Want to know exactly how VCs evaluate your biotech startup?

Together with 2048 Ventures —one of the leading biotech VCs—we’ve built this guide to unpack the inside baseball on how VCs evaluate biotech startups, and in turn how you can raise a successful round.

Informed by reviewing thousands of decks, and insights on which startups get the most traction on Deep Checks, this playbook helps put together a teaser deck that gets your first VC pitch scheduled.

We’ll go slide by slide on how investors decide whether or not to move forward with a startup. It’ll cover:

- Problem: Demonstrating how you’re solving a burning pain point for your customers

- Solution: Show why you have the best solution to this problem

- Technical risk: How to convince investors to get behind the remaining technical risk that you have

- Why now?: Demonstrating why your startup has just become possible to build. This is make-or-break for many pitches

- Traction: How to show there’s demand for your product before the market has adopted it

- Business Model: How VCs think about your economics

- Market Size: Why bottom up beats top down

- Go to market: Showing you can become big enough, fast enough

- Competition: As markets become crowded, how to create defensibility

- Team: What makes for a world-class founding team?

- The Ask: Use of proceeds and round size

- Pitching: Do’s and dont’s of pitching your startup to VCs

Problem

Demonstrating you're solving a burning pain point for your customers

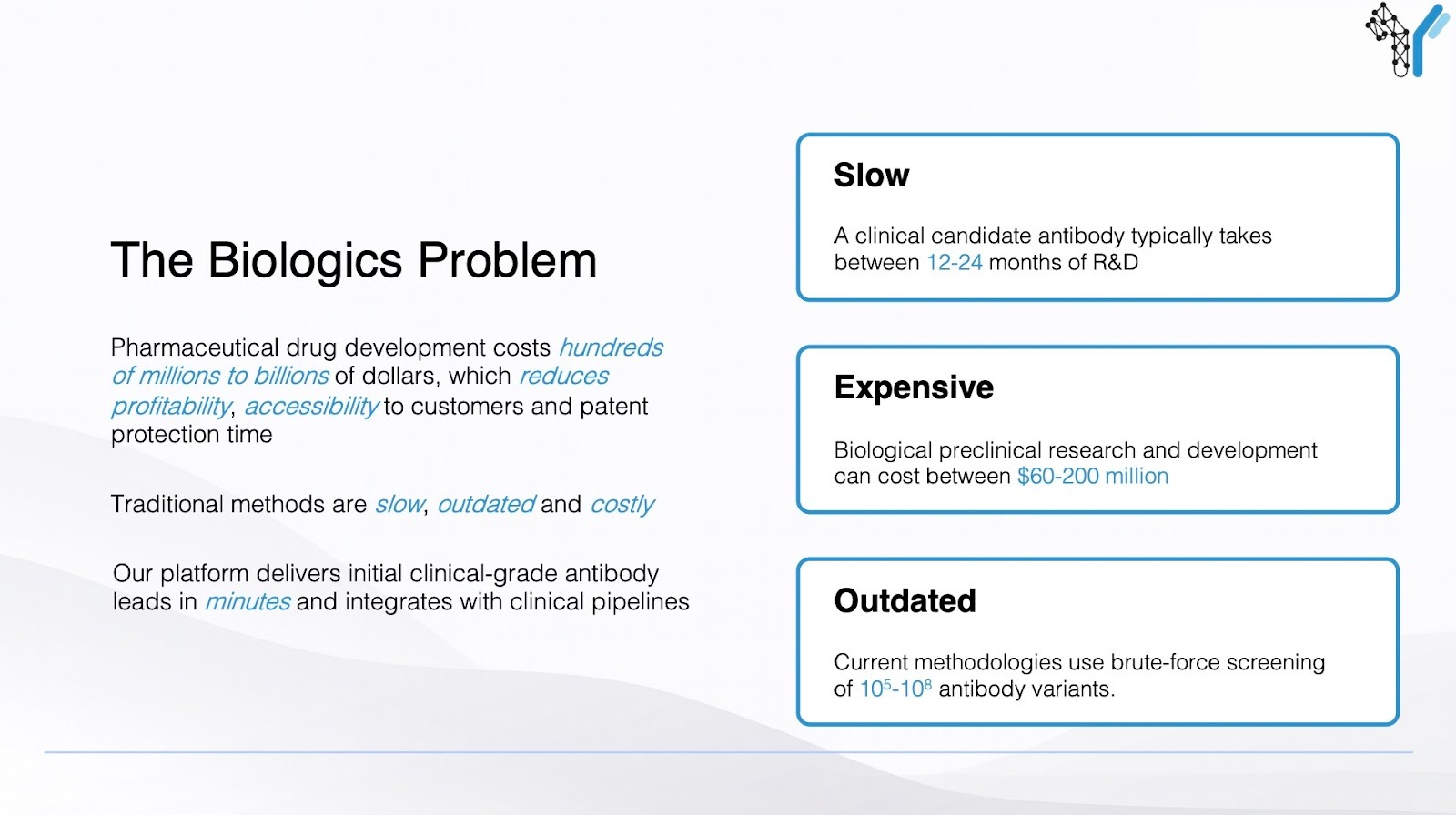

The problem slide exists to convince VCs the pain point you’re solving for your customers is a large, distinct, burning issue that they are willing to endure switching costs to solve.

Biotech problems must connect scientific innovation to clear unmet medical, commercial, or operational needs. The strongest biotech pitches frame the problem through three lenses:

- Clinical or Systemic Impact: Define the burden. For therapeutics, use epidemiology—how many patients suffer and why current standards fail (e.g., 5-year survival <20%). For non-therapeutics, define the "throughput wall" or "accuracy ceiling"—how current methods limit progress (e.g., "90% of drug candidates fail in Phase 2 due to non-predictive models").

- Technical Limitation: Articulate why existing solutions are inadequate. In therapeutics, this is high toxicity or low response rates. In tools/platforms, this is a lack of resolution or speed (e.g., "current sequencing cannot resolve structural variants, leaving 20% of rare diseases undiagnosed").

- Economic Burden: Demonstrate viability. For therapeutics, this might be treatment costs exceeding $150K-$300K with poor outcomes. For non-therapeutics, this is the "Cost of Failure"—biopharma spending $2B+ annually on R&D that hits a dead end due to poor target validation.

Your problem slide should describe the explicit commercial need you are addressing and show customer fluency: who experiences the pain, who is actively seeking a solution, and who ultimately controls budget or adoption. In biotech, these are not always the same person. Each stakeholder may view the problem differently and founders should show they understand that dynamic.

The goal is not just to show that the problem exists, but that it is important enough to support a venture-scale company. You should connect the problem to a market large enough, urgent enough, and persistent enough to justify building a company around solving it.

What gets VCs excited

- A non-obvious insight: Make the investor realize this is an important problem they hadn’t been thinking about, but now can’t ignore.

- Large Addressable Markets: 100K+ US patients for drugs, or a "horizontal" tool used by every Top-20 Pharma lab.

