firmly in the engineering category

- Proprietary technical insights or IP that provide a fundamental advantage, not incremental improvement

- A credible manufacturing cost roadmap showing how you get from current prototype costs to commercial-scale economics

Red flags

- Lab scale performance with no path to commercial scale

- Core technology relying on undiscovered materials or unproven physics

- Scale-up plans that skip intermediate steps (going from bench-scale directly to GW-scale manufacturing)

- No discussion of degradation, failure modes, or performance under real-world variability

- Long list of remaining technical milestones without clear prioritization or funding alignment

- Dismissing manufacturing complexity

- Unrealistic system performance specs, scale-up risk that engineering can't address, ignoring costs to reach market, multi-year iteration times to reach version one, and remaining scientific risk in core functionality.

Traction

How to show there’s demand for your product before the market has adopted it

The traction slide demonstrates how far you’ve come across your business goals before heading into the fundraise. It helps VCs understand your pace and capability of execution.

In order of least to most convincing, there are four ways you can demonstrate your traction to VCs, in order of most to least impactful:

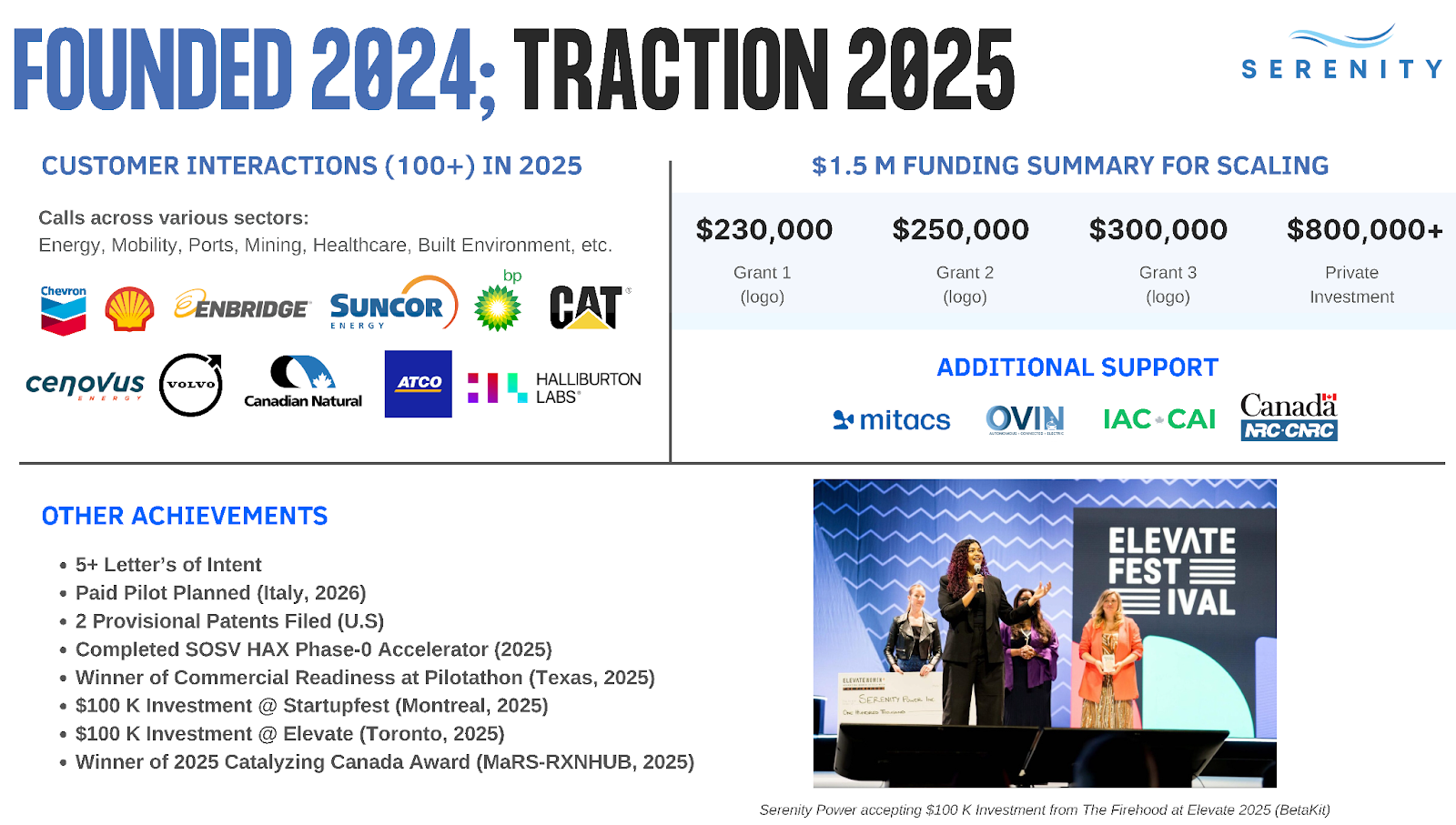

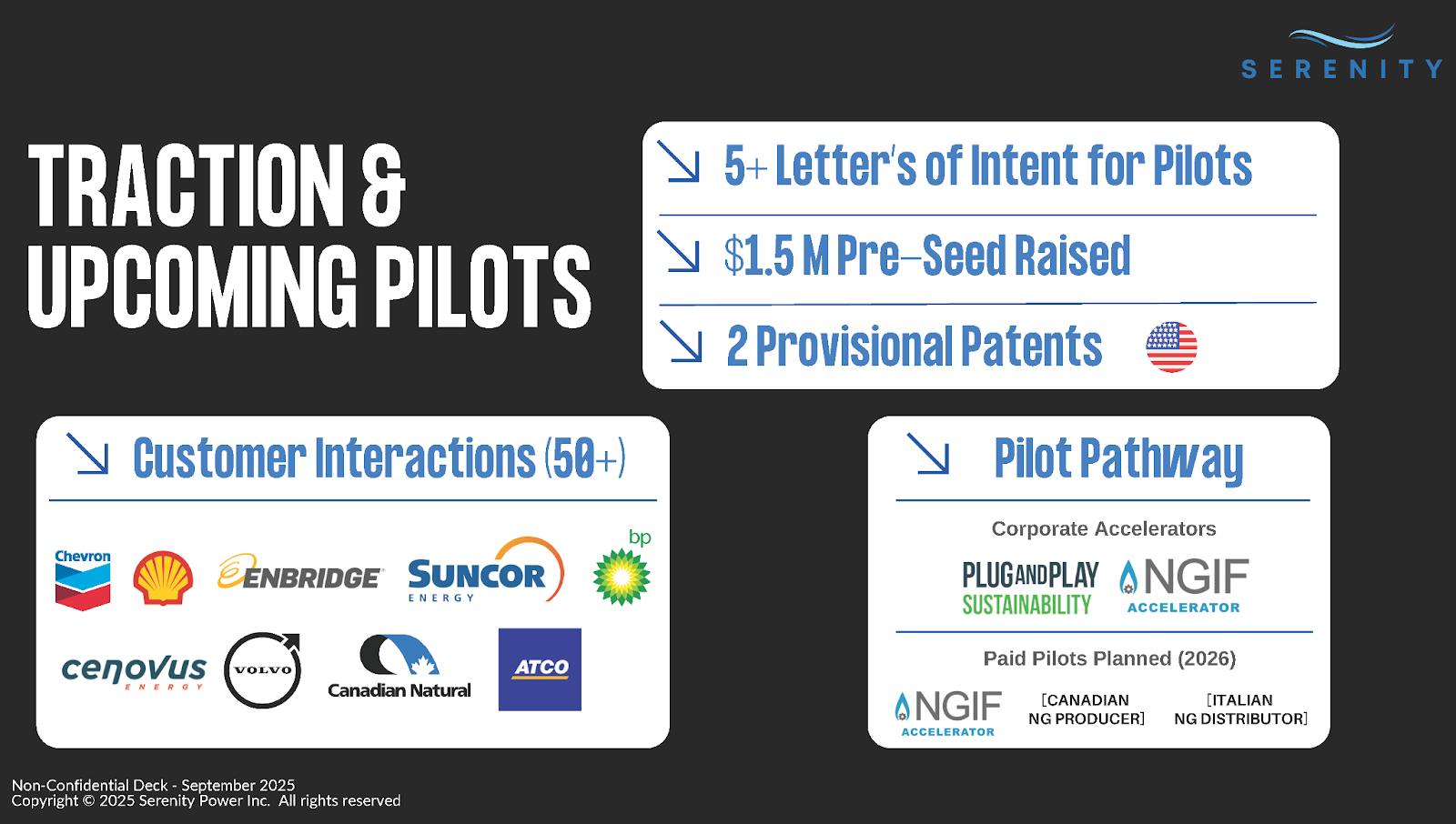

Pilot deployments (most valuable): Energy systems operating at a customer site or grid-connected facility.

Design partnerships: Utility or industrial co-development where they’re investing resources: site access, engineering support, data sharing, grid interconnection assistance.

Letters of intent (LOIs): For energy, LOIs must include specific conditions, volumes, and pricing frameworks. “Will purchase 10 MWh of storage systems upon demonstration of 90% round-trip efficiency over 500 cycles” is strong. “Interested in exploring clean energy solutions” is not. Include: the buyer’s name and role, the specific product configuration, success criteria, and projected pricing.

