Want to know exactly how VCs evaluate your materials & industrials startup?

Together with Steel Atlas, KdT, and Grid Capital — some of the leading materials & industrials VCs— we’ve built this guide to unpack the inside baseball on how VCs evaluate materials & industrials startups, and in turn how you can raise a successful round.

Informed by reviewing thousands of decks, and insights on which startups get the most traction on Deep Checks, this playbook helps put together a teaser deck that gets your first VC pitch scheduled.

We’ll go slide by slide on how investors decide whether or not to move forward with a startup. It’ll cover:

- Problem: Demonstrating you’re solving a burning pain point for your customers

- Solution: Show why you have the best solution to this problem

- Technical risk: How to convince investors to get behind the remaining technical risk that you have

- Why now?: Demonstrating why your startup has just become possible to build. This is make-or-break for many pitches

- Traction: How to show there’s demand for your product before the market has adopted it

- Business Model: How VCs think about your economics

- Market Size: Why bottom up beats top down

- Go to market: Showing you can become big enough, fast enough

- Competition: As markets become crowded, how to create defensibility

- Team: What makes for a world-class founding team?

- The Ask: Use of proceeds and round size

- Pitching: Do’s and dont’s of pitching your startup to VCs

Problem

Demonstrating you're solving a burning pain point for your customers

The best problem slides both describe the painpoint and reveal the structural reason the pain has persisted. The explanation of the latter is often a signal of a founder's market insight(s).

Materials and industrials problems typically fall into one of four categories: performance limitations of existing materials, cost/efficiency gaps in production processes, sustainability/regulatory pressures, or supply chain vulnerabilities. The most compelling pitches quantify the industrial pain point with specific metrics:

- Performance limitations: Existing materials can’t meet desired performance specs for lifetime and performance of products or certain operating conditions.

- Process economics: Manufacturing processes with fundamental efficiency limits, energy intensity problems, or yield/waste issues.

- Sustainability/regulatory pressure: Industries facing carbon taxes, emissions regulations, or customer sustainability requirements, hazardous chemical phase-outs,), or circular economy mandates.