- Documented Failure of Status Quo: High disease progression rates despite treatment, or R&D bottlenecks where standard tools consistently fail to predict human outcomes.

- KOL and Stakeholder Pull: Evidence that key opinion leaders, patient advocacy groups, or lab heads are actively seeking and publishing on the need for your specific solution.

- Regulatory/Reimbursement Clarity: Precedents for FDA accelerated approval (therapeutics) or clear CMS reimbursement pathways/ISO standards (diagnostics and tools).

- High "Switching Value": A solution that is not just 10% better, but 10x faster, cheaper, or more accurate, making adoption inevitable.

Red flags

- "Solved Enough" Markets: Indications where recent breakthroughs have neutralized the "burning pain," or tools where existing legacy systems are "good enough" for current budgets.

- "Vitamin" vs. "Painkiller": Solutions that are scientifically interesting but don't address a mission-critical failure point (e.g., a slightly faster test for a non-urgent metric).

- High Workflow Friction: Products that require changing physician behavior or lab SOPs without providing a massive, quantifiable ROI.

- Niche Limitations: Rare conditions (<10K patients) without an expansion path, or tools for a dying technology stack.

- Biology over Outcomes: Focusing on "interesting mechanisms", with the problem retrofitted to fit the solution rather than how that mechanism solves a specific medical or industrial bottleneck.

- Over-indexing on the problem: Spending too much time explaining the problem without quickly connecting it to your solution.

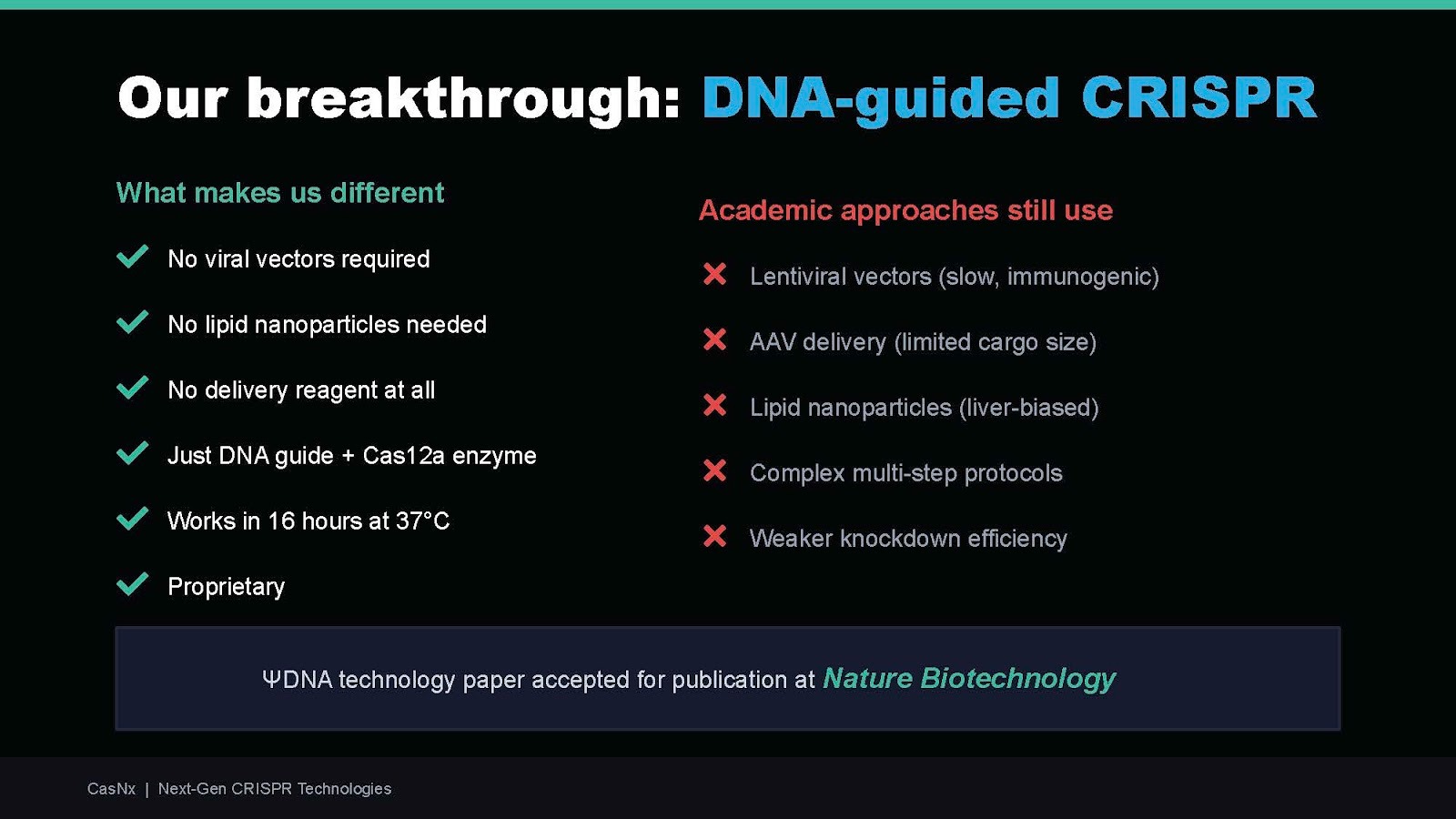

Solution

Show why your solution is the best solution to this problem

In biotech, "price" is rarely the winning benefit in a pitch—it’s efficacy, safety, or speed to milestone. So your solution should focus on clinical or technical superiority.

This slide should bridge scientific innovation with a value proposition such as:

- Performance Metrics that Matter: For therapeutics, use clinical endpoints: “Achieves 60% ORR vs. 25% for standard of care” or “reduces toxicity from 45% to 12%.” For non-therapeutics, use throughput and accuracy: “Screens 10,000 compounds/week vs. 100/week” or “Achieves 98% specificity, reducing false positives by 60%.”

- Mechanism-of-Action (MOA) Clarity: Therapeutic: “Our bispecific antibody blocks VEGF-A and Ang-2, preventing resistance.” Non-therapeutic: “Our microfluidic chip captures rare circulating cells via affinity-based sorting, preserving cell viability for downstream sequencing.”

- Differentiation from Alternatives: Explicitly compare to the status quo and late-stage competitors. Show why your approach solves the limitations of current options (e.g., “Unlike 2D cultures, our 3D organoids recapitulate human biliary architecture, predicting liver toxicity with 85% accuracy”).

- Feasibility and Integration: Demonstrate a clear path to the end-user. For drugs, show manufacturability (CMC) and a clear Phase 1 design. For tools, show "plug-and-play" compatibility with existing lab equipment (e.g., "Integrates with standard Illumina flow cells").

Always include proof-of-concept data—cell line data showing on-target activity, animal model data demonstrating efficacy, or pilot data showing your tool outperforming the current gold standard.

Your solution slide should detail the customer specific metrics that are improved by your clinical or technical advancements.