Customer discovery depth: For pre-product companies, show 30–50+ customer conversations across your target verticals. Document specific pain points, willingness-to-pay thresholds, purchasing processes, and success criteria. Include details like: Who’s the economic buyer vs. technical evaluator? What’s the approval process? What ROI threshold triggers a purchase decision? What are their current alternatives and costs? This level of detail won’t fit on a slide, but is a great material to have as a separate doc or to be able to talk to during calls.

Your traction slide should demonstrate how far along this spectrum you’ve gotten. At minimum for the seed stage, investors will generally want to see a functional prototype and LOIs. You should use it to show off all progress you’ve made, and can include other accomplishments like IP filed.

What gets VCs excited

- Systems operating at customer sites with documented performance data matching or exceeding design specifications

- Customers paying something—even subsidized rates—for pilots

- Evidence of expanding scope: customers requesting larger systems, additional use cases, or multi-site deployments

- Inbound interest from customers who weren’t specifically targeted

- Government grant funding (DOE, ARPA-E, BETO, SETO) alongside commercial traction—shows both technical validation and market demand

Red flags

- Multiple pilots that haven’t converted to larger deployments or commercial agreements (suggests product doesn’t perform well enough)

- LOIs from parties without purchasing authority or budget allocation

- Over-reliance on government grants without any commercial validation

- Pilot results that don’t clearly translate to commercial-scale performance or economics

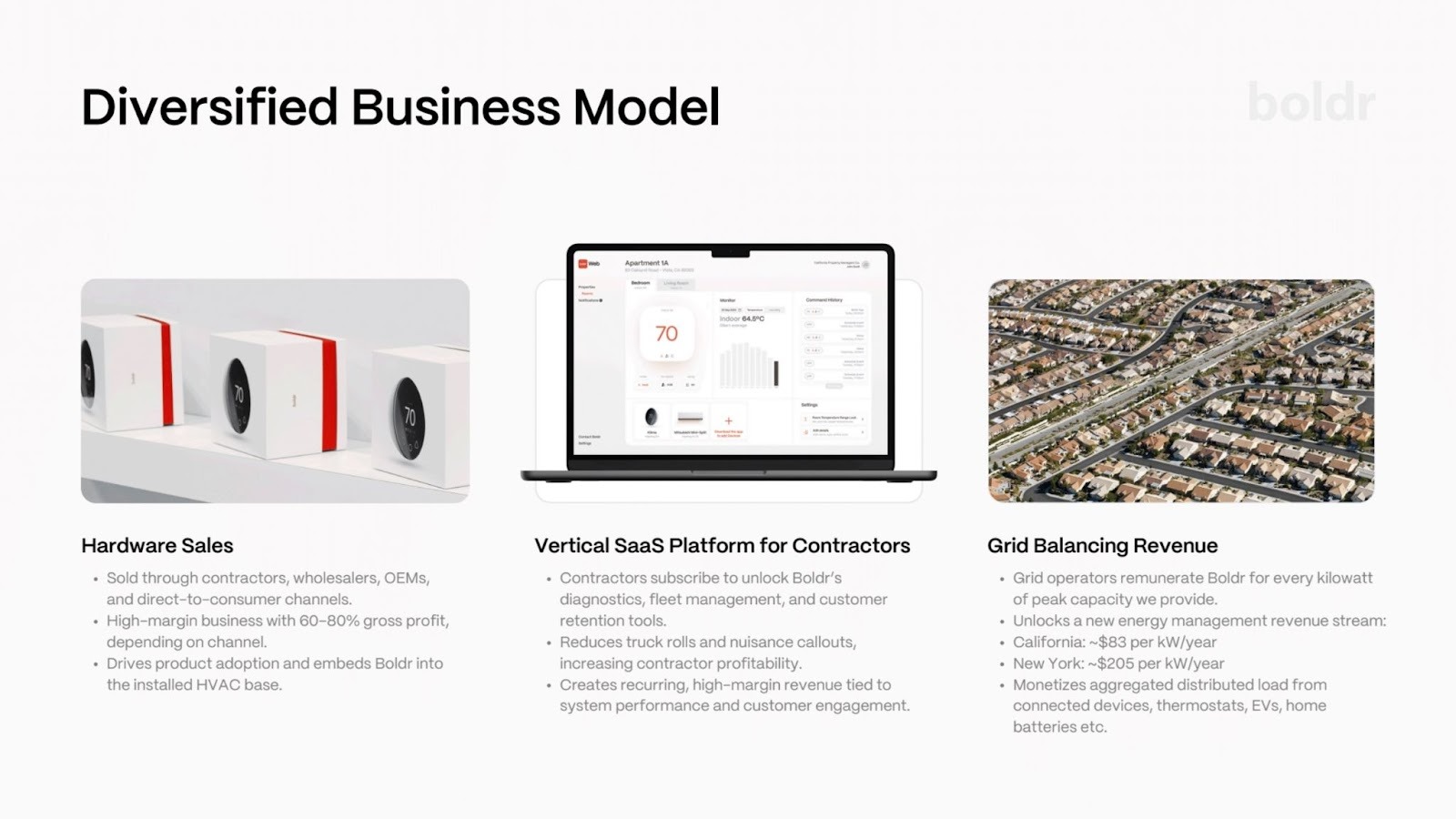

Business Model

How VCs think about your economics: TEAs, scale up risk, and capital stacks

Your business model slide should include how you make money, the price point to your end customers, and margin you are able to achieve yourself. This slide helps VCs understand the margin potential of your business, and stress test your anticipated customer pricing.