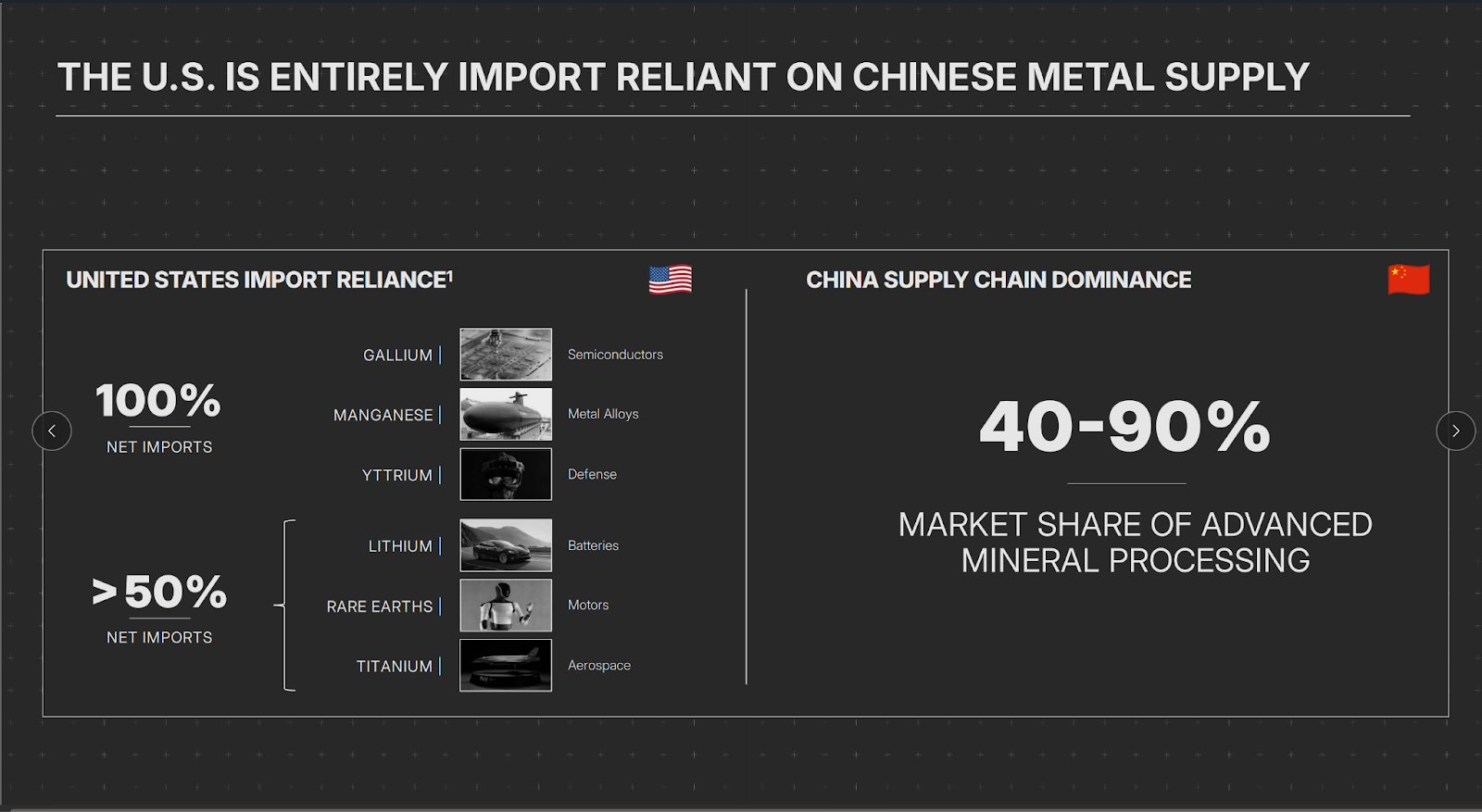

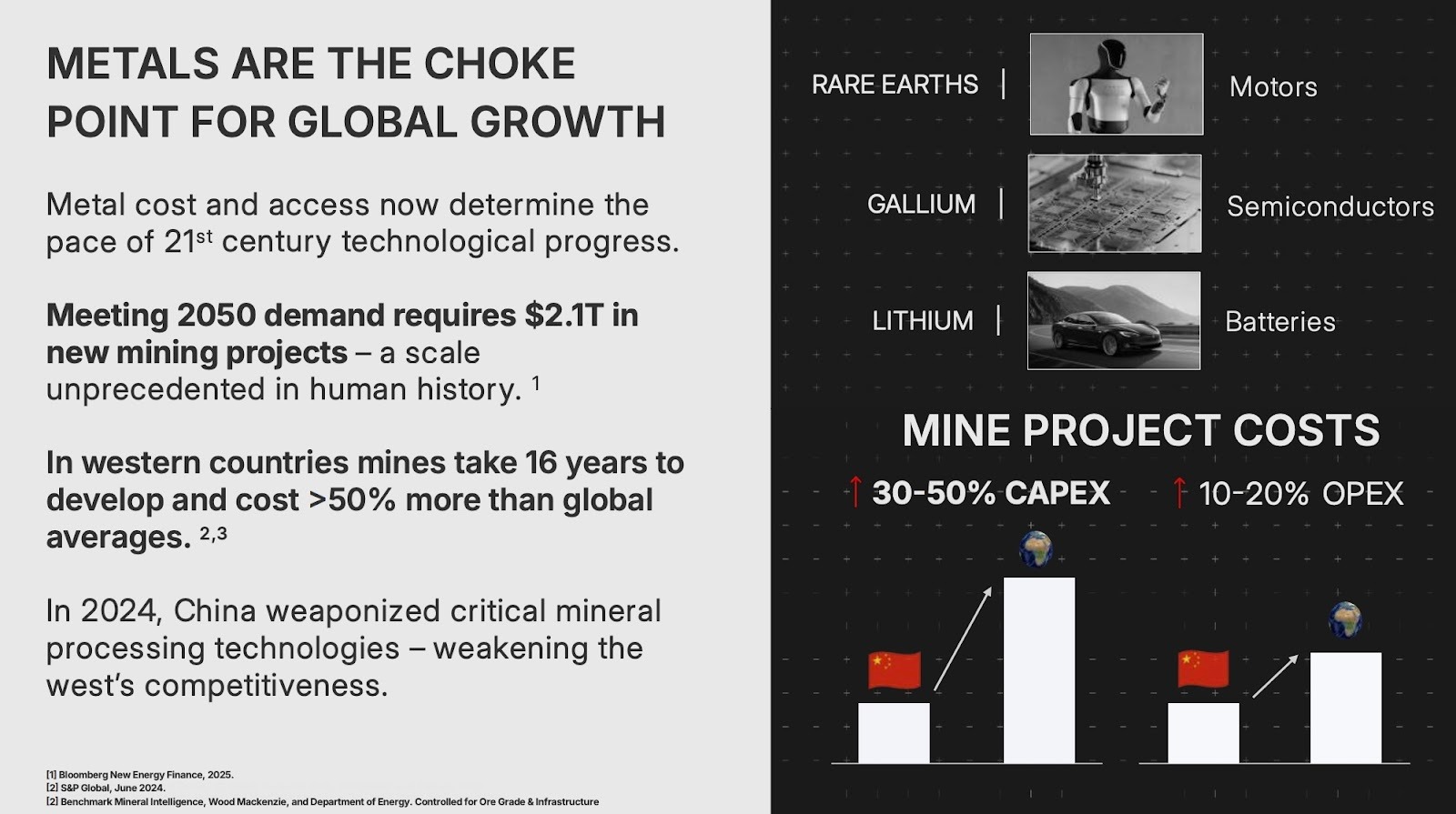

- Supply chain/geopolitical risk: Critical material dependencies on single countries, long-tail specialty chemicals with few suppliers globally, or materials requiring conflict minerals or restricted exports.

For startups that are building manufacturing capacity themselves: You must prove how your product meets performance requirements, prices, or supply chain needs in a manner that is compelling enough to switch over from the incumbent solution. Often, this comes with material qualification processes.

If you are integrating into existing factories, demand starts with the operational pains every machine shop or fab shop understands. This starts by asking which line item your system replaces. If the customer hasn't been spending money on it, it is probably not a priority.

The best way to describe the problem your customers face is to describe the exact financial or supply chain issue your customers are facing.

What gets VCs excited

- Problems where the economic pain well exceeds the solution cost

- Regulatory or market forces creating hard deadlines

- Problems that are getting worse over time (carbon pricing increasing, supply chains deglobalizing, performance requirements rising)

- Evidence that customers have tried solving this internally or through traditional chemical suppliers and failed

- Multi-billion dollar industries held back by a materials bottleneck

- Technical limitations that incumbents publicly acknowledge they cannot solve with incremental improvements

Red flags

- "Better" materials without quantified customer willingness to pay for the improvement

- Problems that could be solved through process optimization or formulation tweaks rather than novel materials

- Generic sustainability claims without specific regulatory drivers or customer mandates

- Focusing on material properties ("higher strength-to-weight ratio") without connecting to customer economics

Solution

Show why your solution is the best solution to this problem

Effective solution slides connect the innovation to customer ROI through the full value chain. Rather than leading with technical spec improvements, show the economic and operational impact:

- Performance metrics in customer context: "Maintains strength to 250°C enabling $600/unit lightweighting vs. steel" not "Tm of 280°C"

- Direct cost comparison across total cost of ownership: "$12/kg material cost vs. $8/kg incumbent, but reduces assembly steps from 6 to 2, saving $15/unit in manufacturing" - include processing, assembly, yield, logistics

- Qualification timeline and path: "Drop-in replacement requiring only reformulation (6-month qualification) vs. redesign (24+ months)"

The solution must address why it's better than: (1) existing workflows with process optimization, (2) incumbent suppliers' roadmap materials/solutions, (3) other startups tackling the same problem.

Hence, your solution slide should detail the precise benefits (by means of price or business outcomes delivered to your end customer) that show why you solve this problem for your customer.