Prioritize clarity over complexity. If an investor cannot quickly grasp what you built and why it’s better, it creates friction for the rest of the pitch.

What gets VCs excited

- Best-in-Class or First-in-Class Profile: A solution with the potential to command premium pricing or become the "new standard" for an entire R&D workflow.

- Strong Validation Packages: For therapeutics, multiple animal models showing dose-response. For platforms, side-by-side comparisons against the current market-leading tool showing superior data quality.

- Combination or Expansion Potential: Therapies that work with existing standards, or platforms that address multiple therapeutic areas (e.g., a delivery system that works for mRNA, DNA, and CRISPR).

- Precision and Enrichment: Solutions that use biomarkers or specific data filters to identify the exact patients (or molecules) most likely to succeed, significantly de-risking the next stage of development.

- Scalability: A clear path to manufacturing or mass production with sound underlying unit economics.

Red flags

- Me-too Solutions: Incremental improvements (10-15%) that won't convince a doctor to change their prescription or a Lab Manager to swap their equipment.

- Lack of Validation: Relying solely on in vitro data for a drug, or "simulated data" for a tool, without real-world or animal model confirmation.

- Complexity Overload: If you cannot explain the MOA or the "physics" of the tool simply, it signals a lack of clarity and future difficulty in sales or clinical training.

- High Adoption Friction: Solutions that require "rip and replace" of expensive legacy infrastructure or radical changes to clinical workflows without a massive, immediate ROI.

- Novelty without a Map: A new modality (like a novel gene editor or a complex diagnostic) that lacks a clear pathway for manufacturing, stability, or reimbursement.

- Over-engineered solutions: Technically impressive but unnecessarily complex relative to the problem being solved.

Technical Risk

How to convince investors to get behind the remaining technical risk that you have

After your solution slide, investors will want to know what your technology is, what your unique insight is, what remains uncertain, and how you plan to address the remaining risks

Acknowledging risk directly builds credibility. Investors are not looking for zero risk, they are looking for teams that understand and can manage it.

In showing this, keep in mind:

Investors typically accept engineering risk (if your team can credibly tackle it and it's technically feasible) but not scientific risk (where there’s still some chance that the product may never work). Early stage VCs want to know:

- What has been proven

- What needs to be proven

- Why you're confident you'll achieve this

Investors distinguish between biological risk (will the mechanism work in a complex human system?), technical risk (can we manufacture/scale/deliver this?), and execution risk (can this team navigate the regulatory and clinical hurdles?). Address each explicitly:

- Validation: Show proof-of-mechanism through genetic evidence, expression data in relevant samples, or pharmacological validation. Ideally, show that your intervention or tool is safe and predictable by referencing healthy volunteer data or pilot studies in real-world environments.

- Technical de-risking: Demonstrate you have solved the core "hard" problems. This includes manufacturability (titers, purity, or yield), favorable stability/shelf-life, and a clear "therapeutic index" or "accuracy margin" that shows the technology works reliably without hitting a ceiling or causing off-target effects.

- Path to maturity: List what is already proven (e.g., "Prototype validated in lab environment") versus what remains (e.g., "Scale-up to 500L" or "Human safety trials"). A clear development plan with staged de-risking allows investors to see exactly when their capital will unlock the next level of value.

- Regulatory and pathway clarity: Show an understanding of the requirements for your specific category. Whether it is an FDA registration path for an asset or ISO certification for a tool, demonstrating that you know the "rules of the game" reduces the perceived execution risk.

Investors accept technical risk if there is a clear, staged plan. Each milestone should reduce uncertainty before the next major capital deployment.

Your technical risk slide should show what’s been proven, and detail this pathway.

What gets VCs excited

- Strong validation from human data or primary samples: Germline variants, somatic mutations, or direct patient tissue results provide the highest level of confidence.

- Predictability: Data from models (computational, animal, or pilot-scale) that have historically predicted real-world outcomes in your specific field.

- Technical de-risking packages: Evidence of GMP-compatible manufacturing, favorable PK/PD or signal-to-noise ratios, and a clean safety or error profile.

- Validated biomarkers or metrics: Tools that enable you to measure response or accuracy in real-time, allowing for "fail fast" iterations and precision development.

- Precedent for the approach: Following validated formats (e.g., monoclonal antibodies or standard silicon-based sensors) is lower risk than entirely novel formats with no known manufacturing path.

Red flags

- Weak validation: Relying on a single model system or a "black box" mechanism that cannot be explained or replicated by third parties.

- Dismissed safety or error signals: Ignoring on-target toxicity or data inconsistencies in early work rather than addressing them with a technical fix.

- Unrealistic timelines: Claiming a 12-month path to market for a complex modality or a high-sensitivity tool without having a prototype or a manufacturing partner identified.

- Vague manufacturing strategy: Stating "we will outsource" without demonstrating that the process is actually transferable or identifying who has the capacity to build it.

- Relying on a single "hero" experiment: One successful run is not traction; VCs look for reproducibility and a robust data package across multiple conditions.

- Lack of clear de-risking plan: No clear experiments or milestones tied to the biggest unknowns.

Why Now

Demonstrating why your startup has just become possible to build

Many ideas have been tried before and failed to materialize. By describing what has changed in the world that makes it uniquely possible to build your business today, and what is fundamentally different now that prevents the same outcome, investors gain confidence that you aren't just repeating past mistakes.

The "why now" narrative usually centers on a convergence of scientific breakthroughs, technological enablement, and shifting market or regulatory dynamics:

- Scientific and technical catalysts: Point to specific breakthroughs from the last 3–5 years that act as a foundation. This could include the maturation of a specific modality, the release of a high-fidelity predictive model, or the availability of new high-resolution data sets that didn't exist a decade ago.

- Technology enablement: Explain how improvements in adjacent fields—such as computing power, automation, or gene synthesis—have reduced the cost or time required to execute your idea. If your approach was "impossible" in 2015 but "standard" in 2026, define exactly what changed (e.g., a 100x drop in sequencing costs or the arrival of specific editing tools).

- Regulatory and policy shifts: Highlight recent changes in how governing bodies view innovation. This includes new pathways for accelerated approval, updated guidance on digital or AI-driven tools, or shifts in reimbursement policies that make a previously "expensive" approach commercially viable today.

- Market and competitive inflection points: Identify recent failures in the field that validate the need for a new direction, or successful exits that prove the market's appetite. A "why now" is often built on the "whitespace" left behind by legacy approaches that have reached their performance ceiling.

The strongest narratives combine these factors: a specific scientific discovery made it possible, a technological drop in cost made it feasible, and a regulatory shift made it profitable.

In addition, a strong “why now” is also about why this company will matter even more in the years ahead. You need a clear “why then”: why this will become inevitable over time.

What gets VCs excited

- Multiple converging inflection points: When scientific, technical, and regulatory trends all point toward your solution simultaneously.

- Durable tailwinds: The underlying trends (scientific, regulatory, economic) should continue to strengthen over time, not just create a temporary window.