When diving deeper in your pitch, VCs want to understand:

- Your economics today

- Your projected economics at scale (and what needs to happen to get there)

- How you'll fund infrastructure buildout (equipment finance, project finance, debt) and how these limit dilution and impact net income over time

For capex-heavy companies: A techno-economic analysis helps VCs understand your model granularly and shows depth of thinking. TEAs can be outsourced as long as you control the assumptions. Learn more here.

For energy-selling companies: Investors want a pathway to at or below price parity with comparable energy delivery, storage, or transfer. Being able to explain why your system specs, integration process, LCOE, deployment timeline, and system ROI are optimal for your target use case helps VCs grasp your solution's attractiveness.

What gets VCs excited

- EaaS or long-term contract models with demonstrated customer willingness to sign multi year agreements

- Multiple revenue streams from a single deployed asset (energy sales + grid services + capacity payments + tax credits)

- Stacking of policy incentives (IRA PTC/ITC, state-level incentives, carbon credits) that improve near-term economics while underlying costs decline

- Land-and-expand dynamics where initial deployment leads to expansion within customer’s portfolio

Red flags

- Business model entirely dependent on a single policy incentive

- Installation and operation costs that remain high and unpredictable at scale

- No clear path from current prototype costs to commercially viable margins

- Revenue projections that assume perfect capacity factors or utilization rates without real-world data

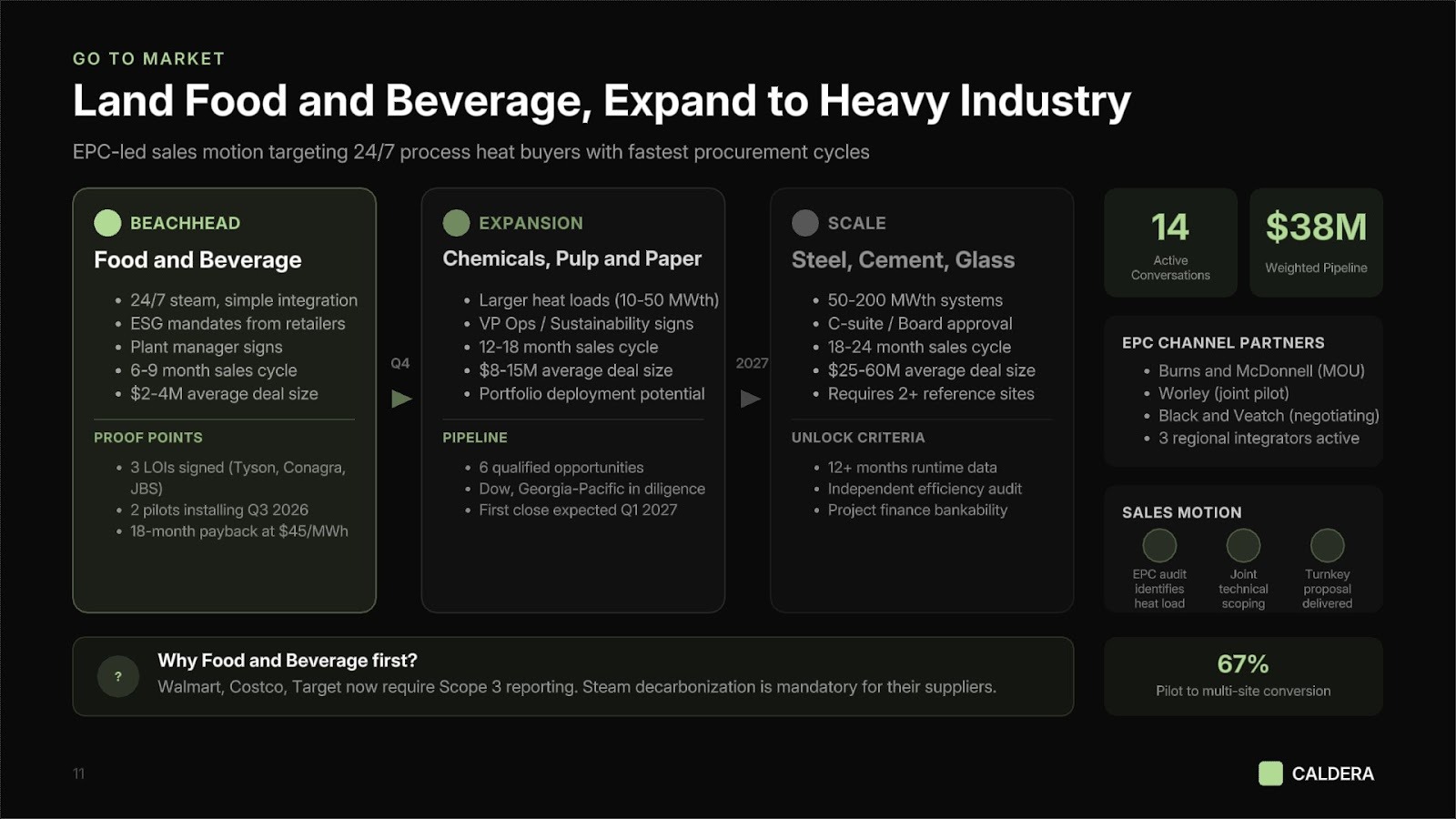

Go to market

Showing you can become big enough, fast enough

Within the pitch, the most important question to answer is how your GTM motion can support a venture scale amount of revenue (usually $100M+) within 5-7 years. VCs will generally use this slide to get to understand your depth of knowledge on the sales cycle and customer purchasing dynamics.

VCs will want to talk through:

Customer segmentation and sequencing:

- Initial beachhead: Start with the customer segment most willing to adopt new technology and where your economics are strongest.

- Expansion path: How do you move from early adopters to mainstream energy buyers?

- Enterprise and utility timing: When can you sell to top-20 utilities or Fortune 500 industrials? What proof points are needed from your larger customers to unlock the potential for adoption?

This slide should outline who your customers will be, how you reach them, and how you will stage your GTM if your customer type changes over time.