What gets VCs excited

- Clear value proposition at commercial scale

- Solutions that are drop-in replacements or require reasonable qualification

- Evidence that the solution works in real production environments, not just lab samples (scaled synthesis, tested in customer processes, durability data)

- Multiple value drivers simultaneously: performance, cost, sustainability, and/or supply chain security

- IP protection around composition, synthesis, or processing that creates lead time for competitors

- Path to continuous improvement through formulation optimization, process learning, or additional R&D

Red flags

- Solutions that require complete redesign of customer products or processes

- Leading with material properties before showing business value

- Cost competitive only at a commercial scale you won't reach for years (companies can sequence around this with early markets that have higher willingness to pay)

- No clear path from current lab/pilot scale to commercial volumes and costs

- Ignoring critical qualifications: regulatory approvals (FDA, EPA, REACH), industry specs (ASTM, ISO), or customer testing requirements

Technical Risk

How to convince investors to get behind the remaining technical risk that you have

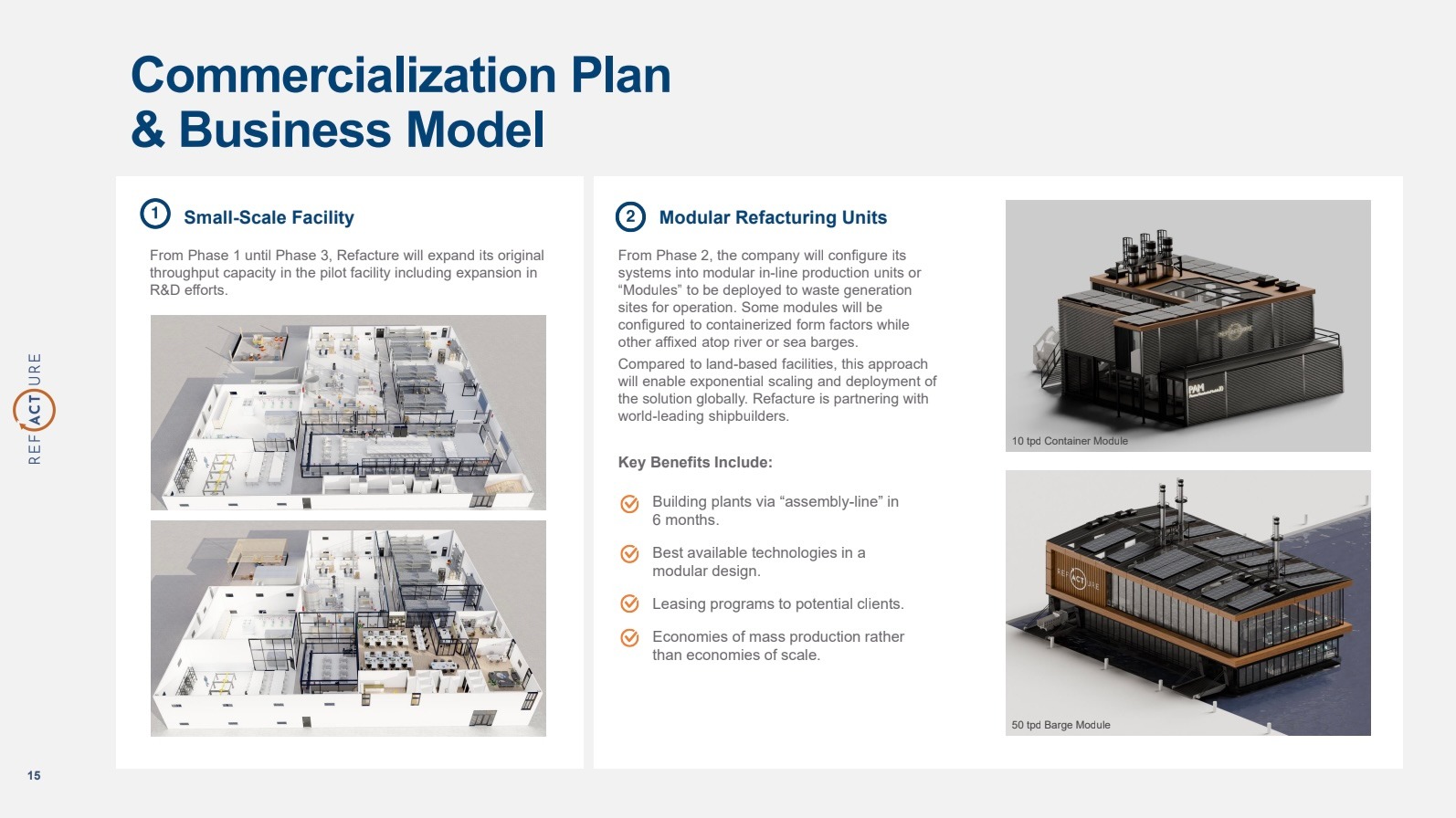

The most important thing to de-risk is your material or process having a path to being de-risked at the specs and price point needed by your end customers. Being able to show how far along you are and what remaining work there is to get there (or within further efficiency from production at scale) are the two most important aspects of the technical risk slide.

In showing this, keep in mind:

Deeptech venture investors typically accept engineering risk (if your team can credibly tackle it and it's technically feasible) but not scientific risk (where your product might simply not work). Early stage VCs want to know:

- What has been proven

- What needs to be proven

- Why you're confident you'll achieve this

For materials and industrials ventures this could mean:

- Ability to produce batches at a size that can be tested by your customers

- Performance validation: Third-party testing data, customer field trials, or industry-standard certifications.

- Manufacturing pathway: Identified contract manufacturers or toll processors.

- Raw material supply chain: Ability to secure suppliers for key inputs at commercial volumes and prices

- Quality and consistency: Demonstrated batch-to-batch reproducibility.

For manufacturing inputs: You must start by describing the output of your product or system that allows your customers’ system to work at scale. For semis, keeping defect density stable across wafers, lots, and tools as volume increases. For heavy fabrication and shipbuilding, preventing distortion so large structures fit together without rework.

What is the single physical limit that caps the entire system? Every serious manufacturing technology has one. The best founders are able to map the supply chain they operate in and identify associated bottlenecks and risks. Being able to describe these constraints, and the work you’ve done to push through it helps get to the bottom of your ability to integrate with end customers - a high TRL solution means little if it’s too far from manufacturing integration feasibility.

To quantify the financial viability of this transition, many investors rely heavily on Techno-Economic Analysis (TEA) rather than traditional P&L statements and forecasts. Since the cost of the first unit is often astronomically high, the team models Nth plant economics: the theoretical unit economics when the factory is running at volume. This model is subjected to rigorous sensitivity analysis, e.g. what happens to gross margins if production yields drop by 15% or if energy prices spike. If the business model collapses under minor operational variances, it becomes very difficult to craft a story for an investment. This should be backed by a sensitivity table, and narrative around how you act if different variables are impacted.

As such, this slide should include technical diagrams (if not covered in the solution slide), your TRL level, and highlight any remaining customer benefits not covered in the solution slide.