- Citing recent peer-reviewed validation: Referring to specific high-impact papers or clinical results from the last 24–36 months that de-risk your core thesis.

- Solving a new problem created by a recent success: For example, the success of a first-generation technology often creates a secondary bottleneck that your company is perfectly positioned to solve.

- Tangible cost/time reductions: Hard data showing that what used to take years and millions of dollars can now be done in months for a fraction of the price.

- Recent regulatory precedents: Pointing to a similar technology or product that received a favorable ruling or designation in the last year.

- Team-timing fit: why your team is uniquely positioned to act on this inflection point. For example, access to new data, key insight from prior failures or proximity to emerging workflows.

Red flags

- Generic "AI" or "Innovation" claims: Vague statements about technology advancing without specific examples relevant to your workflow.

- Citing old inflection points: If your "why now" happened in 2010, the question becomes why a dozen other companies haven't already won the market.

- Ignoring past failures: Claiming an idea is "new" when a similar version failed three years ago without explaining what has technically changed to prevent a repeat.

- Relying solely on market size: Markets being "large" or "growing" isn't a "why now". Investors need to see a specific catalyst for change.

- "Wait and see" regulatory hurdles: If your success depends on a law that might pass or a guideline that might change, you are pitching a political bet, not a technical one.

Traction

Traction in biotech is not about user growth; it is about the systematic accumulation of evidence. VCs evaluate your progress based on a hierarchy of "De-risking Milestones" that move from theoretical potential to validated reality:

- Formal Validation & Clinical Data. The highest form of traction. This includes human clinical data (safety or early efficacy), paid research collaborations with Top-20 Pharma, or commercial licensing agreements with "skin in the game" (upfront payments).

- Regulatory & Technical Momentum. This includes formal FDA designations (Orphan, Fast Track, Breakthrough), positive pre-IND feedback, and a defensible "Freedom to Operate" (FTO) analysis. It also covers "human-relevant" proof points, such as data from primary patient cells or organ-on-a-chip models that outperform legacy animal standards.

- Strategic Partnerships & Internal Pipeline. For platform companies, this is measured by "internal pipeline" progress—showing the tech can generate multiple distinct leads. This tier also includes written commitments like Letters of Intent (LOIs) from Phase 2 investigators or pharma partners that specify "if/then" triggers for future deals.

- Stakeholder & Ecosystem Buy-in. Support from a high-engagement Scientific Advisory Board (SAB) of active industry leaders, collaborations with academic medical centers, and non-dilutive grants from major foundations (e.g., Bill & Melinda Gates Foundation, Michael J. Fox Foundation).

For platform-based companies, traction is also measured by "internal pipeline" progress—showing that the technology can successfully generate multiple distinct leads or applications in parallel, rather than being a "one-hit wonder."

Your traction slide should demonstrate how far along these axes you’ve been able to achieve.

What gets VCs excited

- Human data or human-relevant proof points: Any data showing that the technology behaves as expected in human systems, even in small pilot cases or healthy volunteer studies.

- Regulatory momentum: Recent formal designations or completed meetings with agencies that provide a clear, accelerated roadmap to market.

- High-engagement advisors: SAB members who are not just names on a slide but are actively involved in designing protocols or reviewing data.

- Pharma interest with "skin in the game": Option agreements, research funding, or licensing discussions that provide commercial validation of the science.

- Clear path to pharma engagement: Even without active partnerships, showing a clear understanding of what pharma needs to see to engage (e.g., required data package, validation standards) and how you’re building toward it.

- Repeatability: Evidence that your platform or tool can produce consistent results across different targets, indications, or lab environments.

Red flags

- Reliance on "low-fidelity" data: Presenting only basic cell-line or animal data without a plan to move toward more predictive, human-relevant models.

- Passive advisory boards: A list of prestigious names who have no active role in the company or whose expertise is outdated for your specific technology.

- No regulatory or IP strategy: A lack of clarity on how you will protect your work or navigate the formal approval process suggests a lack of execution sophistication.

- Partnerships without "teeth": Unfunded academic collaborations that lack a clear path to commercial use or pharma-level validation.

- Lack of focus: For platforms, trying to solve too many problems at once without a "lead" program or application that is approaching a major value inflection point.

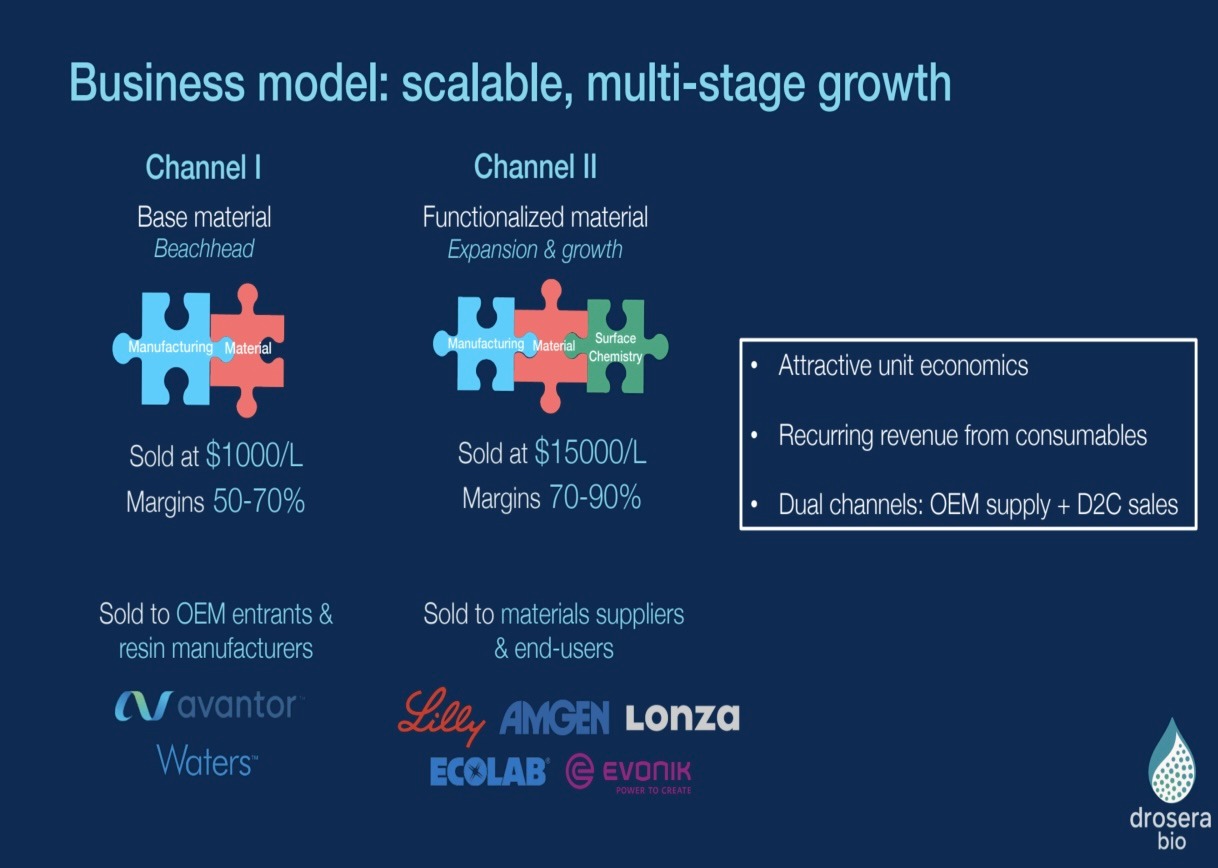

Business Model

How VCs think about your economics

Your business model slide should be immediately clear: who pays, for what, and how revenue scales over time. It should include the basics of how you make money, the high level economics of price point to end customers, and margin you are able to achieve yourself.