What gets VCs excited

- A clear beachhead with a distinct willingness to pay and ability to move fast

- Pipeline of qualified opportunities

- Customer references willing to evangelize and accelerate sales to peers in the industry

Red flags

- No clear segmenting and sequencing of customer types

- Pilots that don’t convert to commercial deployments

- Ignoring the role of project finance, EPC partners, and channel relationships in scaling energy businesses

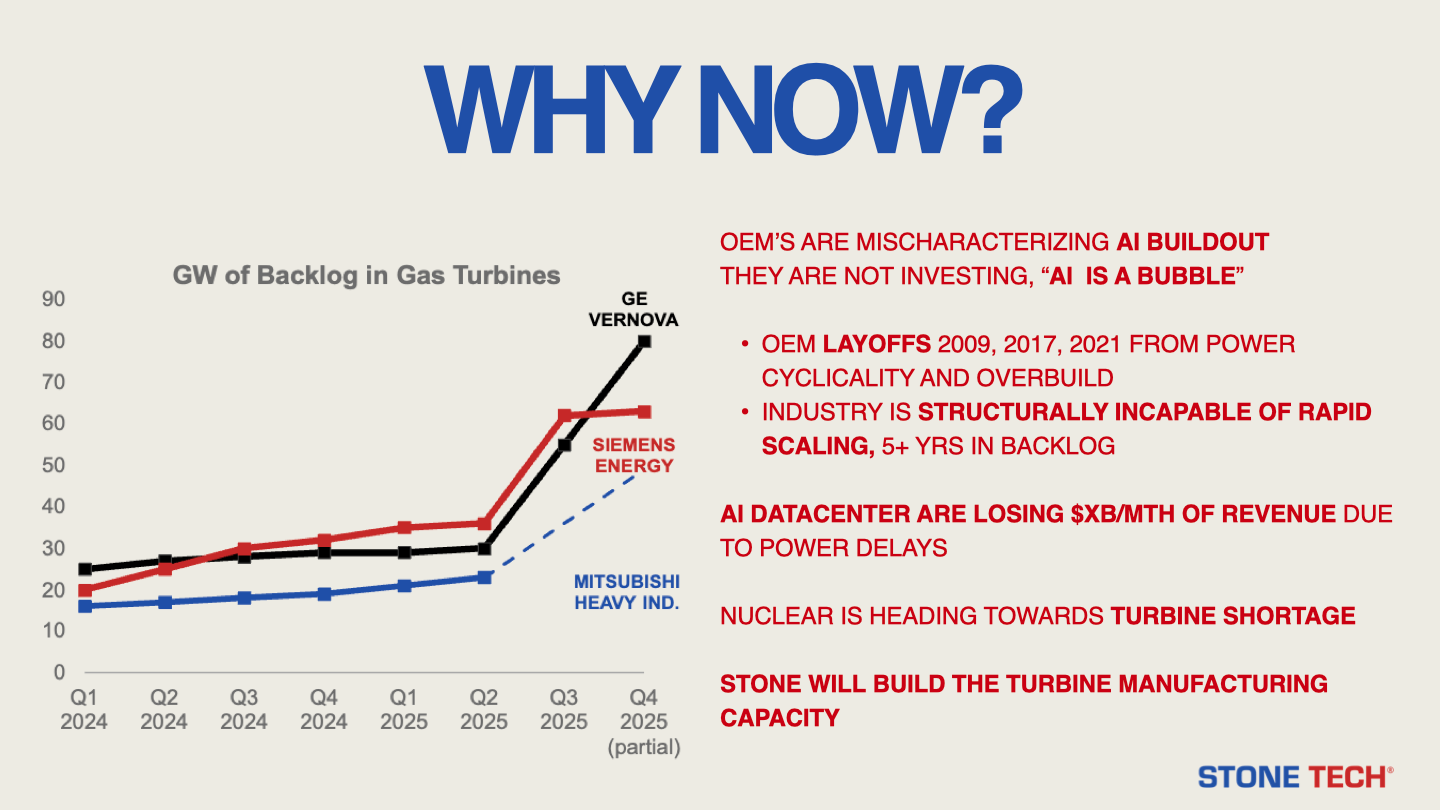

Why Now

Demonstrating why your startup has just become possible to build

Many energy startup ideas have been tried before. After addressing technoeconomic risk, explain what makes your startup uniquely possible now to overcome investors' "prior competitive landscape" concerns.

Inflection points across technology, policy, consumer behavior, or buyer demand create compelling narratives for why your startup is timely. Here are examples we're seeing in 2026:

Demand

- Power producers leave money on the table daily when they can't meet staggering demand for new capacity

- Infrastructure strain from demand spikes, intermittent power, and severe weather is driving demand for resilience, grid hardening, and intelligence

Technology

- Grid-scale battery costs have fallen 90%+ over the past decade. Solar module costs are at historic lows.

Policy

- Nationalized supply chain trends are directing capital toward battery and magnet supply chain companies

Consumer behavior

- EV and solar adoption is driven by peer influence beyond financial motivations—this will extend to modern HVAC and home energy management systems

Describing what inflection points make your business uniquely possible today helps investors overcome the “prior attempt” risk, and build enthusiasm for your business.

What gets VCs excited

- Specific, quantified changes in enabling conditions (“Battery cell costs fell below $80/kWh, making our system economics viable for the first time”)

- Confluence of multiple trends making your solution newly viable (technology cost + policy incentive + demand pull)

- Evidence that buyer willingness-to-adopt has shifted (“Two years ago, utilities wanted to study this. Now they’re issuing RFPs with delivery timelines.”)

- Recent failures of competing approaches that validate your different method (“Green hydrogen projects are being canceled at scale; our approach avoids the electrolyzer bottleneck entirely.”)

Red flags

- Generic claims about the energy transition without showing what specifically changed

- “Why now” arguments based on hypothetical future improvements (“When fusion works, our components will be essential”)

- Ignoring why previous cleantech companies failed at similar problems

- Over-reliance on a single policy incentive that could be modified or repealed—without showing the economics work independently