What gets VCs excited

- Working samples in customer hands being tested in their processes right now

- Pilot-scale production demonstrated with cost structure understood

- Clear identification of remaining scale-up risks with concrete de-risking plans

- Strong IP position: composition of matter patents, process patents, or trade secrets that create real barriers to entry

- Early engagement with an EPC firm to consult about the first of a kind financing needed for commercialization, or have done an early front-end engineering design study

Red flags

- Still at lab scale production/process readiness without a clear path to kg scale

- Process requires exotic conditions (ultra-high pressure, cryogenic temperatures, ultra-pure environments) that make scale-up capital-intensive

- No demonstrated batch-to-batch consistency or quality control processes

- Relying on future breakthroughs ("We expect AI to optimize our formulation" or "Better catalysts will reduce our cost by 10x")

- Teams that have only academic / national lab backgrounds and haven't owned a production outcome. If that's the case, address head-on and explain the mitigation plan (e.g. key hire, weeks embedded on customer plant floors etc)

Why Now

Demonstrating why your startup has just become possible to build

Many times, ideas have been tried before and failed to materialize. By describing what has changed in the world that makes it uniquely possible to build your business today, investors gain confidence in your business.

Inflection points across technology, policy, consumer behavior, or buyer demand create compelling narratives to demonstrate this. Here are examples we're seeing in 2026:

Demand:

- Automotive electrification driving battery materials demand (projected 40% EV penetration by 2030 creating 2,000 GWh cell demand)

- Industrial decarbonization mandates: EU carbon border adjustment mechanism (CBAM) pricing emissions-intensive imports, corporate net-zero commitments requiring supply chain decarbonization

- Building sector transformation: Net-zero energy codes requiring dramatic envelope improvements, mass timber adoption in mid-rise construction

Technology:

- AI/ML for materials discovery: Models screening millions of candidates reducing discovery time from years to months

- Advanced characterization: Cryo-EM, atomic-resolution microscopy enabling understanding of structure-property relationships previously invisible

- Continuous flow chemistry: Making small-batch specialty chemicals economical, enabling on-demand production

- Digital twins and process simulation: Reducing pilot-plant iteration cycles by predicting scale-up behavior

Policy:

- PFAS phase-outs: EPA designating entire chemical class as hazardous, eliminating incumbent solutions in coatings, textiles, firefighting foams

- Inflation Reduction Act: Production tax credits for clean hydrogen ($3/kg), advanced manufacturing credits (25-30% of capex), making low-carbon processes economically viable

- Critical minerals policy: CHIPS Act, Defense Production Act funding for domestic production of rare earths, lithium, graphite

- Circular economy regulations: Extended producer responsibility, recycled content mandates, packaging restrictions

Note that policy tailwinds can be reversed or rescinded—businesses that are existentially dependent on them carry meaningful risk that VCs will discount accordingly.

Supply chain:

- China export restrictions: Gallium, germanium, graphite export controls creating western supply urgency

- Deglobalization: Onshoring / friend-shoring reducing willingness to depend on single-source suppliers

- Pandemic supply chain lessons: Industrial buyers accepting higher costs for supply security and redundancy

The best why now slides describe the confluence of trends that’s made your startup uniquely possible today.

What gets VCs excited

- Customer pull: Evidence that buyers are seeking solutions today, not hypothetically in future

- Technology convergence: Multiple advances (characterization + AI + manufacturing) together enabling your approach for the first time

- Economic inflection point: Input costs, carbon prices, or competing technologies crossing threshold that changes adoption math

- Regulatory deadline creating hard cutoff ("PFAS ban eliminates 70% of current solutions by 2028 with no qualified replacements")

- Supply chain crisis: Geopolitical event or concentration risk driving customers to actively seek alternatives now

Red flags

- Assuming gradual tech adoption curves when materials typically have long year qualification cycles

- "Why now" based entirely on your technology breakthrough, not market/regulatory changes

- “Why now” based on a commodity price spike - your business must be able to survive underlying commodity price swings

- Ideas that have failed before without clear explanation of what's fundamentally different