Biotech business models generally fall into three categories: asset-based, platform-based, or hybrid models. VCs evaluate these based on the "Value Inflection Points"—the specific milestones where the company's valuation jumps significantly:

- Product-driven revenue: This model focuses on developing a specific asset (a drug, a diagnostic, or a high-value reagent) to sell to a larger player or commercialize directly. Economics are driven by peak sales potential, which is a function of the addressable population, pricing (benchmark against current standards), and market share.

- Platform and service revenue: This involves licensing technology or providing a service to multiple partners. Revenue comes from upfront payments, research funding, and "bio-bucks" (milestones and royalties). VCs look for "platform leverage"—the ability to generate multiple revenue streams from a single core technology without a linear increase in costs.

- Hybrid models: This is often the most attractive to VCs. You use a platform to generate an internal pipeline of high-value products (capturing 100% of the upside) while simultaneously partnering with others for non-core applications to generate non-dilutive cash flow, validate the tech and show market pull

- Reimbursement and COGS: For anything entering the clinical or diagnostic workflow, you must demonstrate a path to reimbursement. VCs analyze your "Gross Margin"—the difference between the price a payer is willing to pay and your Cost of Goods Sold (COGS). High-margin biotech (60-80%+) is essential to offset the high R&D costs.

Key metrics VCs evaluate: time to revenue (often 5-10 years), capital efficiency (how much dilution is required to reach a major data readout), and the "Exit Multiple" (what similar companies sold for at a similar stage of maturity).

Your business model slide should detail the cost to your customer, and your margin from sales or license agreements.

What gets VCs excited

- Multiple paths to "liquidity": A company that could be a candidate for an IPO, a M&A exit by a large pharma, or a series of high-value licensing deals.

- Scalability without massive headcount: Using automation or software-like workflows to increase output without a proportional increase in expensive lab labor.

- Clear reimbursement precedents: Pointing to existing codes or "Value-Based" payment models that already cover similar technologies at the price point you are targeting.

- High "Bio-buck" potential: Platform deals with significant back-end royalties that provide long-term, high-margin upside.

- Capital efficiency: Reaching a "Value Inflection Point" (like a successful pilot or Phase 1 data) on a relatively small amount of seed or Series A capital.

- Clear sequencing of the business model: A thoughtful plan for how the business evolves over time, with a clear starting point, rather than trying to pursue every possible business model at once.

Red flags

- Unrealistic pricing: Assuming a premium price point in a market where existing alternatives are cheap or where payers are actively pushing back on costs.

- Low-margin "Services" traps: Business models that look more like a consulting firm or a contract research organization (CRO) than a scalable technology company.

- High "Customer Acquisition Cost" (CAC): Models that require a massive sales force to reach fragmented, low-budget customers (e.g., individual academic labs) for a low-cost product.

- Ignoring the "Valley of Death": Not accounting for the significant capital required between the initial prototype and the final regulatory approval.

- No "Wholly-Owned" upside: For platforms, licensing away all the best applications early on, leaving the startup with only the "scraps" of their own technology.

- Speculative build: Investing heavily in development without clarity on downstream buyers, partnership interest, or commercial path.