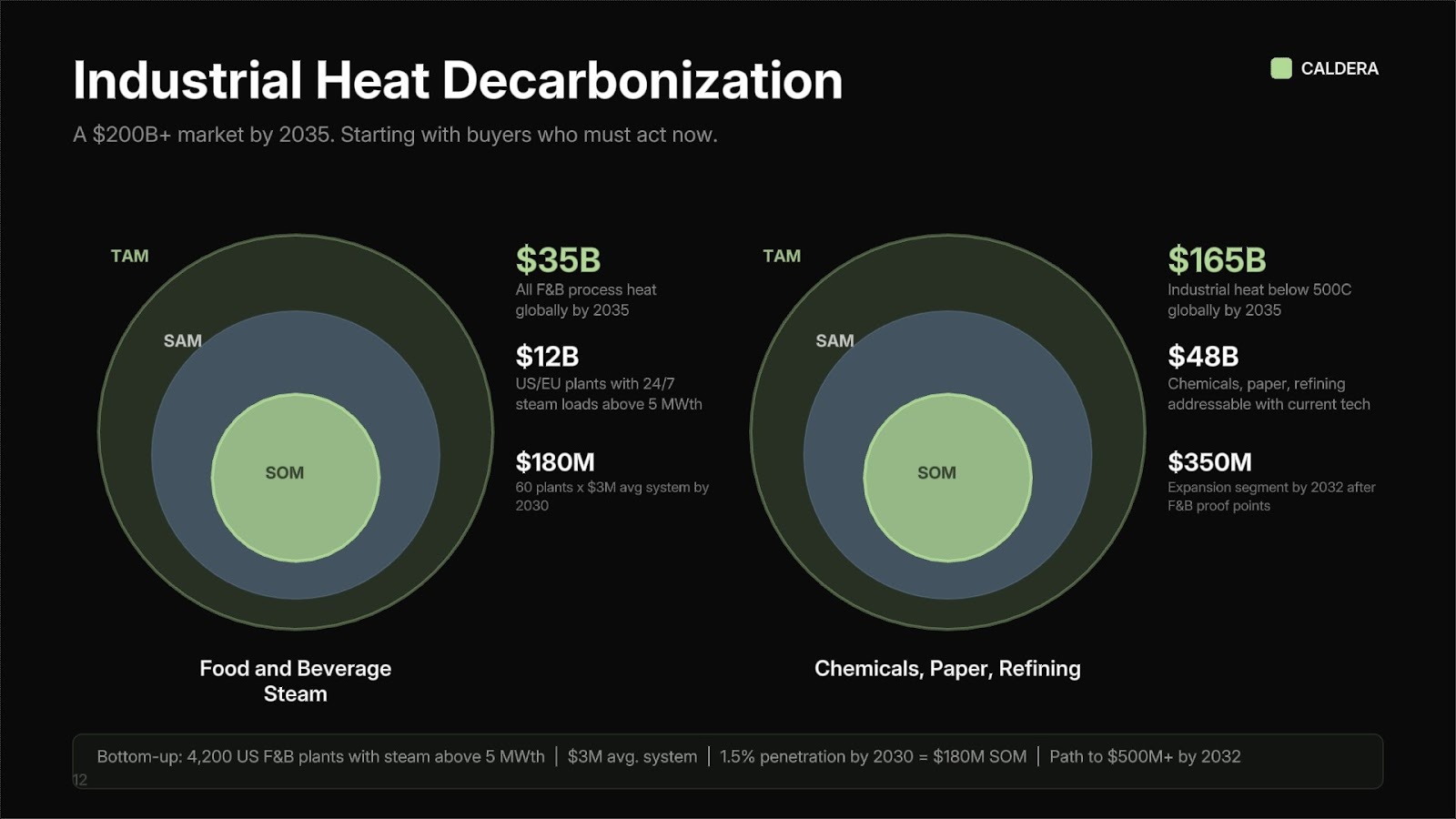

Market Size

Why bottom up beats top down

Your market sizing slide should be broken down into your:

Total Addressable Market (TAM) The total revenue opportunity if you achieved 100% market share across all potential customers globally. Total potential customers × Annual revenue per customer

Serviceable Addressable Market (SAM) The portion of TAM you can realistically reach given your business model, geographic focus, and current capabilities. Customers matching your target profile and location × Annual revenue per customer

Serviceable Obtainable Market (SOM) The market share you can realistically capture in the next 1-3 years, accounting for competition and resources. SAM × Realistic market share % that you could target over the next few years

This method of calculating these numbers is much preferred to “top down” market sizing, where you infer total demand based on high level industry numbers. This is because VCs want to understand how large your business can get. The TAM might be $5B, but if you price 1/10th of comparable products, the amount of market you can capture might be $500M.

It’s ok to lean towards top down if bottom up is hard to quantify, as well to have market sizes picked from estimates into the future (ie 2030 market size is X), so long as it’s clearly labeled how you’re getting to those conclusions.

What gets VCs excited

- TAM >$5B with clear, defensible bottom-up math showing a venture-scale opportunity

- SOM achievable in 3–5 years representing a $100M+ revenue opportunity independently

- Market sizing validated by customer conversations

- Evidence of market growth driven by structural forces (electrification, data center buildout, decarbonization mandates) rather than cyclical trends

- Platform potential where your initial application opens adjacent markets with realistic expansion path

- Ability to walk through how you arrived at your market sizing, and what your bottom up market size is for your SOM and SAM

Red flags

- Top-down market sizing only

- Market size claims that don’t match deployment realities (claiming 100% of industrial heat can be electrified when your technology works for specific temperature ranges)

Competition

Who are your competitors, and how do you demonstrate defensibility

Energy is a massive market that can support multiple venture-scale outcomes. The concern is whether competitive pressure from incumbents will crowd out your sales or erode pricing over time.

Put simply: when competing head-to-head, do you have good reason to win? Can you demonstrate a path to quickly become a trusted industry leader or achieve enough scale to carve out meaningful market share?

In discussing this slide, it’s important to keep in mind:

Energy competition is multi-dimensional. You’re competing against: (1) incumbent fossil fuel technologies, (2) established clean energy solutions, (3) other emerging technologies in your category, and (4) customers choosing to wait or do nothing. Your competitive positioning must address all four.

Addressing incumbent risk

VCs will ask: “Why won’t NextEra / Tesla Energy / Siemens / GE build this?” Your answer must show:

- Technology approach fundamentally different from their product roadmap or core competency

- Market segment they’re not targeting (they focus on utility-scale; you target C&I) or business model they can’t easily adopt

- Speed advantage: you can iterate and deploy faster while they manage legacy products and customers

- Novel manufacturing or materials approach that requires different expertise than they possess

The strongest defensibility arguments show your solution is directionally impossible or highly unlikely for top incumbents to build themselves. It should be technically novel, challenging to replicate without your team's specific expertise, and protected by IP. Over time, becoming a trusted industry leader and achieving economies of scale creates durable advantages over future competitors.

Tied to showing you can overcome competition, is showing why you will maintain a competitive edge.

Defensibility can emerge from

- Proprietary technology and IP: Novel chemistries, reactor designs, manufacturing processes, or system architectures protected by patents.

- Operational data and learning: Each deployment generates performance data that improves system design, control algorithms, and predictive maintenance.

- Bankability and track record: Every MWh deployed, every cycle completed, every year of operation builds bankability. Insurance underwriters, project financiers, and procurement teams need performance track records.

- Supply chain and manufacturing relationships: Exclusive feedstock arrangements, manufacturing partnerships, or component supply agreements that limit competitor access.

- Integration and ecosystem: Deep integrations with grid operators, utility SCADA systems, energy management platforms, or industrial control systems create switching costs.

- Economies of scale: Larger facility costs give unbeatable end prices, and are protected by the capital required for facility build out.

Your competition slide should demonstrate these characteristics.

What gets VCs excited

- Unique technical approach with IP protection (patents filed or granted on core innovations)

- Demonstrable performance advantages (2x duration, 30% lower LCOE, 5x faster deployment) on metrics customers actually use to make purchase decisions

- Strong head start with evidence competitors can’t easily replicate your approach

- Market positioning that makes you the obvious choice for a specific application

- Customer validation that your differentiators matter

Red flags

- “No competitors” or “we’re first”—there’s always competition, even if it’s the status quo

- Competitive axes that don’t drive purchase decisions (“we use a different chemistry” when customers care about LCOS and reliability)

- No clear answer to why large incumbents won’t build this

- Differentiation based only on features, not fundamental approach or business model

- Multiple well-funded competitors further ahead with similar approaches

- Claiming IP protection on obvious or easily-designed-around innovations

Team

What makes for a world-class founding team?

Energy founders come from diverse backgrounds—policy makers, aerospace engineers, scientists, prior founders. The common thread among great founders is understanding that commercial and regulatory challenges matter as much as technical ones, and surrounding themselves with teams to tackle both.

At Julian Capital, we’ve written about what makes a great founding team here. We're excited by founding teams who are:

- Commercially minded with technical depth

- Building their life's work—the culmination of their career or their final pursuit

- Ambitious enough to scale to $1B+ valuation

- Relentlessly resourceful with high agency

- Persuasive and authentic storytellers

- Comprehensive in thinking through all business avenues (GTM, competitive landscape, bottom-up TAM, etc)

Within energy, these qualities shine through:

- Deep technical expertise: At least one founder with the technical depth to navigate workflows and hiring from lab to commercial scale.