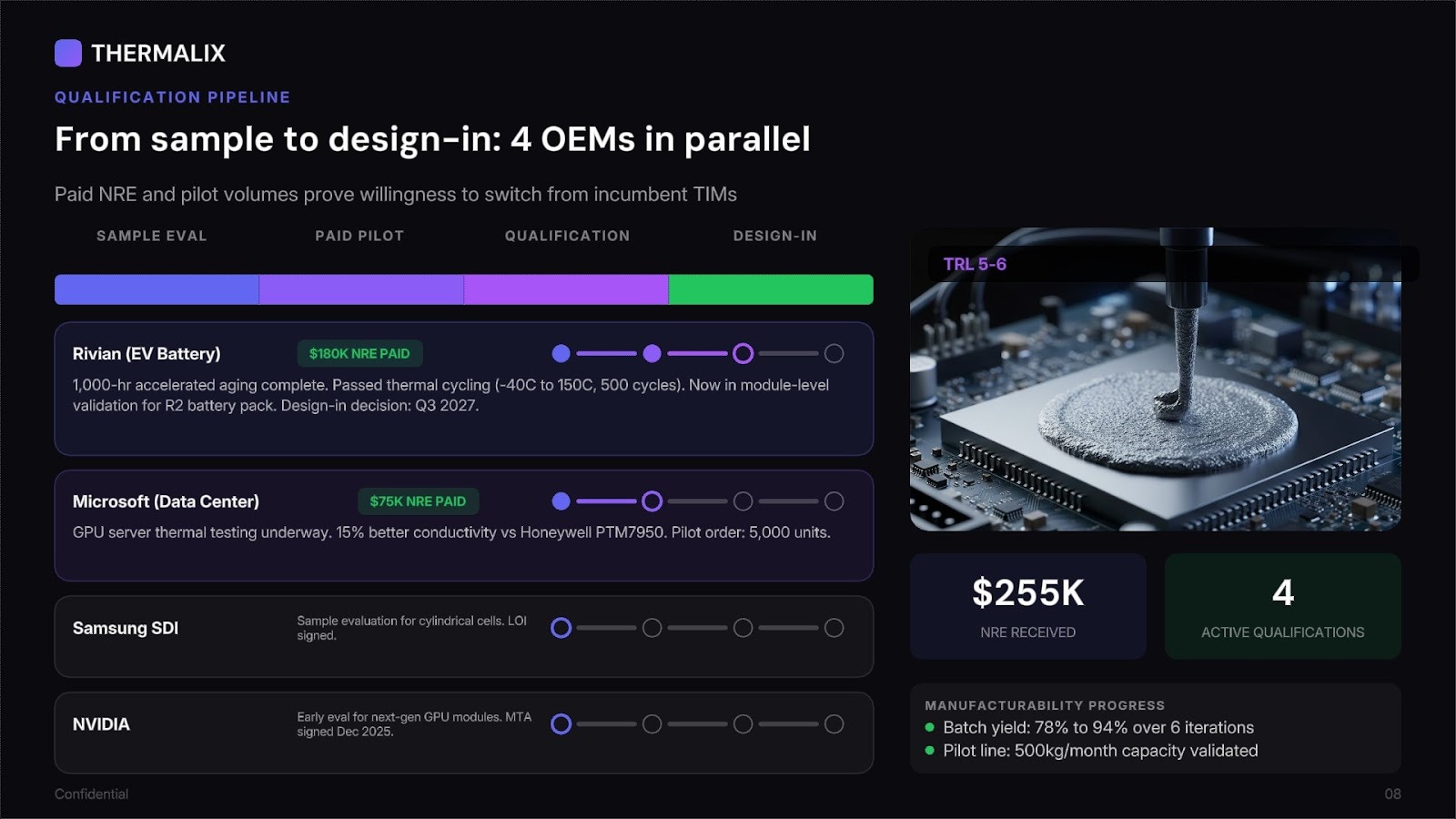

Traction

How to show there's demand for your product before the market has adopted it

In order of least to most convincing, there are three ways you can demonstrate your traction to VCs.

Deep problem understanding: Show you grasp your customer's specific challenges by answering: How many customers have you spoken to? Do you understand their purchase economics? Are you solving concrete problems like grid congestion or supply chain gaps? What makes this urgent now versus a future hypothetical?

Working demos: Lab or pilot-scale demonstrations de-risk your technology and economics. Draw clear lines between your demo and what customers need to see for adoption—ideally captured through paid pilots. Bonus points if you’ve been able to translate this into customer qualification or 3rd party validation.

Written commitments: Best case: paid demonstrations, joint development agreements, or commercial agreements. Paid demonstrations carry much more weight than LOIs. Next best: LOIs specifying purchase conditions and pricing. Verbal feedback carries less weight.

Within this, there are four phases of qualification to be able to talk through that help show the traction you’ve been able to achieve:

Technical: Have you identified and taken measures to reduce real risks in real conditions? That looks like a prototype that hits the key physics numbers against incumbent processes, with reproducible data and clear error bars. It might be a weld process that matches or beats an existing procedure on penetration and defect rate, or a new thermal process that holds temperature uniformity over a full part (machining/casting/printing). Each time you knock out one of these uncertainties and can show clean before/after data, that is traction for an investor (but also your next potential customer) during a demo.

Commercial: VCs care less about how many logos you have and more about the depth of one or two relationships at seed. Strong traction is a design partner who is clearly a champion, gives you access to their process/data/engineering resources, and is willing to let your hardware touch something that matters to them. That relationship can be a paid NRE or pilot, even small, tied to a specific line or part family. If far along enough, we want to be able to reference a plant where you have gone through several iterations and the operators or engineers can describe, in their own words, how the system improved something they already measure.

Sales acumen and progress: In selling into manufacturing fabs, the buyer is usually the plant manager, the shop owner, the operations lead, the welding superintendent, or the head of machining. IT and OT can be involved only when data leaves the shop. In the case of a factory deployment, the sales motion almost always begins with a pilot cell or workstation, usually on a non-critical job. Paid pilots are better than free ones because shops commit resources. They will never risk their best job first, so expect to start on work that's important enough to learn from but not important enough to risk the business.

In procurement, we often see friction with safety requirements, insurance, welding codes, quality certifications, or union constraints (we've seen this in steel and rebar automated manufacturing in the US). Additionally, anything that requires significant downtime or reorganizing a shop floor has low odds of success for an initial pilot. Lastly, we've seen black-box models fail because weld engineers and machinists must understand why a system changed heat input, toolpath, feed, speed, etc. A good way to start is by removing this risk outright depending on the job. If possible, start with contract manufacturing first.

Demonstrating a path to scale: SpaceX's early traction (in one form) was convincing engineering hires from TRW, Boeing and NASA to join before Falcon 1 worked, and then proving they could manufacture and iterate Merlin engines repeatedly until performance stabilized. That combination of top technical talent choosing to stake their careers on the effort, plus a few early builds that show the team can close the gap between theory, prototype and repeatable production is massive. If a startup can demonstrate that it has drawn in unusually strong engineering hires, built a small version of its system more than once, reduced variance between iterations and identified the bottlenecks that matter most for scaling.

The best traction slides show how far along these spectrums you’ve been able to reach.

What gets VCs excited

- Multiple customers in parallel qualification processes

- Paying customers: Any revenue or paid pilots show customers have budget and urgency

- Tier 1 customer validation: Fortune 500 or industry leaders testing your material (easier to sell to followers)

- Specific qualification milestones achieved: "Passed accelerated aging tests, now in field trials"

- Letters of intent with concrete terms: volumes, pricing, qualification criteria, timelines

- Successful pilot scale-up: Demonstrated you can make material at quantities customers need for testing

- Customers willing to do reference calls: Demonstrates deep conviction and trust between you and your customer

Red flags

- No samples in customer hands despite being 18+ months post-founding

- LOIs without specifics

- Only talking to one customer (concentration risk and suggests limited TAM)

- Customers only interested "if price drops by 50%" (suggests economics don't work)

- Traction entirely from grants/government funding without commercial interest

- Generic customer conversations without progressing to technical evaluations

Business Model

How VCs think about your economics

Your business model slide should include the basics of how you make money, the high level economics of price point to end customers, and margin you are able to achieve yourself.

Within materials and industrials, it’s about being able to show the economics you provide to customers: cost to implement, their economic benefit, and the payback period (if introducing new equipment). Your own business model should show the cost to your customer, the cost of production, and your margins.

What gets VCs excited

- Clear path to strong gross margins at commercial scale with realistic volume assumptions

- Unit economics improving rapidly with scale and learning curve effects demonstrated in early production

- Customer economics showing 3-10x+ ROI, or economic/product improvements

- Asset-light approach using contract manufacturers reducing capex requirements to scale

- Drop-in solutions that work within existing production/distribution workflows

Red flags

- COGS never reaching competitive levels even at massive scale

- Gross margins that are materially worse compared to your existing competition.