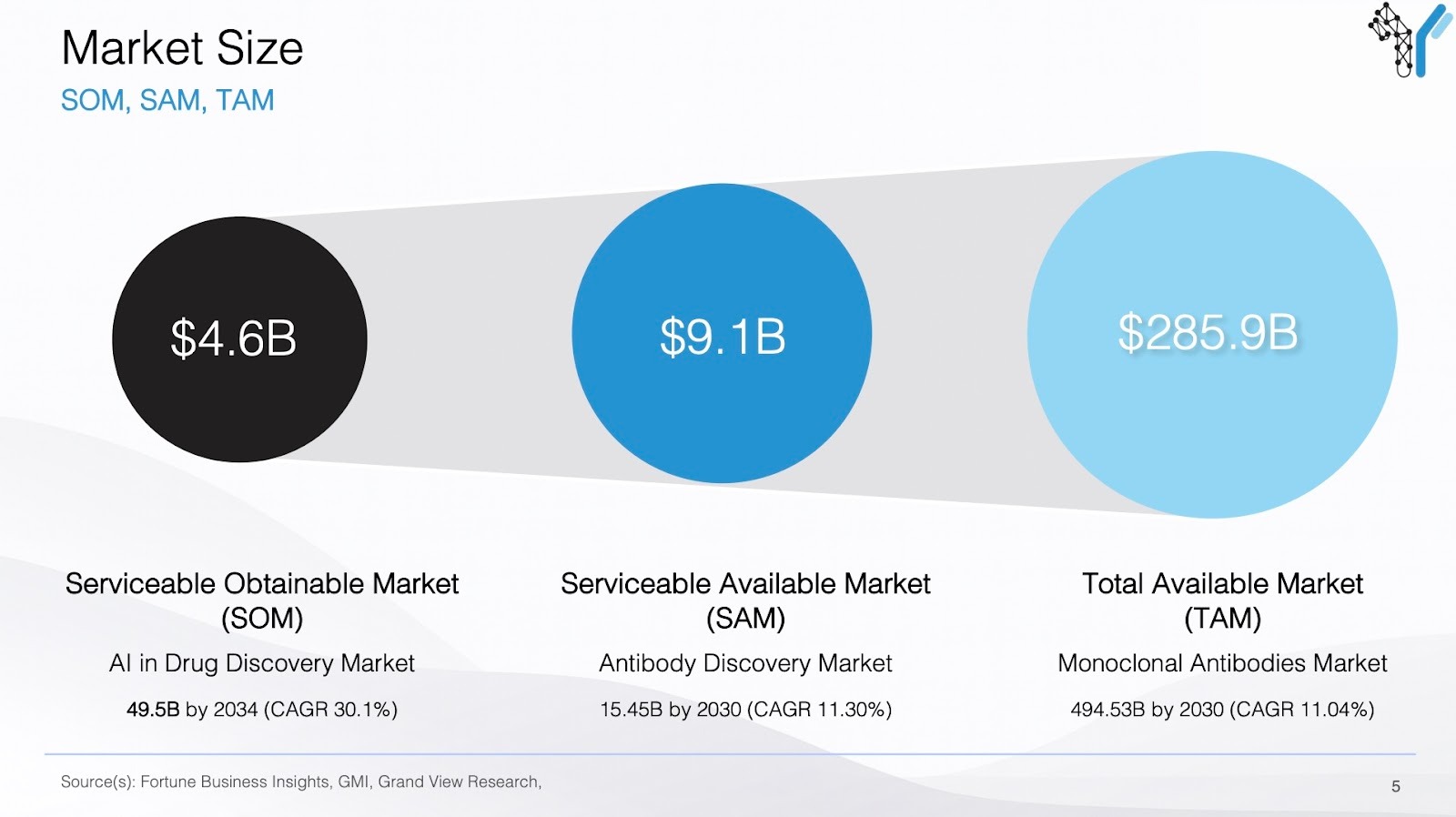

Market Size

Why bottom up beats top down

Your market sizing slide should demonstrate that you understand exactly who will pay for your solution and how many of them exist in the real world. It should also be easy to understand at a glance. Investors should quickly grasp how big this can get and what assumptions drive that outcome.

Market sizing requires a granular analysis of epidemiology, the technical landscape, and realistic adoption rates. VCs look for "Bottom-Up" logic rather than generic industry statistics:

- Total Addressable Market (TAM): The global universe of potential users or patients. For a therapeutic, this is the total incidence or prevalence of the condition. For a tool, it is the total number of labs or R&D programs globally that face the bottleneck you solve.

- Serviceable Addressable Market (SAM): The portion of the TAM you can actually reach given your specific technology, geography, and regulatory status. This accounts for patient sub-types (e.g., specific biomarkers) or lab types (e.g., high-throughput screening vs. basic research).

- Serviceable Obtainable Market (SOM): Your realistic market share at peak maturity. This accounts for competition, the speed of clinical adoption, and the "inertia" of legacy systems.

Your sizing must be based on a defensible price per unit or per year. This should be benchmarked against the cost of the problem you are solving—such as the price of the current standard of care or the cost of a failed R&D cycle.

A credible biotech market size is built on "Patient Flow" or "Workflow Volume": Start with the total population, subtract those who are ineligible, and multiply by a realistic price point supported by reimbursement or budget precedents.

What gets VCs excited

- Blockbuster potential: A clear path to $1B+ in peak annual revenue supported by rigorous data, not just "1% of a $100B market" logic.

- Expansion opportunities: An initial market that is defensible and profitable, with "adjacencies" that allow the technology to move into larger indications or broader industries over time.

- High-value niches: Markets with smaller populations but high "unmet need" that allow for premium pricing and faster, more efficient paths to market.

- Validation via comparables: Sizing that aligns with the historical sales of similar successful products or tools in the same category.

- Growing "Problem" sectors: Markets where the underlying issue is becoming more frequent or more expensive (e.g., rising aging populations or increasing complexity in drug manufacturing).

Red flags

- Top-down "Fantasy" sizing: Claiming a massive market based on "total healthcare spend" or "total R&D spend" without connecting it to your specific product.

- Ignoring the "Line of Therapy" or "User Type": Sizing for every cancer patient when your drug only works in the 3rd line of treatment for a specific mutation.

- Unrealistic pricing assumptions: Projecting high prices without evidence that payers or lab managers have the budget or incentive to pay them.

- Static market views: Failing to account for upcoming competitors or generic entries that will shrink the available market by the time you launch.

- "Everyone is a customer": Claiming your tool is for "every scientist" without identifying the specific high-value users who will be the early adopters.

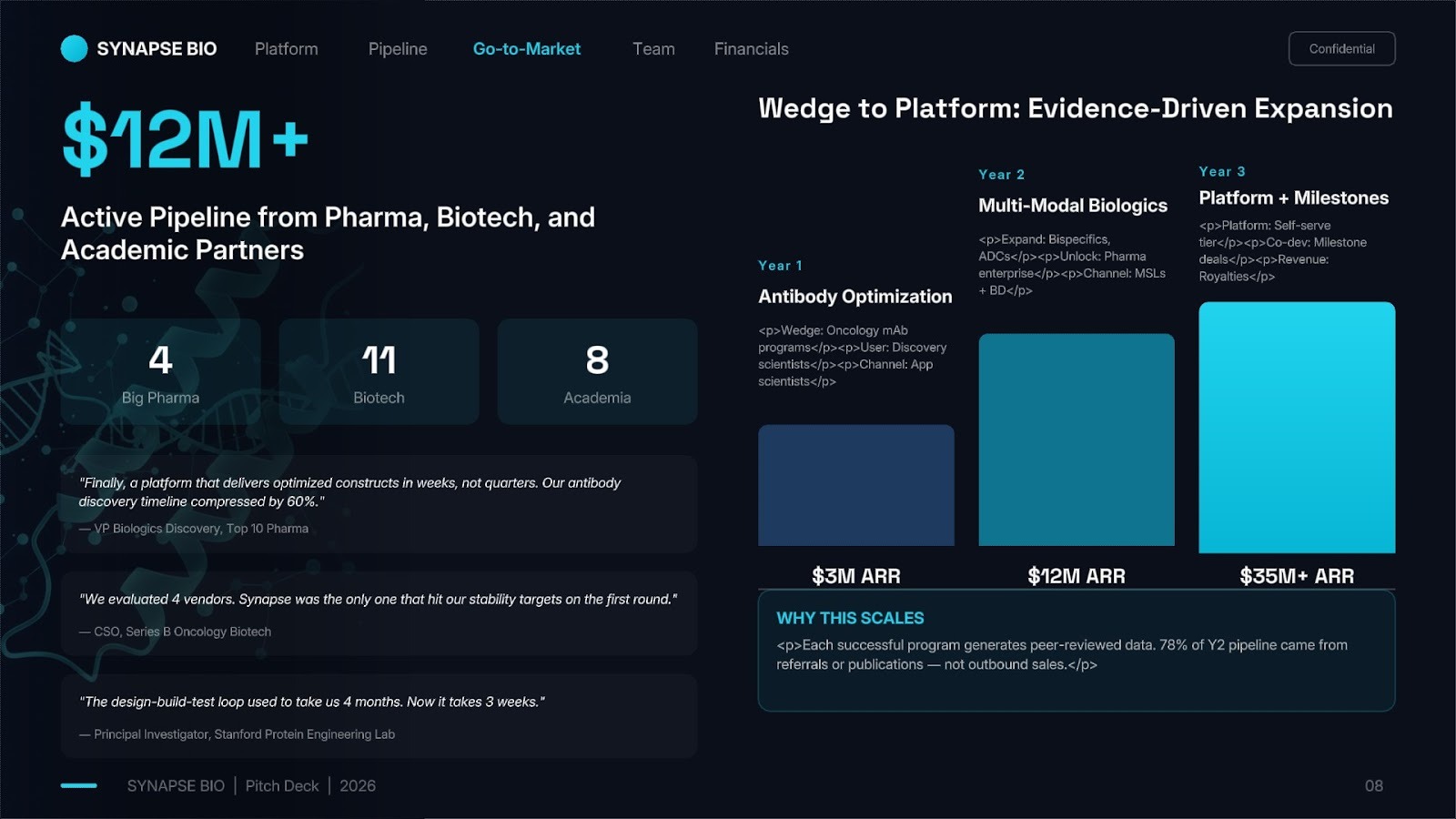

Go to Market

Showing you can become big enough, fast enough

This slide should outline who your customers will be, how you reach them, and how you will stage your rollout as your footprint grows. VCs use this to determine if you can support venture-scale revenue (usually $100M+) within the decade timeframe of a fund.