- Manufacturing or deployment experience: Someone who has scaled hardware manufacturing or deployed energy systems in the field. Understands: design for manufacturing, supply chain management, quality control, field commissioning, and what can go wrong between prototype and production.

- Energy industry and regulatory expertise: Deep understanding of your target customer’s world: utility procurement processes, industrial energy management, grid interconnection, power purchase agreements, regulatory frameworks. You know buying cycles, approval processes, and the language that resonates.

- Commercial and project finance capability: Someone who can sell into your end market. Doesn’t have to be a founder (can hire VP Business Development) but the founding team needs commercial orientation.

What gets VCs excited

- Teams that combine deep technical expertise, hardware/manufacturing experience, and energy industry commercial orientation

- Founders who have successfully built and deployed energy or hardware systems before (even in prior companies or roles)

- Deep domain expertise in target energy market with existing customer and industry relationships

- Track record of attracting top engineering talent

- Founders who are mission-driven and committed for the long term

- Understanding of project finance and capital structures needed to scale energy deployments

Red flags

- Teams without anyone who has built and manufactured physical products or deployed energy systems

- Founders who can’t articulate clear division of responsibilities or have overlapping roles

- Pure software engineers trying to build complex energy hardware without hardware co-founder

- Lack of urgency or treating this as a research project rather than a business with commercial milestones

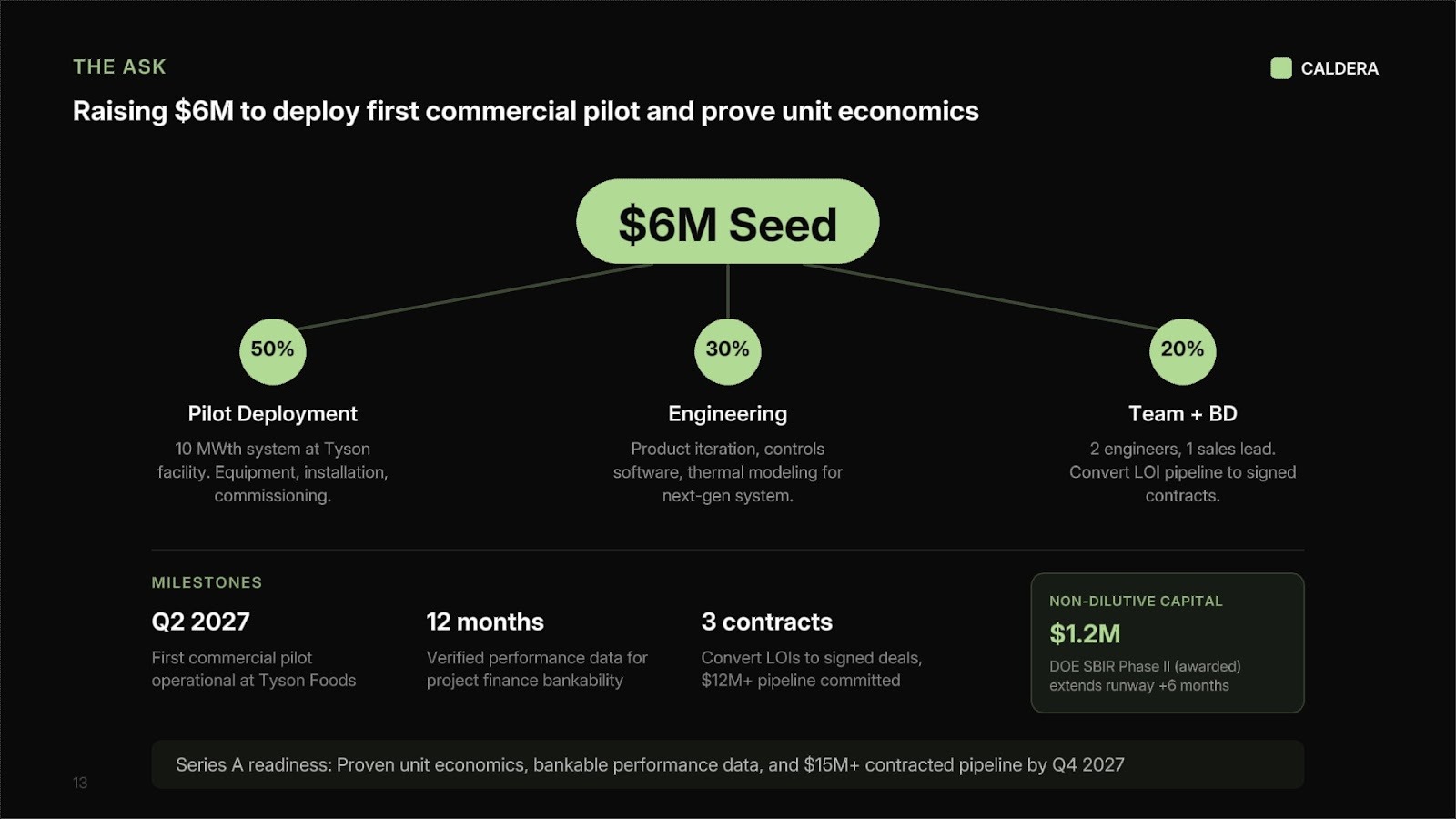

The Ask: Use of proceeds and round size

The ask shows how much you are raising and what you plan to accomplish with it. We wrote about choosing how much to raise here.

You should account for the capital intensity of hardware development, pilot deployments, and the long timelines associated with utility and industrial sales cycles. Investors want to see that your raise gets you to clearly defined technical and commercial milestones.

What gets VCs excited

- Raise sized to specific technical or commercial milestones (first pilot, first paying customer, a specific performance threshold)

- Clear articulation of what de-risking the next round requires

- Evidence that non-dilutive capital (grants, DOE loans) has been pursued or secured to extend runway

- Use of proceeds that maps directly to the team and infrastructure needed to hit stated milestones

Red flags

- Raise sized by "how long we can survive" rather than "what we need to prove"

- No clear milestone that the funding unlocks—just generic "product development and sales"

- Underestimating capex requirements for hardware builds, permitting, or pilot deployments

- Assuming maximum grant funding without contingency

Pitching: Do’s & Dont’s

Here’s how (and how not) to pitch:

The best pitches are conversational. Answers should be succinct yet demonstrate depth of thought.

Great founders bridge vision with detail. They intimately understand their problem space and can explain it clearly—both the problem and the system around it. They understand the path to scale and can map how the business will evolve getting there.

Do

- Be honest about what doesn’t work yet: VCs appreciate realism. “Our system achieves 82% round-trip efficiency; we’re targeting 88% with our next-gen power electronics”.

- Have strong answers on unit economics: You should be able to walk through your projected system and business economics.

- Demonstrate customer intimacy: Drop specific details that show you deeply understand your buyer: “Utility procurement requires an independent engineer’s report, insurance certification, and typically a 12–18 month evaluation period before a PPA is signed.”

- Address the “why now” directly: Proactively explain what’s changed that makes your solution viable and your business timely.