- Requiring immense capex to reach minimum viable scale

- Price point requiring customer to completely re-engineer their product

- Economics dependent on by-product credits or carbon credits that aren't guaranteed

- No clear understanding of cost structure

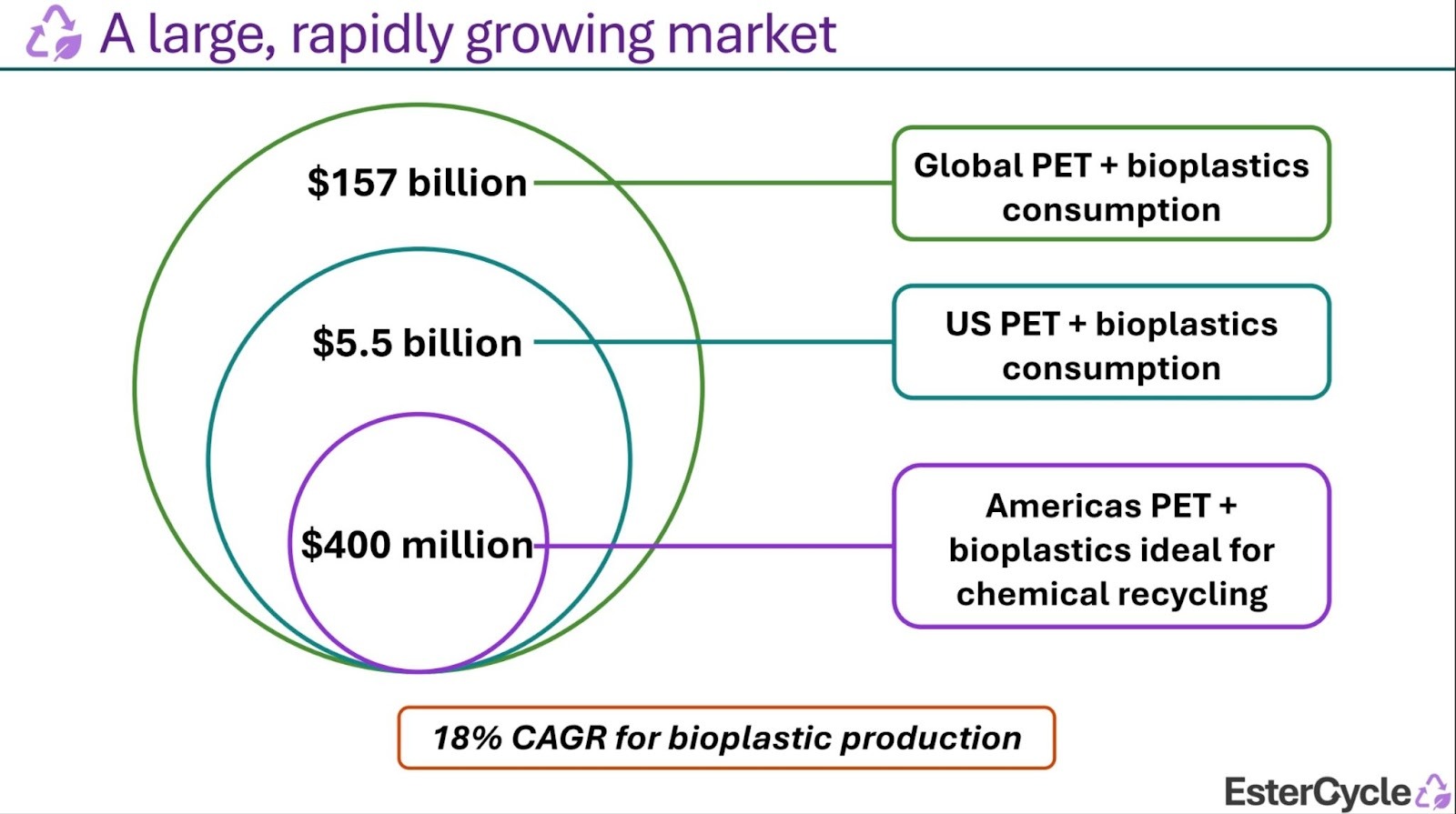

Market Size

Why bottom up beats top down

Your market sizing slide should be broken down into your:

Total Addressable Market (TAM) The total revenue opportunity if you achieved 100% market share across all potential customers globally. Total potential customers × Annual revenue per customer

Serviceable Addressable Market (SAM) The portion of TAM you can realistically reach given your business model, geographic focus, and current capabilities. Customers matching your target profile and location × Annual revenue per customer

Serviceable Obtainable Market (SOM) The market share you can realistically capture in the next 1-3 years, accounting for competition and resources. SAM × Realistic market share % that you could target over the next few years

This method of calculating these numbers is much preferred to “top down” market sizing, where you infer total demand based on high level industry numbers. This is because VCs want to understand how large your business can get - the TAM might be $5B, but if you price 1/10th of comparable products, the amount of market you can capture might be $500M.

Though it is acceptable to lean towards top down if bottom up is hard to quantify, and it is ok to use projections for market size so long as it’s clear how you’re arriving at your conclusions (ie TAM is based on 2030 estimates).

What gets VCs excited

- Multiple independent paths to significant revenue

- TAM expanding as price decreases or performance improves

- Entering existing markets with established demand vs. creating new markets requiring behavior change

- Market size validated by customer conversations

- Growing markets driven by electrification, decarbonization, reshoring, or regulatory mandates

- An addressable market that can support the math of returning an investors fund (ideally a few times over). Requires a perspective on your current round size / entry price and future dilution.

Red flags

- Top-down from massive commodity markets

- Ignoring incumbent stickiness ("We'll replace all steel in automotive" without acknowledging qualification barriers)

- Market size entirely dependent on winning single large customer or application

- Addressable market under $500M total

- No segmentation or prioritization - treating all applications as equally accessible

Go to Market

Showing you can become big enough, fast enough

This slide should outline who your customers will be, how you reach them, and how you will stage your GTM if your customer type changes with scale. Within the pitch, the most important question to answer is how your GTM motion can support a venture scale amount of revenue (usually $100M+) within the decade timeframe of a venture fund. VCs will generally use this slide to get to understand your depth of knowledge on the sales cycle as well.

Specific to materials and industrials, you must take into account the qualification and evaluation process of your end customers. Are there initial markets with easier ability to move quicker and have a burning problem to address?

Your GTM slide should describe who you’re targeting, and how you plan to sequence your GTM over time.