The go-to-market (GTM) strategy is defined by the technical category and the regulatory environment. It’s generally about navigating the gatekeepers of clinical or industrial adoption:

- Identifying the decision-makers: You must distinguish between the user and the payer. In a clinical setting, this is the prescribing physician versus the insurance committee; in an R&D setting, it is the bench scientist versus the head of procurement. Your GTM must address the incentives of both.

- Staging the rollout: Most biotech success starts with a "wedge" indication or a high-value pilot with a single "Top 10" partner. This provides the validation needed to expand into broader markets. Define your Phase 1 (early adopters/validation), Phase 2 (market expansion), and Phase 3 (broad commercialization).

- Sales and distribution channels: For concentrated markets (like oncology or specialized R&D), a small, highly technical field force of MSLs (Medical Science Liaisons) or application scientists is often enough. For broader markets, you may need strategic partnerships with established distributors or "Big Pharma" commercial arms to reach the necessary scale.

- Managing the "Inertia" of the status quo: Biotech is risk-averse. Your GTM must include a plan for "evidence generation"—using publications, conference presentations, and real-world data to convince a conservative industry to swap a validated legacy process for your innovation.

Your GTM slide should address how you plan to go to market and get your first customers, and how you sequence customer types over time. Investors want to understand the initial motion that gets the product into real use.

What gets VCs excited

- Concentrated prescriber or buyer base: Markets where a 20-person team can reach 80% of the total revenue potential (e.g., specialized transplant centers or specific pharma R&D hubs).

- Strategic partnerships with "Built-in" scale: Agreements with major distributors or co-marketing deals with industry leaders that reduce your customer acquisition cost.

- Low barrier to adoption: Products that can be integrated into existing workflows with minimal training, hardware changes, or regulatory hurdles.

- High "Value-Based" pull: A strategy that aligns with current trends, such as tools that reduce hospital stays or platforms that decrease drug development timelines.

- Strong “Wedge”: A focused entry point with high probability of success.

- Clear "Wedge" to Platform expansion: Starting in a niche with zero competition to build a brand and cash flow before attacking a larger, more competitive market.

Red flags

- "Boiling the Ocean": Trying to sell to every doctor or every lab at once without a focused starting point.

- Underestimating the sales cycle: Assuming a 3-month sales cycle in an industry where procurement or clinical committees often take 12–18 months to make a decision.

- Ignoring the "Middleman": Failing to account for the influence of GPOs (Group Purchasing Organizations) or PBMs (Pharmacy Benefit Managers) in the US healthcare system.

- High "Rip and Replace" costs: A GTM that requires the customer to throw away millions of dollars in existing infrastructure to use your tool.

- No plan for "Post-Market" evidence: Assuming that getting a "stamp of approval" (FDA or ISO) is enough to drive sales without a plan for continuous data generation.

Competition

As markets become crowded, how to create defensibility

The strongest defensibility arguments show your solution is directionally impossible or highly unlikely for top incumbents to build themselves. It should be technically novel, challenging to replicate without your team's specific expertise, and protected by IP. Over time, becoming a trusted industry leader, compounding your data and achieving economies of scale creates durable advantages over future competitors.

Defensibility in biotech is rarely about being "first to market"; it is about "depth of moat." This includes your intellectual property (IP), your proprietary data, and your "regulatory head-start":

- Mapping the landscape: Identify three layers of competition: the current standard of care/tooling, late-stage clinical or technical pipeline competitors, and "alternative" approaches (e.g., a diagnostic that competes with a therapy). You should also account for emerging players and what others are building that could compete in the future.

- Intellectual Property and Freedom to Operate: Beyond just having patents, you must show a "moat" around your core innovation. This includes "composition of matter" patents, method-of-use patents, and trade secrets in manufacturing or data processing that are difficult for competitors to reverse-engineer.

- Data Moats and Feedback Loops: For platform or AI-driven companies, defensibility comes from proprietary datasets that improve the technology with every run. Explain how your data is "unique, high-fidelity, and non-public," making it impossible for a competitor to simply copy your algorithm.

- Switching Costs and Integration: Describe how your solution becomes "entrenched" in a user's workflow. This could be through integration into a clinical electronic health record (EHR), a validated laboratory SOP, or a specific regulatory approval that is tied to your unique hardware or software.

Your competition slide should demonstrate why your solution beats our incumbents and potential emerging competitors.

What gets VCs excited

- Dominant IP position: Owning the "foundational" patents for a new modality or a critical technical component that others must license to operate.

- Superior "Performance Delta": Being not just marginally better, but having a "step-function" lead in safety, efficacy, or speed that a competitor cannot bridge without a total redesign.

- Network effects or data flywheels: Systems where more users or more experiments lead to better results, creating a "winner-take-all" dynamic in a specific technical niche.

- High regulatory barriers: Having a head-start on a 5-to-10-year clinical or validation path that forces competitors to spend hundreds of millions just to catch up.

- "Manufacturing Moats": Proprietary processes (CMC) that allow you to produce a complex biological or tool at a cost or quality level that others cannot replicate.

Red flags

- The "Ostrich" approach: Claiming "no competition" usually signals a lack of market awareness or a market that is too small to be interesting.

- Focusing on "Features" over "Outcomes": Competing on "more buttons" or "faster processing" rather than the fundamental clinical or economic result.

- Weak IP strategy: Relying on generic software patents or "obvious" improvements that are likely to be challenged or easily designed around.

- Ignoring "Big Pharma" or "Legacy Tools": Failing to realize that the biggest competitor is often the "Good Enough" status quo that is already bought and paid for.

- Price as the only moat: Competing solely on being cheaper is dangerous in biotech, where R&D costs are high and a larger competitor can easily subsidize a temporary price war.

Team

What makes for a world-class founding team?

We've written about what makes a great founding team here. We're excited by founding teams who are:

- Commercially minded with technical depth

- Building their life's work—the culmination of their career or their final pursuit

- Ambitious enough to scale to $1B+ valuation

- Relentlessly resourceful with high agency

- Persuasive and authentic storytellers

- Comprehensive in thinking through all business avenues (GTM, competitive landscape, bottom-up TAM, etc)

The team slide is often the most important for early-stage VCs, as the technology will inevitably evolve. They are looking for a combination of "technical aptitude" and "commercial thoughtfulness."