- Acknowledge and address incumbent risk: Don’t wait for VCs to ask “Why won’t Tesla/GE/Siemens build this?” Address it upfront with a credible, specific answer.

- Lean in on your team: At the early stages, you and your team are a driving decision factor. Show why you’re uniquely qualified to bring this business to market.

Don’t

- Don’t get lost in technical details: Focus on what your system does, what it costs, and why customers need it. Dive in further on the tech when prompted to.

- Don’t overclaim your capabilities: Every energy technology has limitations—temperature ranges, cycle life constraints, geographic requirements. Be specific about what you can and cannot do.

- Don’t dismiss competition: Acknowledge competitors—including the status quo—and explain your differentiation.

- Don’t ignore the commercialization challenge: If your team is all PhDs with no industry experience, acknowledge this as a gap and show your plan to address it (advisory board, early hires, partnerships).

We hope this guide was useful to you and if you’d like to get in touch, don’t hesitate to reach out to Julian.Capital, Lowercarbon, Climate Capital, and Voyager. You can also apply in <1 minute to get put in touch with thesis fit investors for free at DeepChecks.VC.

Want to know what Lowercarbon thinks about the future of energy? We went deep here:

What are trends (inflection points in technology, cost curves, demand, policy, or consumer behavior) that excite you about this sector?

You have a few fundamental pressures driving the adoption of new solutions. Customers are racing to deploy power to meet staggering energy demand in the coming years, desperate because they’re leaving money on the table every day they can’t energize new capacity. You also have customers seeing their status quo physical and digital infrastructure buckling under pressure, as a result of this speed, intensifying weather, labor constraints, and more. While these are slightly different drivers, they result in the same intense urgency for new solutions. It is hard to understate just how strong the customer demand is today for technology and services that will solve problems for customers across the energy landscape. As a founder, you are stepping into markets where customers already feel pressure. The structural demand - meaning customers who are constrained by supply or reliability - means the path to adoption becomes much clearer. We are seeing major customer demand in the way of real purchases and real offtakes sooner than we’ve ever seen it.

Amidst the movement, it can be hard to choose where to focus your energy as a founder, but we come back to the big picture on what makes us excited about the future. There’s been an amazing development of the venture-readiness of the average startup building in the arena of hard tech; this extends beyond energy systems and into other closely related fields like biotech, manufacturing, and beyond. Potential founders have had more surface area to learn how to build great hardware and how to handle operational complexity at companies like SpaceX, Tesla, Anduril, and now even the companies derived from those training grounds. The acceleration of hardware iteration with AI is taking this to another level.

What have these inflection points uniquely enabled?

Put together, these trends are powerful. We’re in a moment where better solutions will exist at the moment when customers want to pay for them. When teams can build, test, and rebuild with that kind of speed, entire new categories become viable to be venture-scale companies. Companies are figuring out how to build deeper moats and to scale into dramatically bigger markets. As a consequence you see more investors gaining appetite to invest in hardware, and particularly around the challenges of energy systems, which have been previously more difficult to change.

This is a market environment where the scale and urgency of demand is shaking customers loose from prior patterns of activity and creating space for more cost effective, reliable solutions to win on their own merit. As a firm who has obsessed over the economics of energy for roughly the past decade and seen promising solutions for improving it across generation, distribution, and more, the value of these solutions is finally being recognized by customers and reaching breakout growth.

On a personal level for founders, there is something grounding about working on problems that aren’t discretionary. You know your market will exist 10 years from now. From what we see, energy challenges are a great home for people looking to do their life’s work.

If you could wave a magic wand, what underserved customer segment or problem would you want more startups tackling?

The playing field in energy is vast. It’s impossible to call just one problem. The following are just a sample of some of the critical challenges in energy that companies in our portfolio are solving:

- Data centers from clean, low-cost power (Crusoe)

- Solving the turbine bottleneck (Arbor)

- Grid-responsive data centers (Emerald AI)

- Financing energy infrastructure (Crux)

- Leading commercial fusion development (Commonwealth Fusion Systems)

- Powering solar assets from space (Overview)

- Protecting utility infrastructure from wildfire (Gridware)

- Autonomous nodes for ocean-based power production (Panthalassa)

- Residential rooftop solar for the Indian market (Solar Square)

There are many multi-billion dollar companies to be built. Finding the problem and shape of company that you are particularly motivated by is the real challenge for founders.

Underwriting Demand: How do you underwrite customer demand in this sector?

When the markets can be as large and fundamental as ‘customers needing electrons’ - sussing out customer demand is not really an exercise of if customers will be interested in what you’re building. They will. It’s about how good a company is at productizing, selling, and executing that solution or service. That is what makes something sink or swim.

The overwhelming scale of demand doesn’t mean getting traction with customers is easy. Customers in the energy realm don’t always operate like your average market. Among the main differences:

- Your product doesn’t solve a problem in isolation but is actually a part of a constellation of solutions, all relating to the physical grid and its constraints. The value to your customer is in the whole picture of their solution set, not just what you bring to the table. Figuring out how you fit in is somewhat of a puzzle.

- Utilities as a customer base have particular incentives and ways of operating. To put it simply, the sales cycles are complex and require expertise. Even if you are not directly selling to utilities, the influence of their market behavior will find every corner of the market.

This said, there are of course ways to successfully navigate this. At the early stages of a company’s life, we look for instincts from the founder around the commercial motion and granularity in their thinking around prospective partners and customers. TAM should be supported by specifics. If a company’s pre-revenue, are there any ongoing conversations with customers or partnerships that allude to future interest? Where is a customer already constrained by something very concrete, like grid congestion, supply chain gaps, or infrastructure strain? What makes that constraint urgent enough to create willingness in the coming year or two, versus being a hypothetical future need? Even if the insights prove wrong, this kind of thinking is an important leading indicator for success at the later stages where founders need to understand the exact customer, the exact constraint, and the exact pressure that creates willingness to pay.

One way that venture-scale companies have hacked early scaling is proving out a real demonstration of some kind. What counts as a solid demo varies by business but the universal thing is that it derisks something that matters to your customer or partner. The best demos have a real customer who validates the outcome by paying for it in some capacity or by publicly endorsing the results. If investors can draw a straight line between this demo and the larger commercial motion, that is a win.

What factors influence purchase decisions, and which ones hinder adoption?

In the AI race, speed is everything. With the urgency that customers have to get solutions ready, startups have needed to move even faster than historical precedent. With customers focused on the fastest path to gigawatts, there is time sensitivity on the scale of not years, but months. What used to look like an acceptable deployment schedule in the range of 5 years to getting to a commercial deployment of some kind, has been compressed to 2-3 years or less.

Learn how to navigate big, multi-headed customers. Everyone from utilities to hyperscalers like Google and Microsoft will need to draw on a range of solutions. This means:

- Your solution will sit as part of a portfolio of approaches, reaching across production, interconnect, compute, financing, and more. Knowing how your solution fits alongside others in a portfolio means you can communicate your value better; it may even inform a smart distribution or partnership strategy that helps adoption.

- Finding the way to the decision maker for your particular technology is not always straightforward. Landing the right hires, advisors, and investors to help you navigate the maze of a partner conversation can be extremely helpful.