What gets VCs excited

- Named target customers with specific contact and engagement status

- Founder/team with existing relationships in target industry

- Multiple customer pathways that don't keep you stuck to one customer type

- Clear decision-making process mapped out: who influences (R&D, operations), who approves (procurement, finance), timeline and criteria for each stage

Red flags

- Vague GTM ("We'll sell to chemical companies") without named targets or specific approach

- Underestimating qualification timelines

- No plan for technical support/customer service

- Targeting too many diverse industries simultaneously

- No strategy for dealing with incumbents' customer lock-in

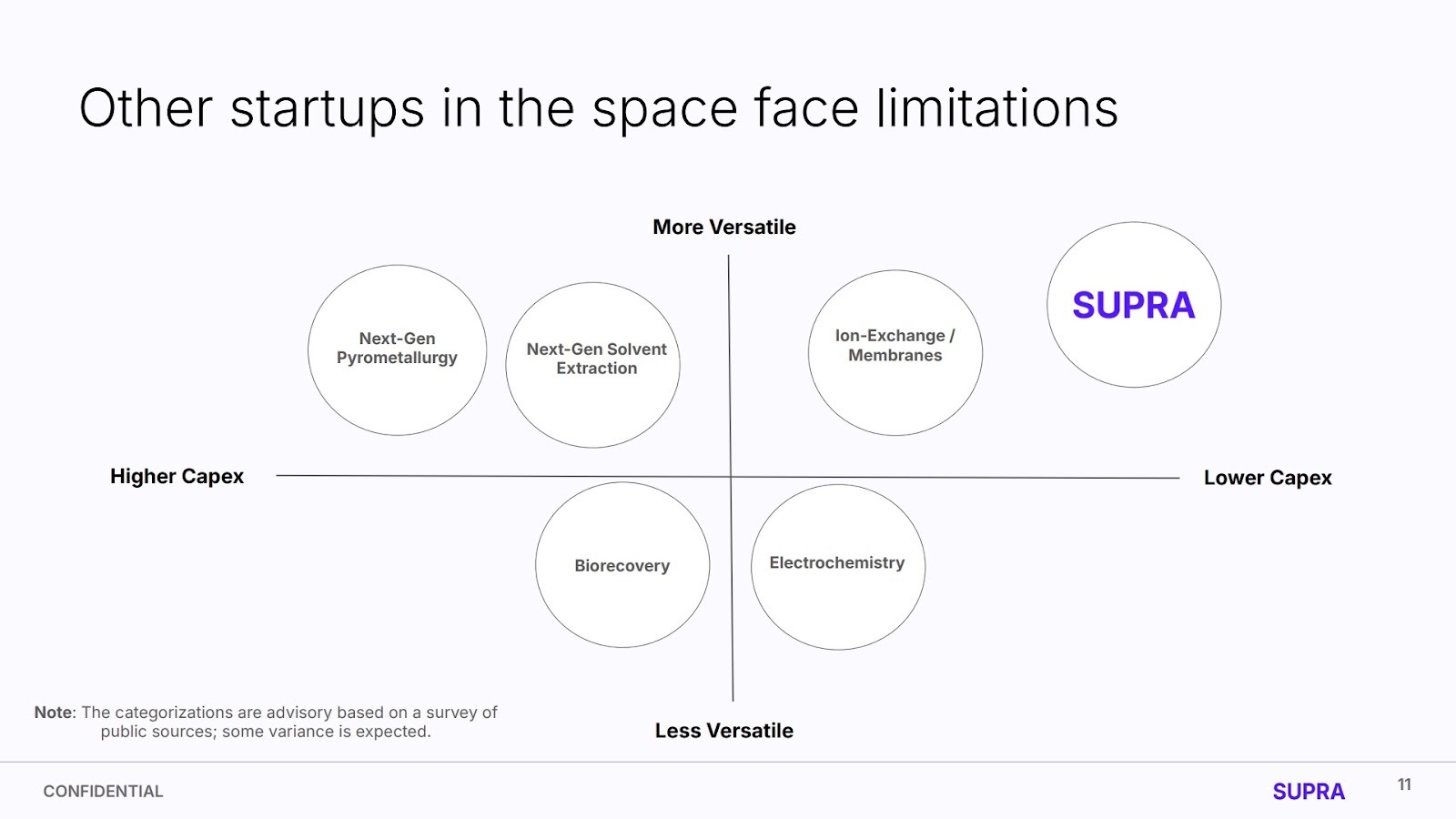

Competition

As markets become crowded, how to create defensibility

The strongest defensibility arguments show your solution is directionally impossible or highly unlikely for top incumbents to build themselves. It should be technically novel, challenging to replicate without your team's specific expertise, and protected by IP. Over time, becoming a trusted industry leader and achieving economies of scale creates durable advantages over future competitors.

Defensibility generally comes from IP protection, process know-how, and eventually customer lock-in through qualification and manufacturing economies of scale. Your competitive positioning must show why incumbents won't simply copy your approach, and why other startups can't replicate what you've built.

If you’re manufacturing something yourself, you must be able to show a glide path to economics that can’t be beat by the incumbent producer. Often, they’ll have distribution, economics, and customer entrenchment that can be challenging to overcome.

Another common pitfall is assuming too broad of a generalizability for inputs in processes to manufacturing facilities. We've seen many general factory-floor robotics aimed at broad labor replacement. The vision of fully lights-out production lines has pulled in billions from SoftBank, Tesla (Optimus), Figure AI, Agility Robotics, and a long tail of Chinese contenders. A true general-purpose humanoid still costs $150K+ per unit, breaks often, and moves slower than a tired human. Factories can solve a large swath of repetitive tasks with $20 - 50K robotic arms. The areas in manufacturing short on labor need 10-100x cheaper robots to make the math work on 100% automation.

On the services side, on-demand fabrication networks and manufacturing marketplaces are crowded. The barriers to entry are low and the path to defensibility is unclear without proprietary automation or a true tooling advantage. Across all these areas, the core challenge is the same with too many companies chasing broad narratives or macro rather than a specific process constraint they can own.

Your competition slide should demonstrate how you shape up compared to incumbent, existing processes, and other startups.

What gets VCs excited

- Multiple overlapping defensibility mechanisms (IP + customer lock-in + manufacturing know-how)

- Broad patent coverage making design-arounds difficult

- Proprietary access to key inputs or manufacturing capabilities

Red flags

- Patents with narrow claims easily designed around

- Claiming no competition when large chemical companies could enter if market proves attractive

- Defensibility based solely on being first without structural barriers to fast followers

- Trade secret strategy without ability to prevent reverse engineering

Team

What makes for a world-class founding team?

At Julian Capital, our deeptech seed fund that invests in many advanced manufacturing companies, one of the things we care most deeply about is the founding team — more often than not, it’s the deciding factor at the seed stage. We've written about what makes a great founding team here. In short, we're excited by founding teams who are:

- Commercially minded with technical depth

- Building their life's work—the culmination of their career or their final pursuit

- Ambitious enough to scale to $1B+ valuation

- Relentlessly resourceful with high agency

- Persuasive and authentic storytellers

- Comprehensive in thinking through all business avenues (GTM, competitive landscape, bottom-up TAM, etc)

The characteristics that define a strong founding team in deep-tech manufacturing are rooted in a strategic blend of technical mastery, operational literacy, and genuine customer empathy. They possess deep firsthand exposure to plants and production environments, translating this into true process literacy, and the commercial orientation needed to break into your end markets.