A winning team must balance deep domain expertise with the ability to navigate the complex regulatory and financial milestones of the industry:

- The Technical-Commercial Bridge: The strongest teams feature a "Scientific Founder" with deep expertise in the core technology and a "Commercial Lead" who understands the clinical, regulatory, or industrial landscape. VCs look for a history of working together and a clear division of labor.

- Track Record of Execution: While not every founder is a serial entrepreneur, having team members or advisors who have "seen the movie before"—taking a product through the FDA, managing a major pharma partnership, or scaling a manufacturing process—drastically reduces the perceived risk.

- Scientific Advisory Board (SAB) Depth: In biotech, your advisors are an extension of your team. VCs look for "active" leaders—top-tier clinicians or researchers who are shaping the field and have a vested interest in your success, rather than just "logos" on a slide.

- Regulatory and Clinical Sophistication: Even at the seed stage, the team must show they understand the "rules of the game." This includes knowing how to design a trial, manage IP, and handle the "Quality Systems" required for biotech products.

Your team slide should demonstrate the relevant skillsets you have across these dimensions.

What gets VCs excited

- Founders with "unfair" expertise or a unique insight: Individuals who spent a decade researching the specific protein, pathway, or technical bottleneck the company is solving, or have directly experienced the problem themselves.

- Balanced skill sets: A team that doesn't just have three PhDs, but also includes expertise in sales/deal-making, regulatory pathways, or bioprocess engineering.

- Relentless and open-minded leadership: Founders who are deeply committed to the science but are willing to pivot their business model based on market or regulatory feedback.

- Velocity and learning rate: Evidence of rapid iteration, decision-making, and ability to absorb feedback and act on it.

- Resourcefulness: Ability to get things done with limited capital (creative partnerships, early data, non-dilutive funding).

- High-tier institutional backing: Coming out of a prestigious lab that can "vouch" for the technical rigor of the work.

- Diversity of perspective: Teams that combine "insider" industry experience with "outsider" technical innovation (e.g., a software engineer and a biologist building a discovery platform).

Red flags

- The "Single-Threaded" Founder: A solo founder with no technical or commercial partner, which creates a high "key-man" risk.

- Academic-only mindset: A team that views the company as an extension of a research lab and lacks a sense of urgency regarding commercial milestones and "burn rate."

- Low-engagement advisors: Listing famous names who haven't spoken to the founders in six months or who have "conflicting" roles at major competitors.

- Missing critical functions: A biotech company with no clear plan for regulatory or manufacturing leadership as they approach their next value inflection point.

- Equity imbalances: Unusual cap table structures where the active founders own too little of the company to stay motivated through a 10-year development cycle.

The Ask

The ask shows how much you are raising and what you plan to accomplish with it. We wrote about choosing how much to raise here.

Biotech raises are stage-defined by convention, and investors will immediately situate your ask within the standard progression from discovery through IND-enabling studies, Phase I, Phase II, and beyond. Your raise must be explicitly tied to a clinical or regulatory milestone, and your use of proceeds must map to the specific studies, trials, and manufacturing activities required to reach it.

Be precise about what data package this round generates and why that package is sufficient for the next financing or partnership event. "This $8M seed funds IND-enabling tox studies and CMC development, targeting IND filing in Q3 2026 and a Series A to fund Phase I."

What gets VCs excited

- Raise explicitly tied to a regulatory milestone (IND filing, Phase I completion, Phase II readout) with a clear timeline

- Use of proceeds broken into study-level specificity: tox package, CMC development, biomarker work, clinical site activation

- Understanding of what partnership or out-licensing opportunities the data package enables

- Clarity on what the milestone means for valuation inflection at the next round

Red flags

- Raise sized on optimistic trial timelines without contingency for enrollment delays or manufacturing setbacks

- Lumping CMC, tox, and clinical costs into a single undifferentiated number

- No discussion of what happens if the primary endpoint is not met—what optionality exists?

- Underestimating cost of GMP manufacturing for clinical supply

- Round sized to reach a data point that isn't sufficient for Series A—leaving the company in a gap

Back your ask with a clear financial model that shows how you will spend capital over time, how you will hire, the key assumptions driving the business and how that ties to the milestones you will unlock. The model isn’t about absolute precision, it's about showing you understand the business and know how to deploy capital to move the company forward.

Pitching: Do's & Dont's

Here's how (and how not) to pitch:

The best pitches are conversational. Answers should be succinct yet demonstrate depth of thought.

At early stages, VCs heavily index on why you're the right team to build this business and why you've chosen each teammate.

Great founders bridge vision with detail. They intimately understand their problem space and can explain it clearly—both the problem and the system around it. They understand the path to scale and can map how the business will evolve getting there.

Biotech-specific pitching guidance:

Do

- Show, don't just tell: Use clear, high-contrast microscopy images, chromatograms, or dose-response curves. Professional, clean data visualization is a proxy for the quality of your lab work.

- Have crisp answers on unit economics: You should be able to recite your COGS, installation costs, service costs, and path to profitability from memory. If you don't know your numbers cold.

- Demonstrate customer intimacy: Drop specific details that show you deeply understand your customer or current care delivery model.

- Benchmark your results: Always show your data side-by-side with the "Gold Standard" or the "Standard of Care." Innovation is relative; "good" results only matter if they are "better" than what exists.

Don’t

- Don't hide the "Dirty Laundry": If an experiment failed or a safety signal appeared, explain why and what you learned.

- Avoid the "Science Lecture": Don't spend 15 minutes on the history of the ribosome; spend it on why your ribosome-targeting tool is a $5B opportunity.

- Don't dismiss the competition: Saying "we have no competitors" is a flag. Even if there isn't another startup doing exactly what you do, you are always competing with the "Status Quo."

- Avoid "Bio-babble": Even with technical VCs, keep your narrative clear. If you can't explain the value proposition to a generalist partner at the firm, you won't get through the investment committee.

- Don't dismiss competition: Saying "we have no competitors" or "they're all doing it wrong" makes you look naive. Acknowledge competitors and explain your differentiation respectfully.

Common founder traps

- Technology-first framing: Leading with "we use generative protein design" instead of "we solve the $10M-per-failure target validation problem."

- Unrealistic timelines: Claiming you will go from lead optimization to an IND filing in 12 months when you haven't identified a CDMO or started tox studies.

- Ignoring "hidden" development costs: Focusing only on the cost of the drug or tool while ignoring the expenses of regulatory filings, clinical site management, quality control (QC), and intellectual property maintenance that often exceed core R&D spending.

- Overestimating adoption rates: Assuming 80% market penetration because your data is superior, while ignoring physician "inertia," complex hospital procurement cycles, or the difficulty of securing favorable insurance reimbursement.

We hope this guide was useful to you! If you'd like to get in touch, don't hesitate to reach out to Julian.Capital or 2048 Ventures, and apply in <1 minute to get put in touch with thesis fit investors for free at DeepChecks.VC.