Adoption fails when founders assume that technology will speak for itself. Customers need to understand how a solution fits into their world, not just that a technical breakthrough is impressive. So, the clearest influence on purchase decisions is whether the technology removes a real bottleneck for the customer. Reliability, integration with existing systems, and cost clarity matter a lot. Much of this comes from knowledge gained firsthand through insider experience working in the sector; otherwise it’s from obsessive research and customer study.

What type of traction matters to you at the seed stage?

At seed, the thing that matters most is whether the founder has a clear reason for building in this space. Trying to make change in the energy landscape is unforgiving and founders need to know exactly why they are choosing to build in this space. Layer on the challenges of building hard tech businesses and the challenge multiplies.

Some of the best companies will pivot many times, so we care less about revenue and more about the depth of thinking and the early signals that the founder will be able to carry the company through its lifetime.

Specifically, we look to:

- Who are your earliest hires? If you are building solo and have yet to hire anyone, what company do you keep as advisors or part-time support?

- What early hints of customer insight do you have, and how have you acquired that insight? While you might not have a full pipeline built out yet at the pre-seed and seed stages, you likely have a range of conversations going with prospective customers and partners. Where do those sit in a high level pipeline (first conversation, pilot discussions, moving towards LOI/MOU)?

- Are there any wins on technical validation, and is it something that truly speaks to proving out the core premise?

- Do you have a sense for how much capital you’ll need over time as you scale? How do you plan to pull on both equity as well as a broad set of non-dilutive sources of capital?

- Do you have clear near-term milestones (next 12-24 months)? If you raise, can you communicate what you plan to spend the money doing?

Technical Risk: How do you underwrite technical and scale-up risk?

The core question is whether you can prove the concept works at a scale that matters to customers, for a reasonable amount of capital. What’s "reasonable" varies by company, but we're looking for founders who have mapped the path to deployment and can articulate what each step actually derisks.

- Milestones should be sequenced and show a founder understands how each rung unlocks the next. Primarily we look for proof around the unit economics and repeatability of a core scaling motion (unless there’s real technical risk, in which case we will look for a lab or other type of technical demonstration).

- We also look for iteration velocity (AI-driven simulation, modular architectures) and the ability to compress long development cycles into shorter periods of time.

- Capital requirements often surprise founders. Many underestimate what it takes to scale hardware, or haven't thought through whether they'll license, build, or vertically integrate. Technical decisions have capital implications down the line. A founder doesn't need all the answers at seed, but they need to show that they have thought about the questions.

- Getting a customer to validate the demonstration strengthens things even more, particularly if they will pay for the output or publicly validate it. Oftentimes this is the allowance that other customers need to follow suit.

Competition: Are there areas where the competitive landscape is especially crowded?

It’s easy to fall into the trap of saying: there’s already a great company here, I won’t build in this space. But the reality is that these markets tend to be expansive enough with enough diverse needs that you shouldn’t automatically write off another entrant. The key is that if there is already a strong player tackling a problem you’re interested in, you need to have conviction on why your company has a right to win.

What trends or types of startups are overhyped right now?

Overhyped ideas often share this quality of being framed to impress investors rather than built to solve a problem someone actually has. This is very clear in companies leading with an AI narrative that sounds promising, but is actually disconnected from a real customer problem and with no sense of a viable business model. We’d say that the burden of proof for companies today is higher, given the froth.

Exits: How do you evaluate exit potential in this sector?

Even from the earliest stages - possibly a decade plus from exit - investors are focused on whether a company can yield a venture-scale exit. While there are plenty of problems to be solved in the field of energy, many approaches and solutions are simply not compelling enough to customers to gain significant adoption, or lack real exit pathways.

Investors can and should come to their own opinions on these things, but you can help fill the gaps by thinking ahead about:

- Precedent transactions across IPOs, M&A, strategic investments: Where have other companies in this field, or analogous ones in other fields, seen exits?

- Public comps: How do relevant companies trade in the public markets?

Are there any M&A trends to look out for?

It’s worth asking why this question matters for companies at inception or very early stages. For early stage founders who want to build to billion dollar outcomes, it’s good to have an eye on M&A trends to the extent you can explain in broad strokes what you’ll encounter in the market: who may want to pick you up early? What you have an eye on acquiring as you grow? How does it show what customers value and will pay for? You want to be obsessive about the goings-on of the markets relevant to you, even if you don’t see a near-term exit via M&A as your primary strategy.

On specific M&A trends across energy: Infrastructure operators, utilities, insurers, and industrials are increasingly acquiring technologies that let them operate more safely, withstand more volatility, or recover more quickly from extreme events. These purchases feel strategic rather than opportunistic which creates good opportunities for founders who are building in resilience, risk reduction, or automation.

Team: What particularly stands out to you in a strong founding team? Are there any qualities of a founding team or pitch that stand out to you?

Lowercarbon’s portfolio is a testament to the range of founders that can make impact in the field of energy. Some come from government roles and have a pre-written map for navigating agencies and pulling on budgets. Some built everything from Falcon 9 to Starbase from the ground-up and know what it takes to build big physical systems with speed. Some have led full technology programs within the Department of War. Some are consumer hardware fanatics who’ve brought their talents to a new class of products. Some are solo founders and some are large co-founding teams. There is no one way to do it.

What great teams in the energy field have in common is that from the start, they are tapped into the fact that this is not purely a technology game. It is even more so a commercial and regulatory one. So building competency across multiple domains as a founder at the early stage - and ultimately hiring the right people to lead these efforts across policy, operations, marketing - is a requirement.

Some other elements of exceptional founders and founding teams are universal:

- Whether they’re technically co-founders or not, the founding team is critical for success. This applies to early part-time help and contractors too. As investors we are laser focused on the company you keep and what that reflects about judgment, ability to tap networks of expertise, and most importantly - whether you’re able to convince people to come along for the ride.

- The strongest founders bridge vision with detail. They understand their problem better than any investor ever will and they can explain it in a way that does not require theatrics. They also show early instincts about how their business model will evolve which tells you they have thought about what scale will ask of them. They have thought deeply about the problem and the system around it. And they communicate with a kind of clarity that makes complex topics feel accessible. Those founders always stand out.

Pitching Pitfalls: What are the most common reasons you pass in this sector right now? Where do founders have blind spots in their pitch or business model?

- Cost and speed advantage falls short. In power generation especially, you're compared to every other electron source, and right now, speed-to-power has become the single most important procurement metric for the largest buyers. Given the urgency of demand, speed of deployment is as important as LCOE.

- Interesting technology without a clear customer need or business model. As mentioned above, founders sometimes skip over the hard question of who will actually pay and why. Monetization can be the real bottleneck in hard tech and it requires the same level of creativity as the technical work.

- The underestimation of capital needs is another company killer, especially in sectors where physical assets are unavoidable.

- As a stylistic consideration, when a pitch relies heavily on buzzwords, it undercuts the seriousness. Frankly, AI froth has increased the burden of proof on founders while pitching, as it is more common to be perceived as opportunistically riding the wave of a trend. Substance and detail are the goal; as a tactical point, a pitch that relies heavily on buzzwords is difficult to take seriously.

What makes a pitch stand out?

It always comes back to the team – why you want to build this business, and the people you’ve brought along for the ride for your first hires. And when the founder can walk us through how the technology becomes a scaled business, without reaching for buzzwords, that creates a lot of confidence.