The team must collectively demonstrate mastery over deployment and economics. This includes comfort with the unglamorous realities of industrial hardware, certifications, and support operations to ensure the solution is productized and venture scalable. Above all, founders must know their numbers cold, providing transparent, physics-based unit economics.

Your team slide should demonstrate the degree to which your team has these qualities.

What gets VCs excited

- Teams with complementary technical depth, manufacturing experience, and commercial orientation

- Deep domain expertise with existing industry relationships and customer credibility

- Track record of attracting top technical talent

- Clear roles and decision rights among co-founders

- Demonstrated bias for action: prototype → pilot → customer testing progression in 12-24 months

Red flags

- Founders who can't articulate clear value proposition or customer economics

- No deep technical expertise on founding team

- No proof of commercial orientation

The Ask: Use of proceeds and round size

The ask shows how much you are raising and what you plan to accomplish with it. We wrote about choosing how much to raise here.

The path from lab synthesis to commercial production involves multiple expensive intermediate steps, and each one requires capital before the next can be justified. Your Ask must show that you understand this progression and are raising for the right step—not skipping ahead or raising too little to complete the current phase.

How to frame it:

Situate your raise within your scale-up roadmap. "We are raising $5M to complete pilot-scale production at 100 kg/batch, validate performance with three offtake partners, and generate the techno-economic data needed to support a Series A targeting a demonstration plant." Investors in this sector are used to multi-stage capital needs—show you've thought through all of them, even if you're only raising for the current one.

What gets VCs excited

- Raise sized to a specific scale-up milestone with clear technical targets (batch size, yield, purity, cost per unit)

- Identification of which technical risks the current round retires and which remain for future rounds

- Clarity on what infrastructure will be built vs. contracted (tolling agreements, co-manufacturing) to minimize capex

- Non-dilutive funding strategy—DOE, ARPA-E, NIST, or industry consortium grants—alongside equity

- Evidence that offtake partners will co-invest in or fund pilot scale

Red flags

- Raising for a scale step without clear performance benchmarks that define success

- Underestimating the cost and timeline of permitting, environmental review, or equipment lead times

- Assuming a single raise gets you to commercial scale without intermediate funding

- No mention of manufacturing partners or toll manufacturers as a path to reduce capex

- Round sized to hire scientists without a clear path to deployment or customer validation

Pitching: Do's & Dont's

Here's how (and how not) to pitch:

The best pitches are conversational. Answers should be succinct yet demonstrate depth of thought.

Great founders bridge vision with detail. They intimately understand their problem space and can explain it clearly—both the problem and the system around it. They understand the path to scale and can map how the business will evolve getting there.

The strongest pitches identify one painful process, such as weld quality, grinding, tube bending, plate cutting, or fixture setup. They show before-and-after proof from real production shifts with photos, videos, and scrap data. GTM plans that acknowledge pilot friction and provide a deployment playbook are impressive. Technical roadmaps that specify which risks remain show honesty (with credible ideas on how to overcome them over time). Founders who know (by heart) their supply chain, vendors, BOM, and governing constraints definitely stand out. Operator empathy is the final filter. Teams that speak the language of welders, machinists, and shop owners, even when they come in as an outsider into the space, shine through.

DO:

- Lead with customer problem and economics, not technical specs

- Be crisp on unit economics at scale: "Current COGS: $45/kg at 100kg/month. Target COGS: $18/kg at 50 tons/month. Sell at $30/kg for 40% gross margin."

- Acknowledge scale-up challenges honestly: "We've demonstrated this at 100kg scale. To reach commercial scale of 10 tons/month requires optimizing xyz." Credibility comes from understanding what you don't know yet.

- Demonstrate customer intimacy: Drop specific details showing deep industry understanding: "Automotive Tier 1s require PPAP submission with 300-unit trial run before design-in consideration, which takes 14-18 months."

- Address "why can't incumbents do this": Don't wait for this question. Proactively explain why incumbents aren't solving this (technical capability, market size too small for them, organizational barriers, IP position).

Common Pitching Pitfalls:

Unsurprisingly, founder stories without a sharp wedge fail to get traction. The pitch presents a vague "platform" solution without articulating a single specific use case. This lack of a clear entry point is often paired with an ROI story that is weak, depending entirely on soft benefits rather than quantifiable, part-level line improvements. Compounding this, many founders display a misunderstanding of the buying committee and the sales motion, treating challenging industrial sales as a simple SaaS or RaaS transaction.

Operationally, a pass often results from an unclear or unproven execution track record. Founders may lack prior experience owning a factory KPI (such as scrap rate, downtime, or cost per unit) signaling a theoretical rather than practical understanding of the customer's pain. While these things may be learned overtime, it can be hard to back when this manifests as an underestimation of deployment, integration, and support costs.

Founders from outside of industry often underestimate how slow and political industrial sales cycles really are. A pitch will spend 10 mins on physics and 2 mins on how adoption happens. Large manufacturers do not buy new technology just because the demo is impressive. While certain founders are excellent at raising on that alone, they spend the next 12 - 18 months just learning about how to sell into the industry.

Pitches often miss that a welding or machining change requires approval from quality, safety, and sometimes the end customer (esp aerospace, semis, automotive). Or that the tool must be interoperable with the users’ existing software and processes. This becomes a gating item.

Other traps materials founders fall into:

- Technology-first framing: Leading with "We discovered a new catalyst" instead of "We enable 40% cost reduction in hydrogen production." VCs fund businesses, not research.

- Underestimating capital needs: "We can scale to 1,000 tons/year with $5M" when realistically need $20M+ for facilities and working capital.

- Ignoring manufacturing complexity: Software founders entering materials vastly underestimate production challenges. Acknowledge if this is new to you and explain mitigation (advisors, hires, partners).

- Not knowing regulatory requirements: "We'll get EPA approval" without understanding what's required or timeline shows lack of homework.

- Missing customer decision-making complexity: Thinking CTO makes buying decisions when it actually requires procurement, operations, finance, QA, legal all to be aligned.

We hope this guide was useful to you! If you'd like to get in touch, don't hesitate to reach out to Julian.Capital, Steel Atlas, KDT, and Grid Capital, and apply in <1 minute to get put in touch with thesis fit investors for free at DeepChecks.VC.